The Dopamine Gap: Why Your Brain Won't Let You Rebalance Your Portfolio

Investing · 25 Mar 2026 · Team Armor

The Dopamine Gap explains why sometimes even smart investors with sound strategies still can't bring themselves to rebalance: selling a stock that's up 40% feels like a loss, and buying one that's down 20% feels like a mistake. In this post, we break down the three cognitive biases that make portfolio rebalancing the most-skipped financial habit and three practical strategies to overcome them, including the system-based approach that takes your emotions out of the equation entirely.

The other day, a close friend of mine was catching me up on some insights he had about the ongoing geopolitical situation. He kept coming across Instagram posts from popular investors suggesting the timing is right. He's read the research. He understands that right now is the time to look at his portfolio closely and make the right investments.

And yet, every Sunday when he sits down to do it, he opens Instagram instead.

He's not a beginner. He's a product manager who can build a roadmap for a product used by millions but he can't bring himself to sell the stock that's up 40% and buy the one that's down 20%. Not because he doesn't understand the logic but because the logic feels wrong.

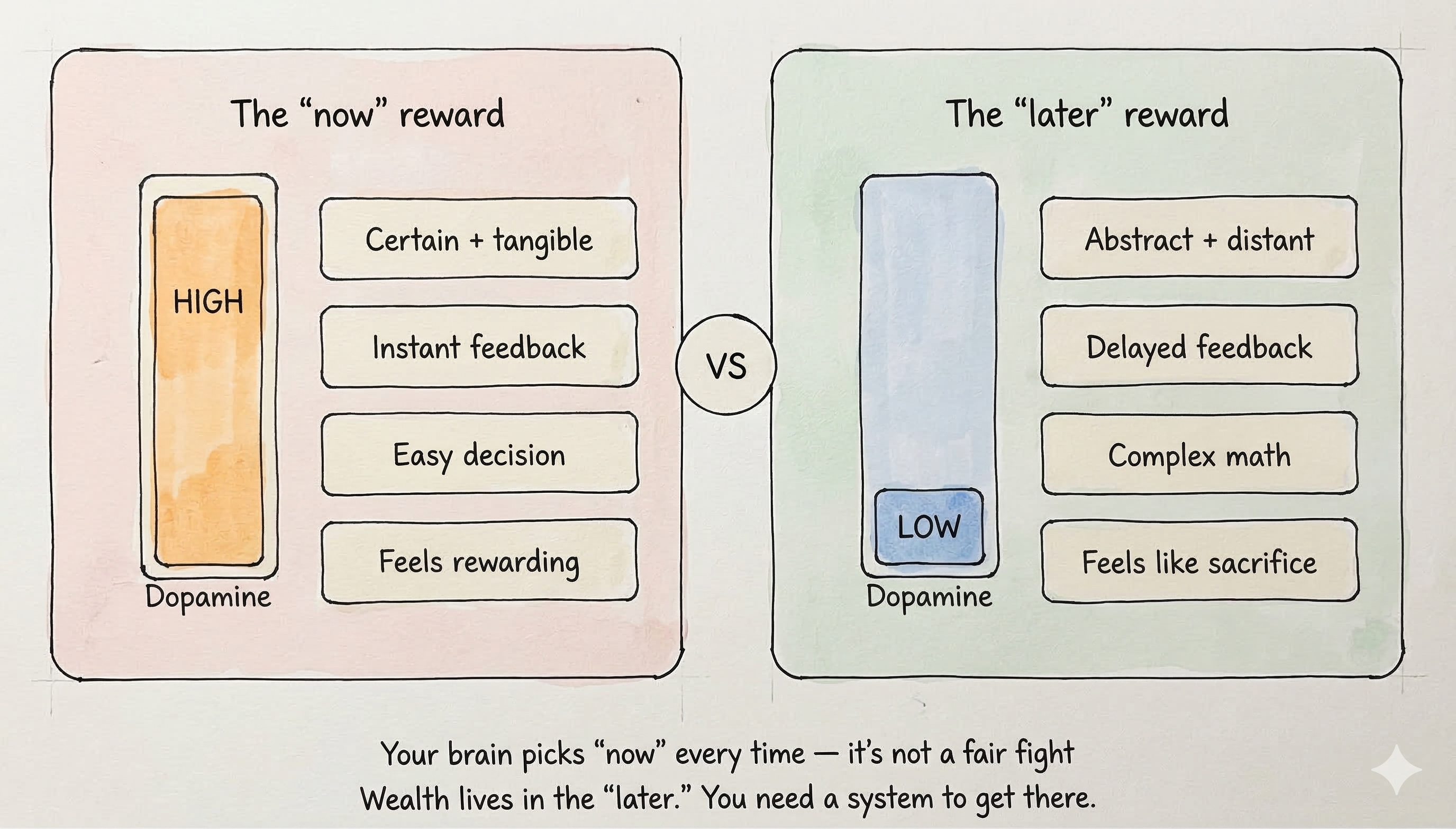

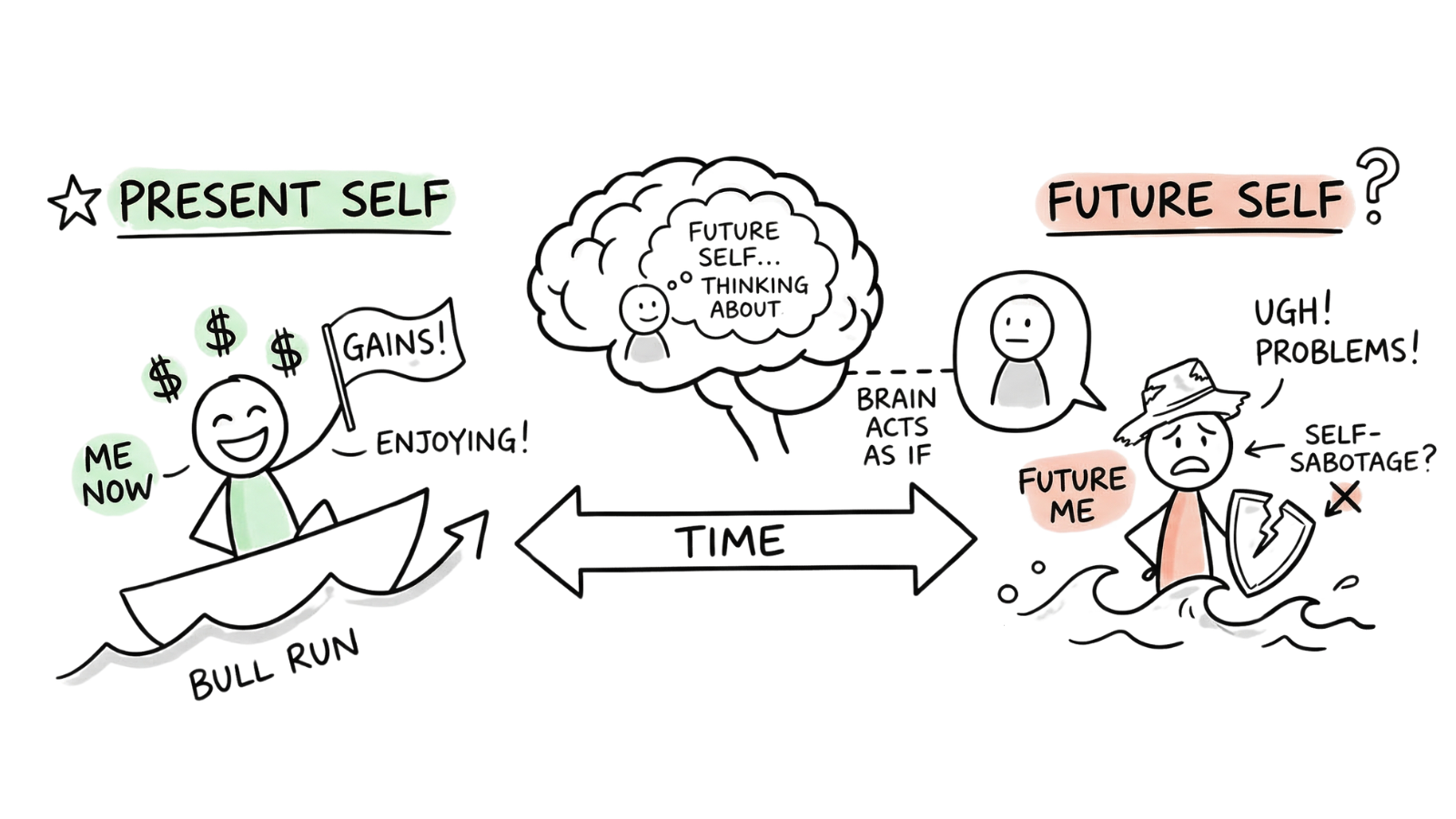

The part of our brain which assesses rewards and pleasure is regulated by a chemical called dopamine. It influences our motivation to pursue various activities. When it comes to our portfolio, dopamine creates a massive imbalance. Holding a winning stock feels good, a hit of certainty, validation, progress. Selling that winner to buy a stock that's falling? That's the opposite of a dopamine hit. It's a dopamine tax.

This imbalance between how your brain rewards holding versus rebalancing is what we call the Dopamine Gap. It's the single biggest reason smart investors with sound strategies still fail to rebalance their portfolios.

Why Does Your Brain Fight Portfolio Rebalancing?

Thousands of years of evolution have trained us to grab what's available right now because tomorrow was never guaranteed. In the context of portfolio rebalancing, this ancient wiring shows up in three specific cognitive traps, each one targeting a different part of the decision.

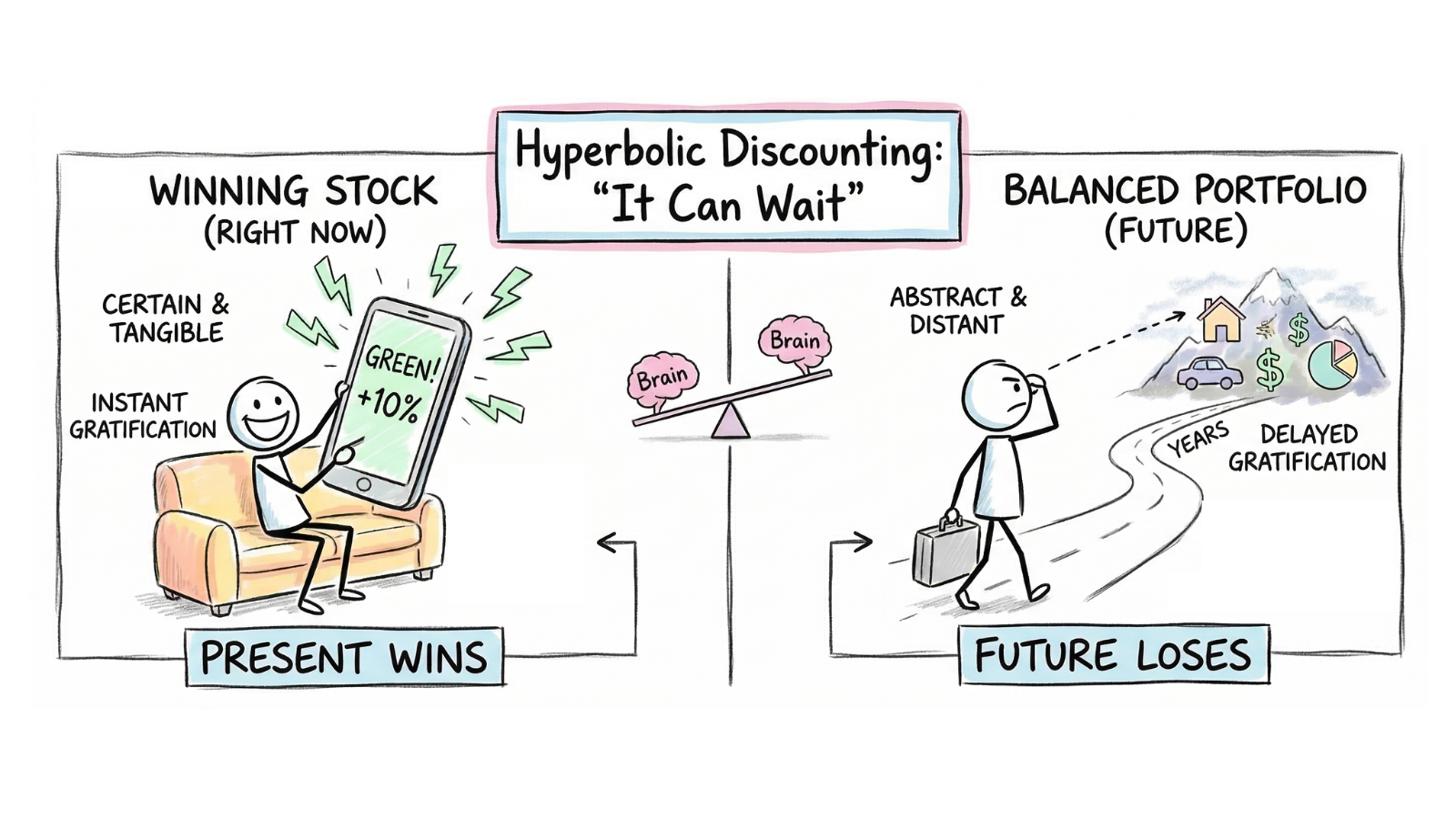

Hyperbolic Discounting: It Can Wait

A balanced portfolio in the future feels abstract and distant.The reward for rebalancing is spread across years. The reward for holding is refreshed every time you open the app and see green. The future always loses to the present when dopamine is the scorekeeper.

The 'Future Self' Gap: Not My Problem Yet

The you who will face the market correction isn't the you who's enjoying the bull run right now. Delaying the rebalance doesn't feel like self-sabotage, it feels like someone else's problem.

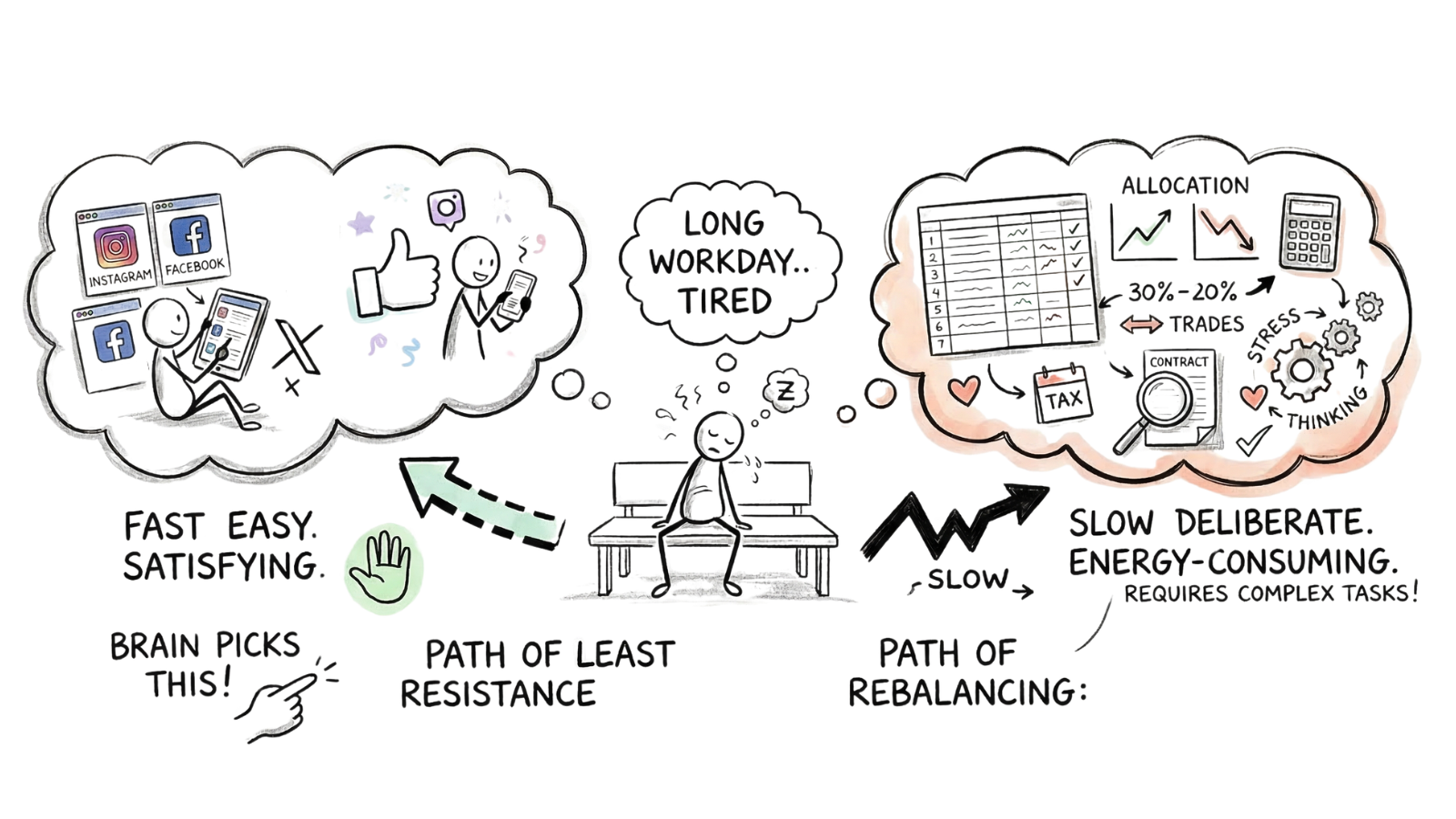

Decision Fatigue: I'll Do It When I Have Energy

Rebalancing requires System 2 thinking which is slow, deliberate, and energy-consuming where you have so many steps to complete. Meanwhile, checking Instagram and planning a vacation is System 1 thinking. Fast, easy, and satisfying. So after a long workday, your brain picks the path of least resistance. Every single time.

How to Actually Rebalance Your Portfolio

If the problem is emotional, the solution can't be too. You have to move the portfolio rebalancing decision from your feelings to a framework. Here are three strategies that work.

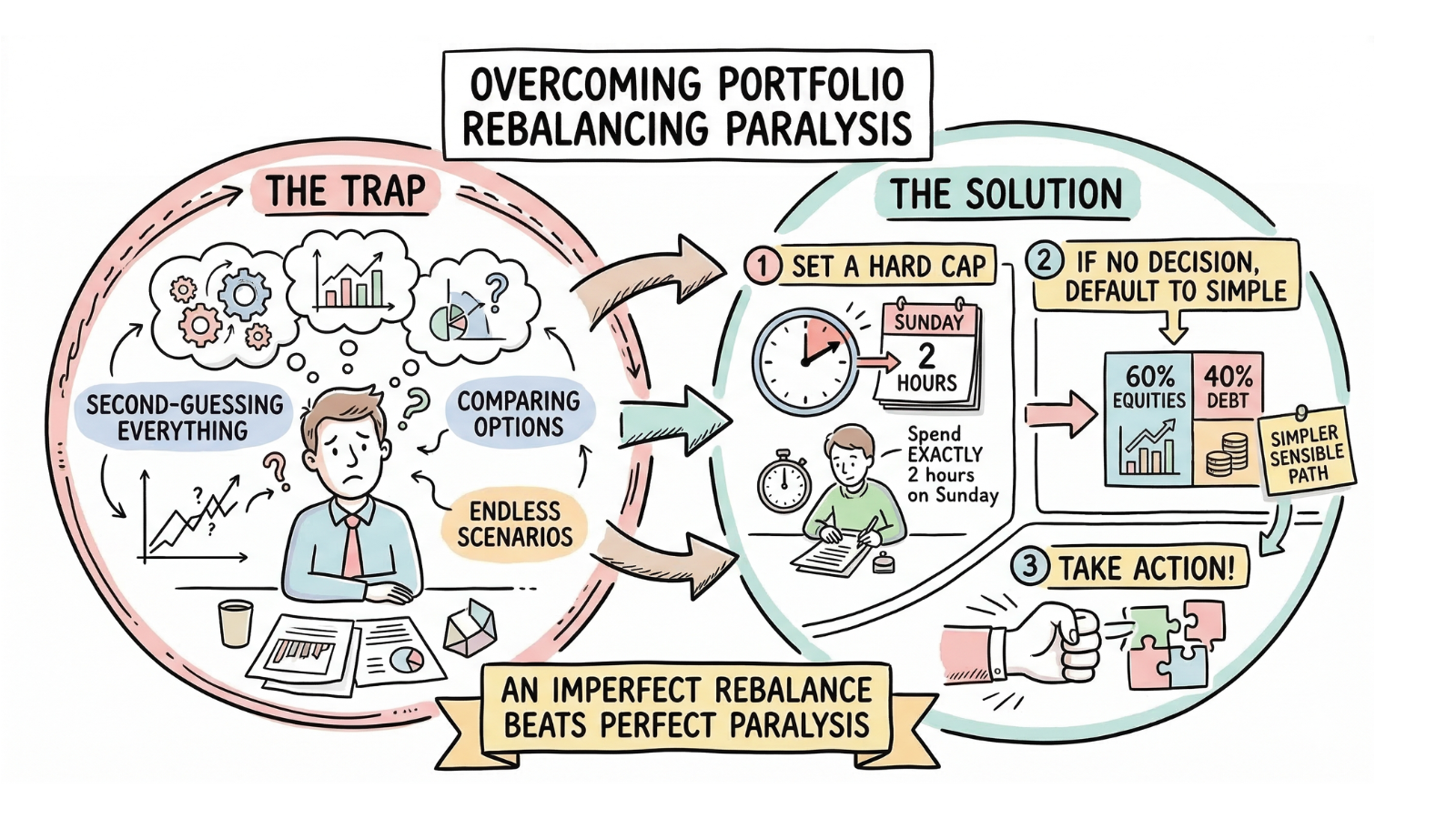

1. The Rule of 2

Your brain will run scenarios forever if you let it. The Rule of 2 suggests that you set a boundary. Spend 2 hours on Sunday and then decide. If you're not able to, default to a 60/40 equity-debt split. An imperfect rebalance beats perfect paralysis.

2. Lower the Activation Energy

You procrastinate on rebalancing because the task feels like a mountain. The fix: break it into micro-steps across days. Today, just log in and look at your current percentages. Tomorrow, calculate the gap. The day after, execute. Each step on its own is tiny, but tiny steps compound just like your money.

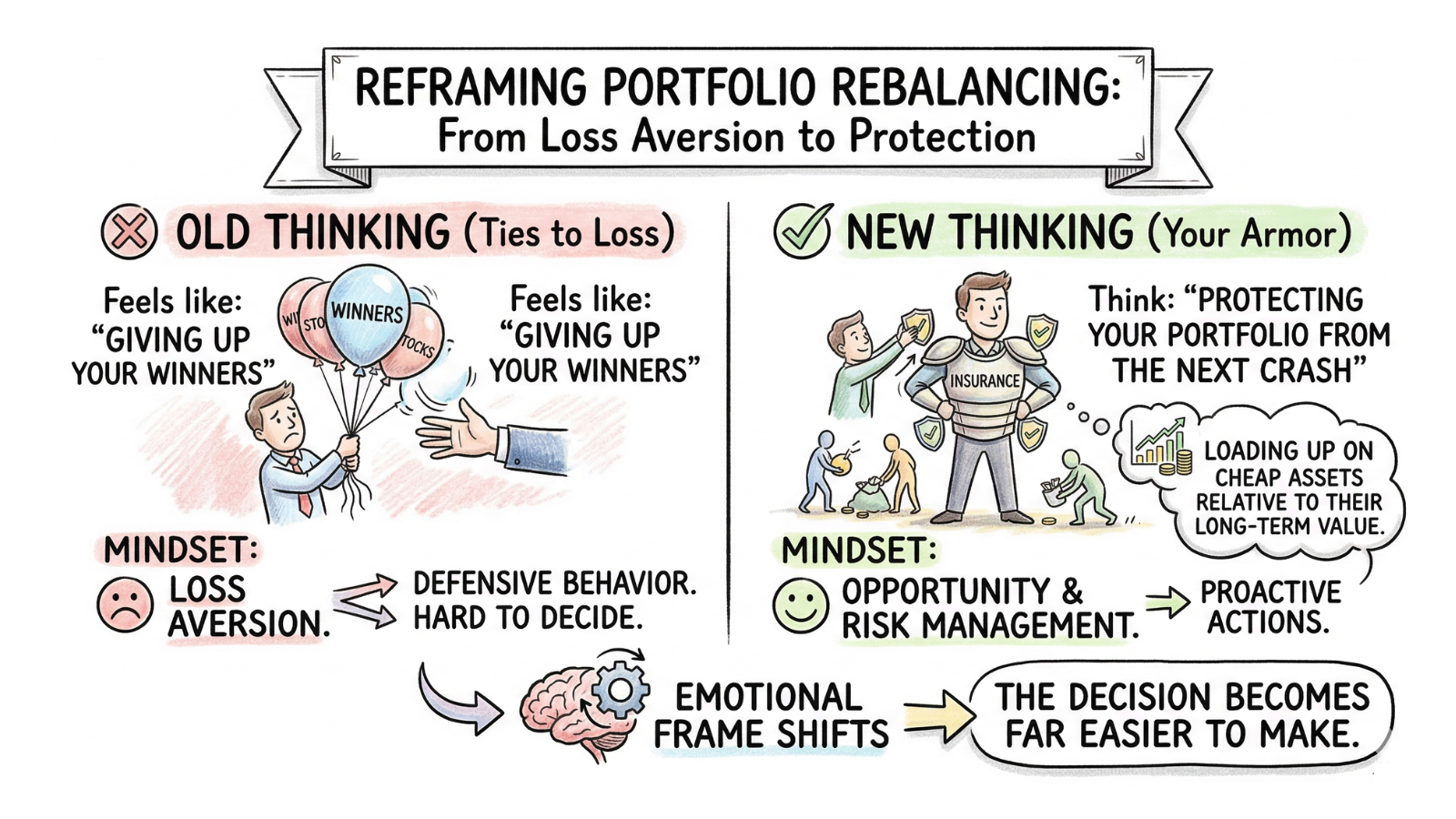

3. Shift from 'Selling Winners' to 'Buying Insurance'

You're not selling winners, you're buying insurance against a market correction. You're not chasing losers, you're loading up on assets that are cheap relative to their long-term value. When the emotional frame shifts from 'I'm losing my best stocks' to 'I'm protecting my portfolio from the next crash', the decision becomes far easier to make.

The bottom line: Portfolio rebalancing is hard because your brain treats selling winners as a loss and buying losers as a mistake. Three cognitive biases: hyperbolic discounting, the future self gap, and decision fatigue stack on top of loss aversion to make rebalancing the financial habit most likely to be skipped. The fix isn't more willpower. It's a system that rebalances based on math, not mood.

Frequently Asked Questions

What is the Dopamine Gap in investing?

The Dopamine Gap is the imbalance between how your brain rewards holding a winning investment versus rebalancing your portfolio. Holding winners delivers a dopamine hit. There is certainty, and validation. Selling that winner to buy an under performer is the opposite: a dopamine tax. This gap is the single biggest reason smart investors with sound strategies still fail to rebalance their portfolios consistently.

Why is portfolio rebalancing so hard?

Portfolio rebalancing is hard because it asks you to do the opposite of what feels right, sell investments that are winning and buy ones that are losing. This triggers loss aversion, a cognitive bias where the pain of giving something up is roughly twice as intense as the pleasure of gaining something equivalent. On top of that, three additional biases stack against you: hyperbolic discounting makes a balanced portfolio feel less valuable than keeping your current winners, the future self gap makes you treat your future self as a stranger who can deal with the consequences, and decision fatigue means rebalancing demands the kind of slow, deliberate thinking your brain avoids after a long day.

How often should you rebalance your portfolio?

It is recommended to rebalance your portfolio quarterly or whenever your asset allocation drifts more than 5% from your target. For example, if your target is 60/40 equity-debt and equities grow to 66% or more, that triggers a rebalance. Calendar-based approaches such as checking every quarter works well because they remove the decision of ‘when’ and lets you focus only on ‘what needs adjusting’. Automated systems take this further by monitoring drift continuously and rebalancing when the math says to, not when you remember to check.

What happens if you never rebalance your portfolio?

Without rebalancing, your portfolio silently drifts from its target allocation. A portfolio that started as 60/40 equity-debt could drift to 75/25 during a bull run, meaning you're carrying significantly more risk than you originally signed up for. When a market correction hits, you're overexposed to exactly the same assets falling the hardest. The cost of inaction doesn't just add up, it compounds in the wrong direction, turning a manageable allocation drift into a real financial setback.

How can I overcome the fear of selling winning stocks?

The most effective way to overcome the fear of selling winners is to reframe what rebalancing means. Instead of thinking ‘I'm giving up my best stocks’ think ‘I'm buying insurance against the next market correction’. This shifts the emotional reward from greed (unreliable) to safety (consistent). Two practical strategies also help: cap your decision time at 2 hours with a default fallback so you can't overthink, and break the task into micro-steps across days - log in today, calculate the gap tomorrow, execute the day after. If the fear still wins, automate the process entirely so the decision is never in your hands.