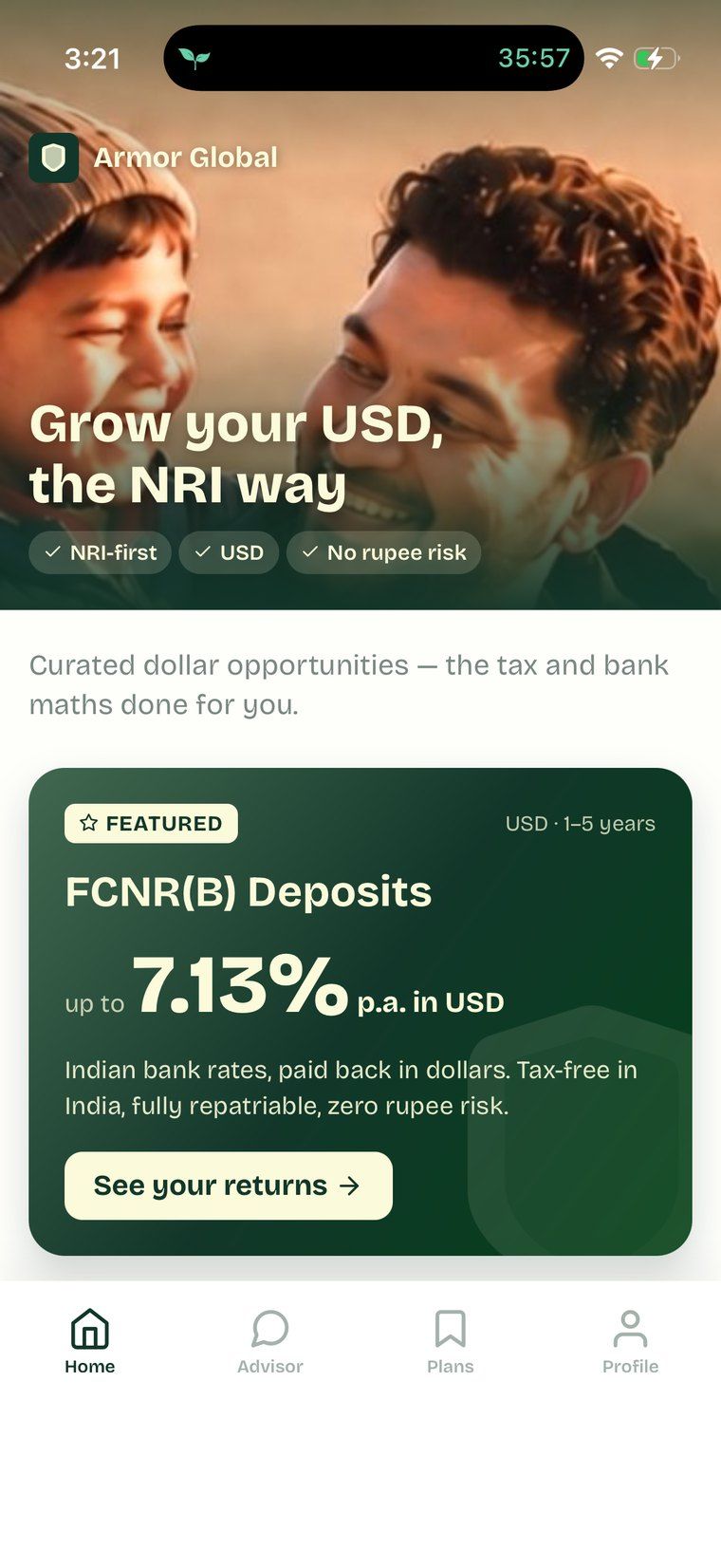

Your dollars can earn a lot more — safely. Armor Global shows you how.

Armor Global is built for NRIs who want their overseas savings to actually work. Right now there is a rare, time-limited opening: Indian banks are paying the highest dollar returns in years. Armor shows you whether it fits your money — and which bank is genuinely best for you.

NRI-exclusive. USD in, USD out. Live rates from 15+ banks.

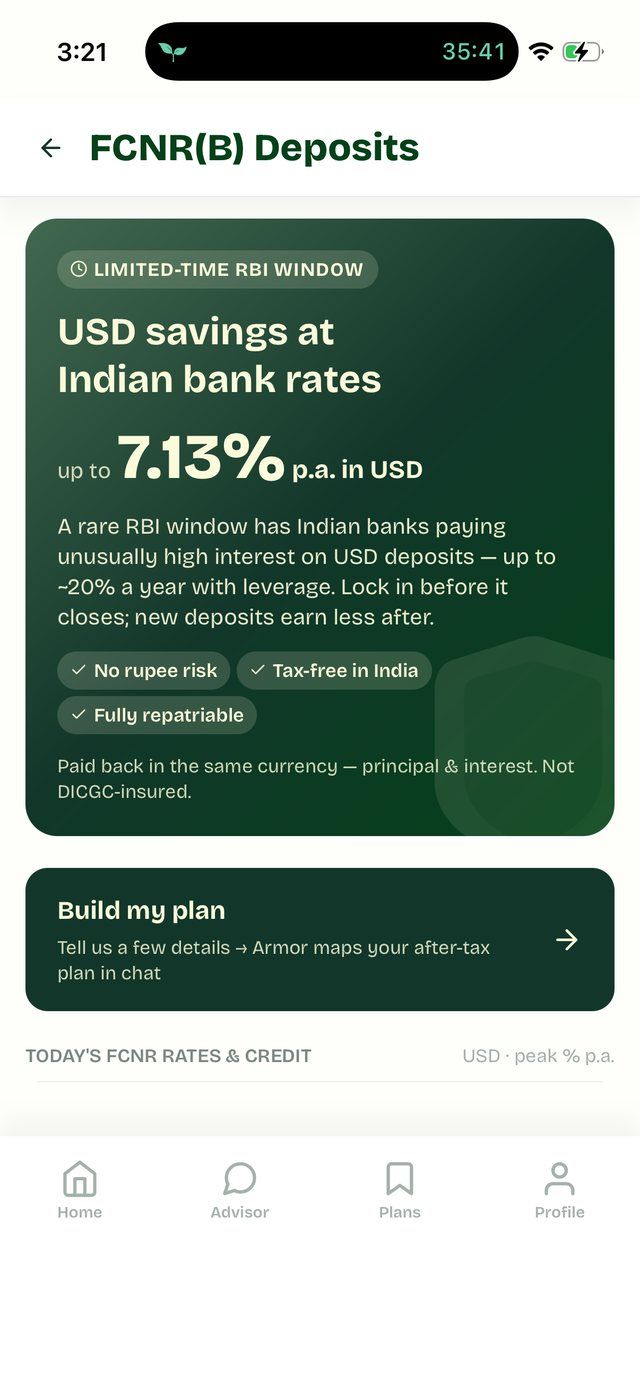

The RBI swap window for fresh FCNR deposits closes on 30 September 2026.

First, the opportunity — in plain English.

It is called FCNR: a fixed deposit you hold in US dollars with an Indian bank, under RBI rules. Dollars in, a fixed return, dollars out — no rupee risk, and tax-free in India. A temporary RBI window has pushed those returns above 6-7%, the highest in years. Every bank quotes its own rate, but none tell you whether it truly fits your money — after your tax, against every other option. That is exactly what Armor Global does.

Every NRI weighing this needs Armor Global.

Whether it is the right call depends on your tax, your timeline, and how each bank’s fine print stacks up. That is the work Armor does for you — in minutes, in plain language.

Compare every bank, live

Rates moved from 4% to over 7% in days, and they are still moving. Armor tracks them across 15+ banks so you are comparing today's numbers, not last week's headline.

See your real return, not the headline

The advertised rate is before your tax. Armor works out what you actually keep, factored for where you live, and flags FBAR and FATCA before they become a problem.

Build a plan in chat

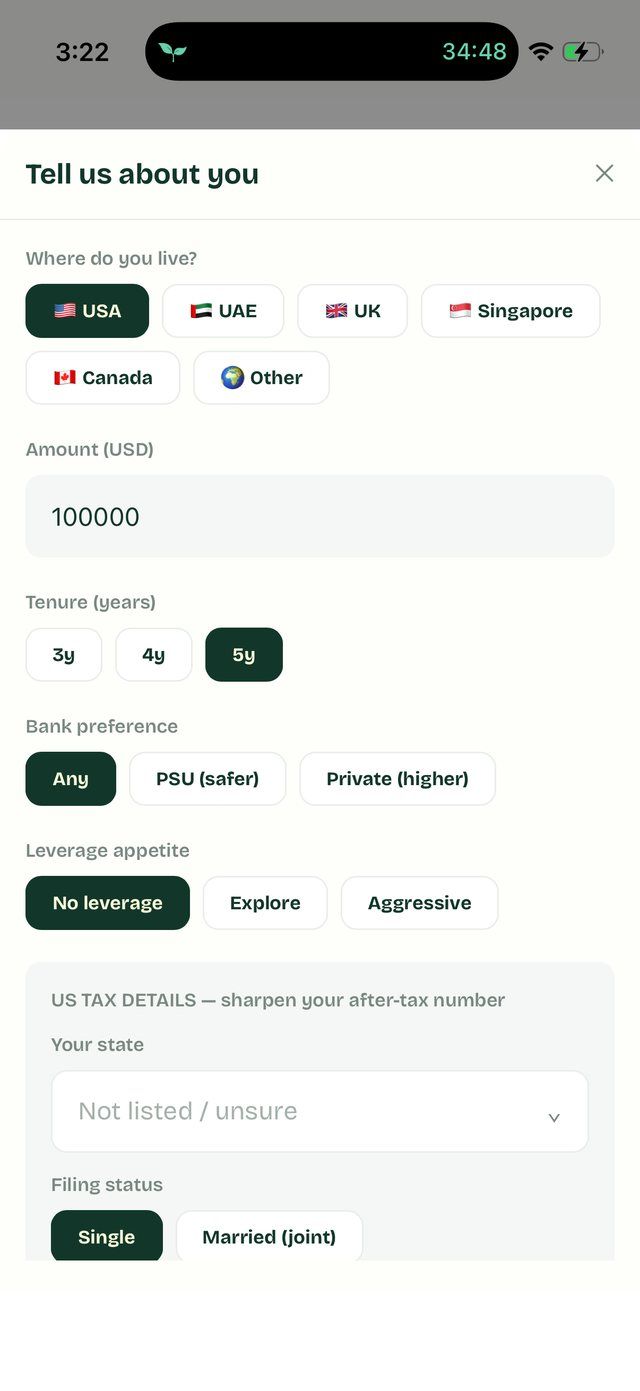

Tell Armor your amount, your tenure, and where you live. It maps your after-tax plan in plain language, grounded in a knowledge base, not generic advice.

Armor Global helps you effortlessly grow your wealth

See it work.

The same questions a good planner would ask, answered in the app. Swipe through.

Open FCNR, see the whole picture

The rate, the window, and the risks in one place. No rupee risk, tax-free in India, fully repatriable, with the fine print in plain sight.

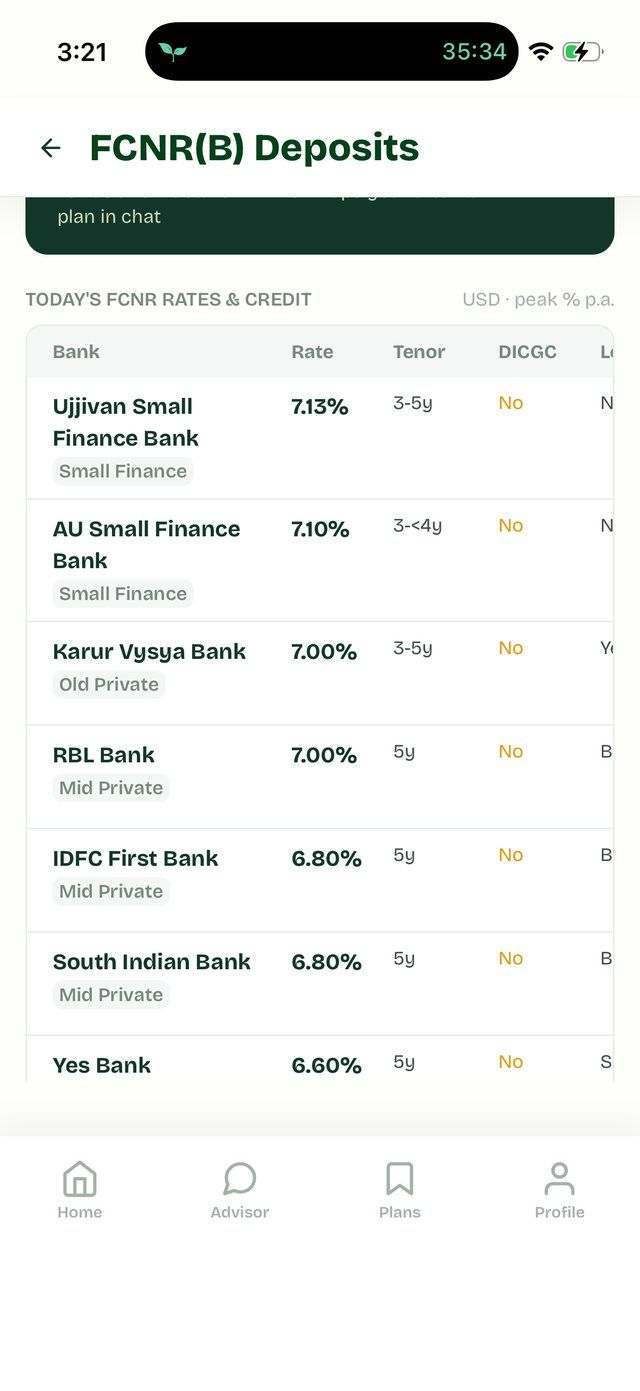

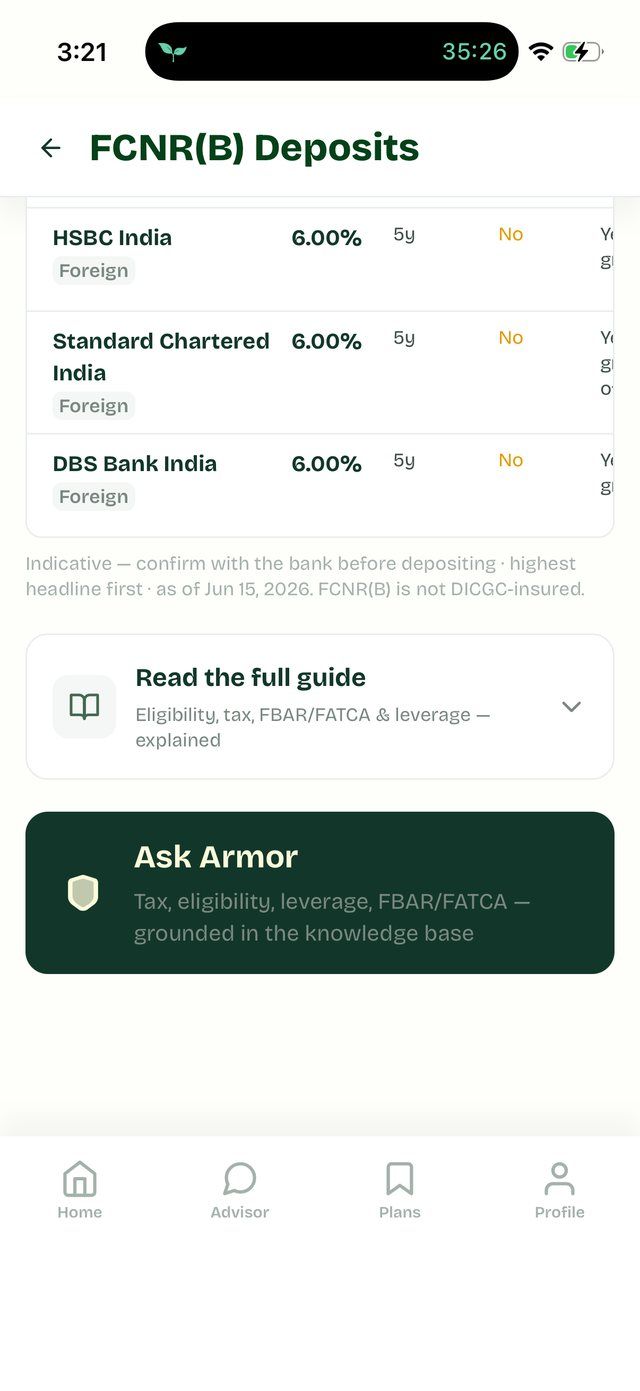

Compare every bank, highest first

Today's FCNR rates across small finance, private, and foreign banks, sorted with the best headline at the top, tenor and DICGC status beside each.

Identify what fits your financial picture

Fill in where you live, how much, and how long. Armor reads it against your situation and shows which option actually fits you, sharpened for your tax.

Ask Armor

You can explore by asking questions to Armor Advisor. It answers from a maintained knowledge base, not generic advice you have to second-guess.

Read this before you lock in.

This is a new and unusually generous window, which is exactly why it deserves a clear head. Four things the rate ads will not lead with.

It opened in June 2026

There is little track record on how this plays out once the window closes and the earlier rate framework returns.

Your money is held for a year

These special-rate deposits carry a one-year lock-in. Early exit carries penalties, so size it against cash you will not need.

DICGC cover stops at ₹5 lakh

Deposit insurance applies, but it is capped at ₹5 lakh per bank and paid in rupees. On a large dollar deposit that is a rounding error, so treat the bulk as uninsured and pick the bank on its strength.

Leverage is not for most people

Borrowing against the deposit to chase a bigger number is a different, high-risk play. If an outsized return finds you elsewhere, treat it with suspicion.

Armor Global is built to give you the real picture, not the loudest one. Know if it fits, then decide.

See if it fits your money — before 30 September.

Compare every bank, see your real after-tax return, and build your plan in minutes.

Try Armor Global today →NRI-exclusive · USD in, USD out · Live rates from 15+ banks

FCNR(B) deposit rates are indicative and set by individual banks under the temporary RBI window for fresh deposits booked on or before 30 September 2026. Rates and terms change, confirm with the bank before depositing. FCNR(B) deposits are not DICGC insured. Armor Global provides planning tools and information, not investment advice.