What Is a Financial Health Check? Why Every Indian Needs One

Product News · 14 Apr 2026 · Team Armor

We get our cars serviced, our blood tested, our CIBIL checked. But almost nobody has ever had their finances structurally assessed. Not their returns, not their balance but their actual financial architecture. Whether it's built to protect them, grow their wealth, and survive whatever comes next. That's what a financial health check is. And most Indians have never had access to one.

Car broke down ? You give it for service.

Out sick for many days? You get a blood test.

You want to get a loan? You check your CIBIL.

Is your money in the right place?

We have tests and checks for everything except our finances.

A financial health check is the practice of deliberately stepping back and asking: is my financial life structurally sound? The question is often "Do I have money in my account right now?" but we barely acknowledge the underlying architecture of our finances, which should be built to protect you, grow your wealth, and absorb unexpected life events.

This is different from checking your portfolio returns. It is different from monitoring your CIBIL score. It is a comprehensive review of the five dimensions that together determine whether you are financially resilient or financially fragile despite appearing stable on the surface.

Why Most Indians Have Never Done One

My honest answer is that the infrastructure to do so has not existed. Access to a qualified financial advisor in India is limited to those with investable assets above a certain threshold or the social network to find one. India has fewer than 1000 SEBI-registered investment advisors as of April 2026, serving a country of 33 crore households.

Secondly, tools available in the present day have been built for transactions, not assessments. Mutual fund apps optimise for SIP sign-ups, insurance platforms optimise for policy sales, banking apps show you what you have, not whether it has been structured correctly.

Lastly, financial health is genuinely multi-dimensional. If you check only one dimension without the others, it gives you a false sense of security. My friend Ayush, has a strong investment portfolio but hasn’t opted for term insurance, he is not financially healthy. Another friend, Swapna has high savings but 60% of her income is locked in EMIs which is a fragile financial structure.

Financial health only makes sense when all five dimensions are looked at together. A gap in any one of them can undermine the strength of the other four.

What are the Dimensions of Financial Health?

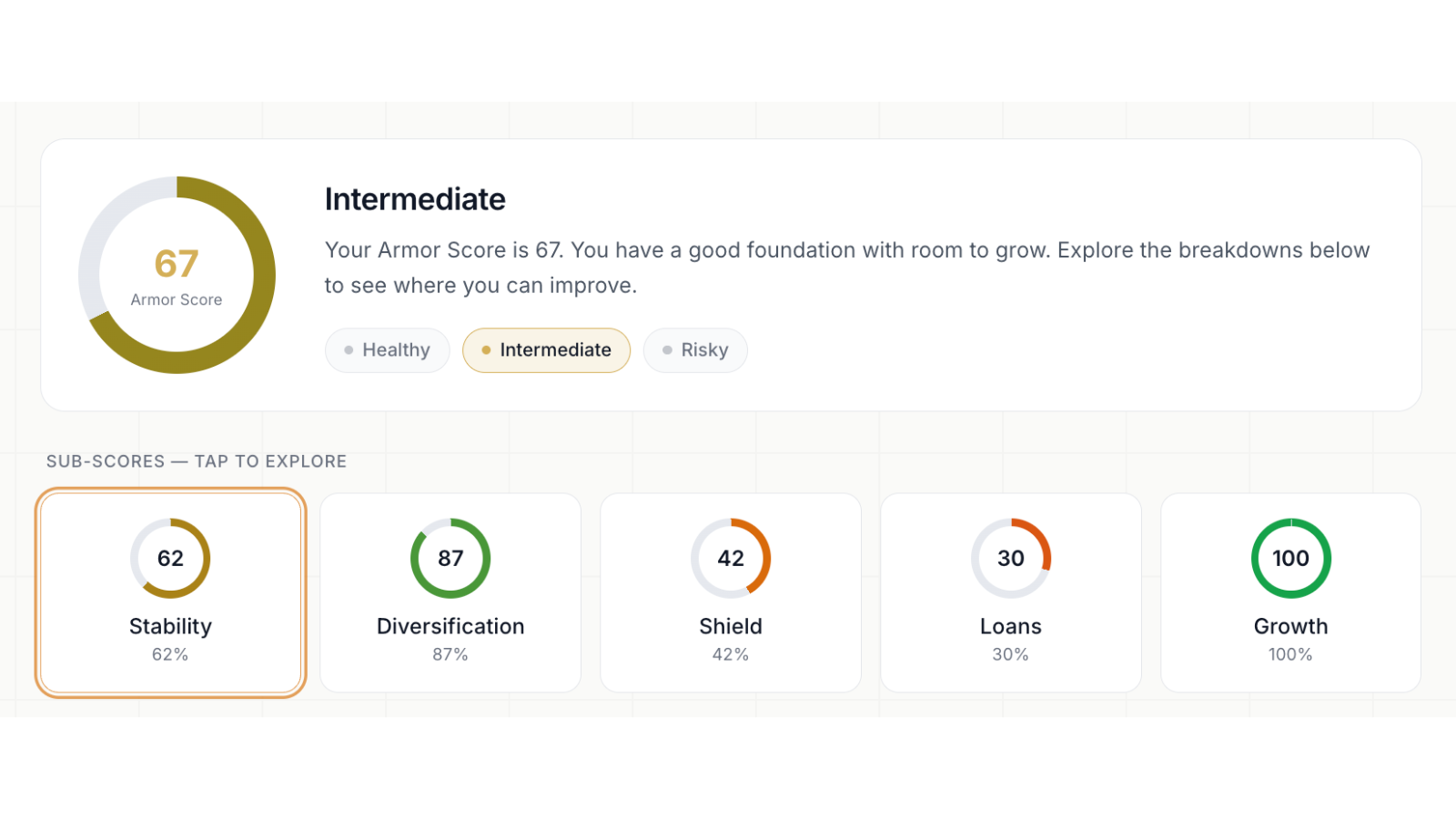

A rigorous financial health check examines five distinct areas. Each dimension is independent; strength in one does not compensate for weakness in another. Together, they produce a complete picture of your financial resilience.

Let’s look at each of these one by one.

1.Liquidity: Your Emergency Safety Net

The first question in any financial health check is simple and uncomfortable: if your income stopped tomorrow, how long could you survive without changing your lifestyle or liquidating long-term investments? The target is six months of total monthly outgo which should include living expenses plus EMI obligations.

For example, If Naresh earns 2.5 lakhs a month, and his monthly expenses including EMI is 1.75L then ideally he should have around 10L as his emergency funds.

2. Diversification: How Spread Is Your Wealth ?

This dimension examines how your total net worth is allocated across asset classes : equity, debt, gold, and real estate. Concentration risk is one of the most under-appreciated dangers in personal finance.

To help you understand this better, if you have a total portfolio of 4 Cr and 80% allocation is real estate, then it is not a diversified portfolio rather it is a single bet on a single illiquid asset.

A proper financial health check will help you measure the gap between your actual allocation and a personalised ideal target.

3.Shield : Are You And Your Family Protected?

Insurance is the most neglected dimension of financial health in India. Everyone relies on the insurance policies given by the employer or takes term insurance without calculating if the quantum of coverage is adequate.

To paint a picture, A ₹50 lakh term plan for Priya with a ₹1.5 crore home loan and two dependents is not financial protection. It is a partial cushion. The target for life insurance should be 15 times her annual income plus outstanding liabilities.

What we’ve noticed is that most people are nowhere near it.

4. Loan Load : How Much Of Your Income Is Already Spent?

Debt is not inherently dangerous but unmanageable debt is. This dimension measures your debt-to-income ratio which is the percentage of your net monthly income that is committed to EMIs before you have paid a single rupee of living expenses. When this number crosses 50%, your finances become fragile - any income disruption leaves almost nothing for living expenses or savings.

5. Momentum : Are You Building Wealth Fast Enough?

Sushant and Kevin are two people with identical balance sheets but they can be heading in completely different directions. Kevin could be saving 5% of their income while Sushant could be saving 30% of the same income & they will look similar today but they will be in entirely different positions in ten years. This dimension measures your savings rate, the velocity at which you are building wealth, not just the current stock of it and the benchmark is 30% of net income.

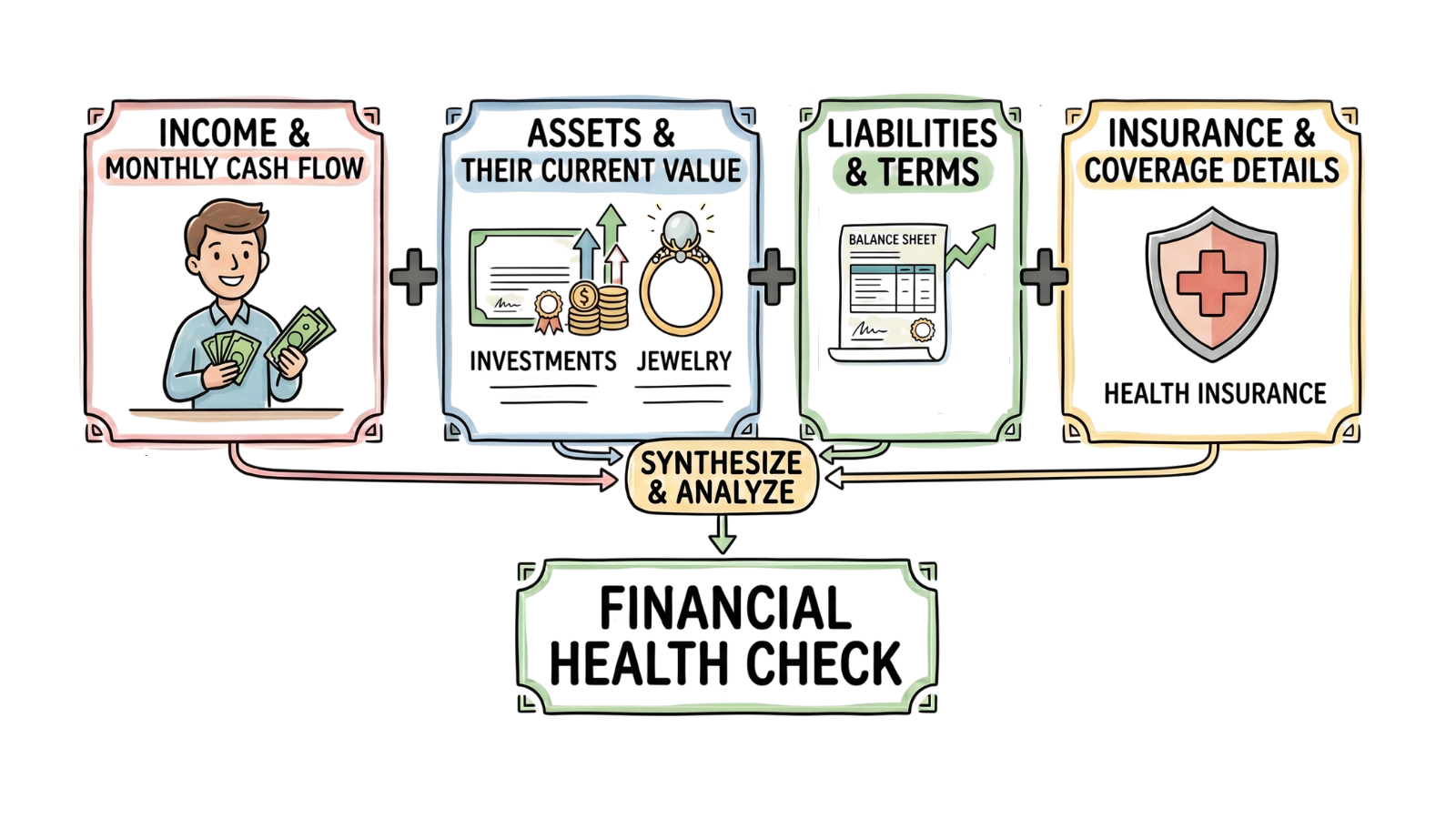

What a Financial Health Check Actually Looks Like

A structured financial health check requires four inputs: your income & monthly cash flows, your assets & their current values, your liabilities & their terms, and your insurance coverage details.

With these four inputs, all five dimensions of financial health can be assessed and scored against evidence-based benchmarks.

The output is a diagnostic picture that assesses which dimensions are healthy, which are weak, and in what order the weaknesses should be addressed. For example, fixing an insurance gap is more urgent than rebalancing a portfolio or building an emergency fund is more foundational than optimising equity allocation. The sequence matters.

How Often Should You Do This?

A financial health check is most useful when it is not a one-time event but a living assessment that updates as your financial life evolves like a job change, a new EMI, a child's birth, a parent's health event, each of these shifts your financial position and changes the picture. Ideally, you review the full picture annually and monitor the most dynamic dimensions like liquidity, loan load, and savings rate on a quarterly basis.

The goal is not to obsess over your finances. It is to have the structural confidence that comes from knowing your financial life is built to handle what comes next. That confidence is earned through visibility, not optimism.

"You cannot improve what you do not measure. A financial health check is simply the decision to measure the things that actually matter."

Where Armor Fits In

The Armor Financial Health Score is built to make this check accessible, structured, and ongoing for every earning Indian.

It takes the five dimensions described above, scores each against calibrated benchmarks, and produces a single composite number that reflects the overall resilience of your financial life. More importantly, it tells you what to fix first. The Armor Financial Score is a prioritised diagnostic, the closest thing to an honest financial health check that most Indians have ever had access to.

Frequently Asked Questions (FAQs)

1.What is a financial health check?

A financial health check is a structured assessment of five dimensions of your financial life: liquidity, diversification, insurance coverage, debt load, and savings momentum. Unlike checking your bank balance or portfolio returns, it examines whether your overall financial structure is resilient enough to protect you, grow your wealth, and absorb unexpected events.

2.How is a financial health check different from checking my portfolio returns?

Portfolio returns tell you how your investments performed. A financial health check tells you whether your entire financial structure is sound including whether you have adequate insurance, manageable debt, sufficient liquid reserves, and a savings rate that is building wealth at the right velocity. Strong returns in one area do not compensate for structural gaps in another.

3.How much emergency fund should I have as part of a financial health check? The target is six months of total monthly outgo which includes living expenses plus all EMI obligations. If your monthly outgo is ₹1.75L, your emergency fund target is approximately ₹10.5L, held in a liquid fund or savings account that is separate from long-term investments.

4.What is a healthy debt-to-income ratio in India?

When your EMI obligations exceed 50% of your net monthly income, your financial structure becomes fragile. Any income disruption leaves almost nothing for living expenses or savings. A financially healthy debt load keeps total EMIs below 40% of net income, leaving room for both living expenses and wealth-building.

5.What savings rate should I be targeting?

The benchmark for the Momentum dimension is 30% of net income. Someone saving 5% and someone saving 30% may look identical on paper today and same balance sheet, same income but they will be in entirely different financial positions within ten years. Savings rate measures the velocity at which wealth is being built, not just the current stock of it.

6.How often should I do a financial health check?

The full five-dimension picture should be reviewed annually. The three most dynamic dimensions, liquidity, loan load, and savings rate, are worth monitoring quarterly, since a job change, a new EMI, or a major expense can shift these significantly in a short period. A financial health check is most useful as a living assessment, not a one-time event.

7.What information do I need to complete a financial health check?

Four inputs cover everything: your income and monthly cash flows, your assets and their current values, your liabilities and their terms, and your insurance coverage details. With these four inputs, all five dimensions can be assessed and scored against benchmarks relevant to your income level and life stage.