ESOP and RSU Tax in India: The 2026 Guide

Investing · 20 May 2026 · Team Armor

ESOPs and RSUs are two of the most valuable benefits an Indian salaried professional can earn, and two of the most badly taxed if you don't plan around them. This guide walks through how the tax actually works in 2026, the four decisions that move your final number, and the five mistakes that quietly cost most employees lakhs on equity their company already paid them.

Your equity just turned into shares, either through RSU vesting or ESOP exercise. Before you've sold a single one, the tax bill has already landed.

That's the part nobody explains when HR hands you your grant letter. You're told you'll receive ₹40 lakh in ESOPs when you join. What you're not told is that the moment you exercise those options, the Indian income tax system treats the entire gain as salary income, taxed at your slab rate. For most salaried professionals, that means 30% plus cess.

ESOP and RSU taxation in India is genuinely complex, but it isn't unmanageable. With the right sequencing, you can legally keep significantly more of what your company gave you.

This guide walks through how the tax works in 2026, the four decisions that move the number, and the five mistakes that quietly cost salaried professionals between ₹5 and ₹15 lakh a year.

Key terms in 30 seconds

- ESOP (Employee Stock Option Plan): A right to buy company shares at a fixed price (the exercise price) after a vesting period.

- RSU (Restricted Stock Unit): A promise to give you company shares at a future date, with no exercise price.

- FMV (Fair Market Value): The price the share would trade at on a given date. Triggers your tax at Stage 1 and becomes your cost base for Stage 2.

- Perquisite: A salary benefit. Taxed at your income slab rate, not at capital gains rates.

- Slab rate: Your personal income tax rate, ranging from 0% to 30% plus cess, based on total annual income.

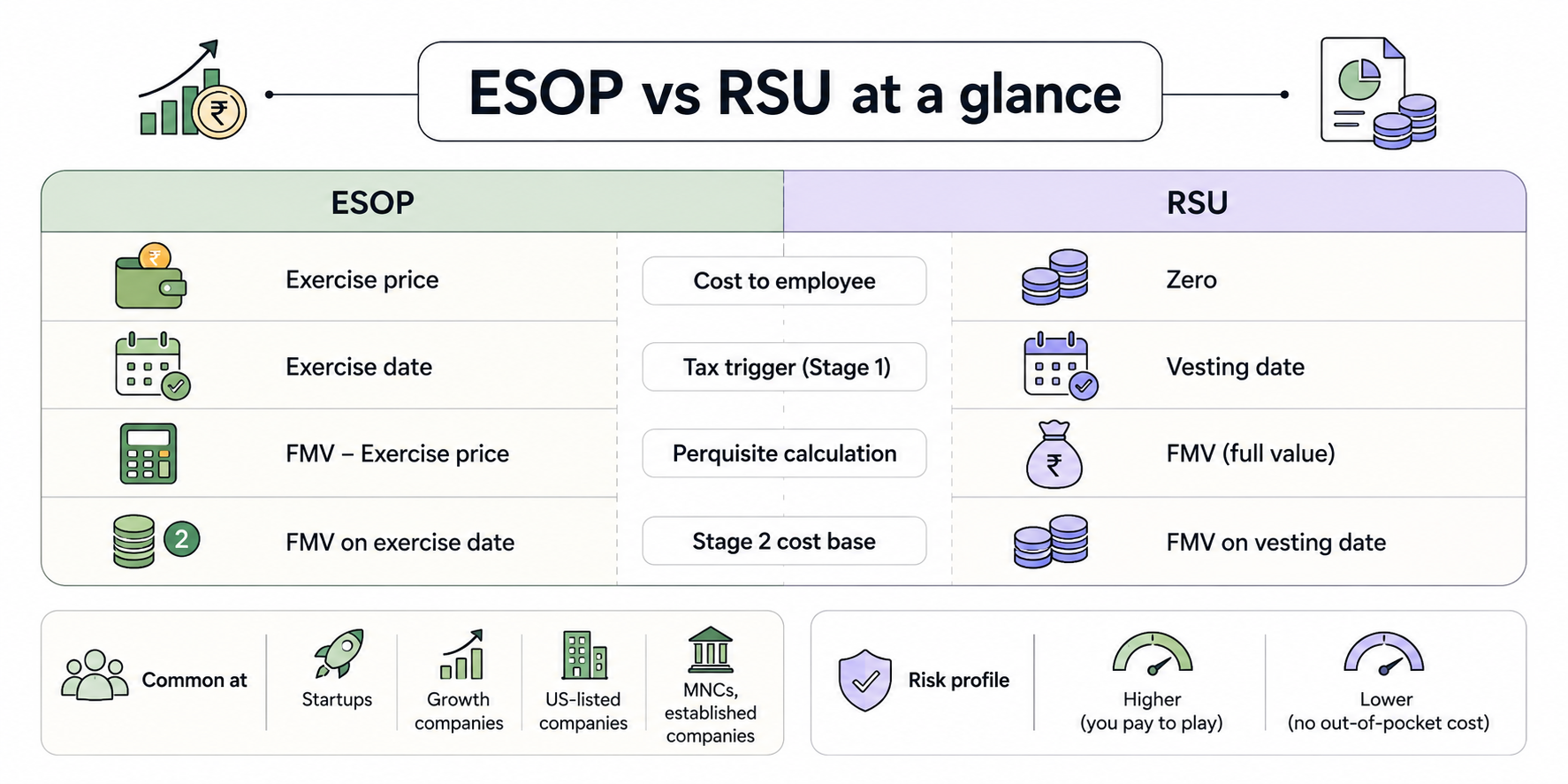

What is ESOP tax in India?

ESOP taxation in India happens in two stages, and most employees only know about the first one.

Stage 1: Perquisite tax at exercise

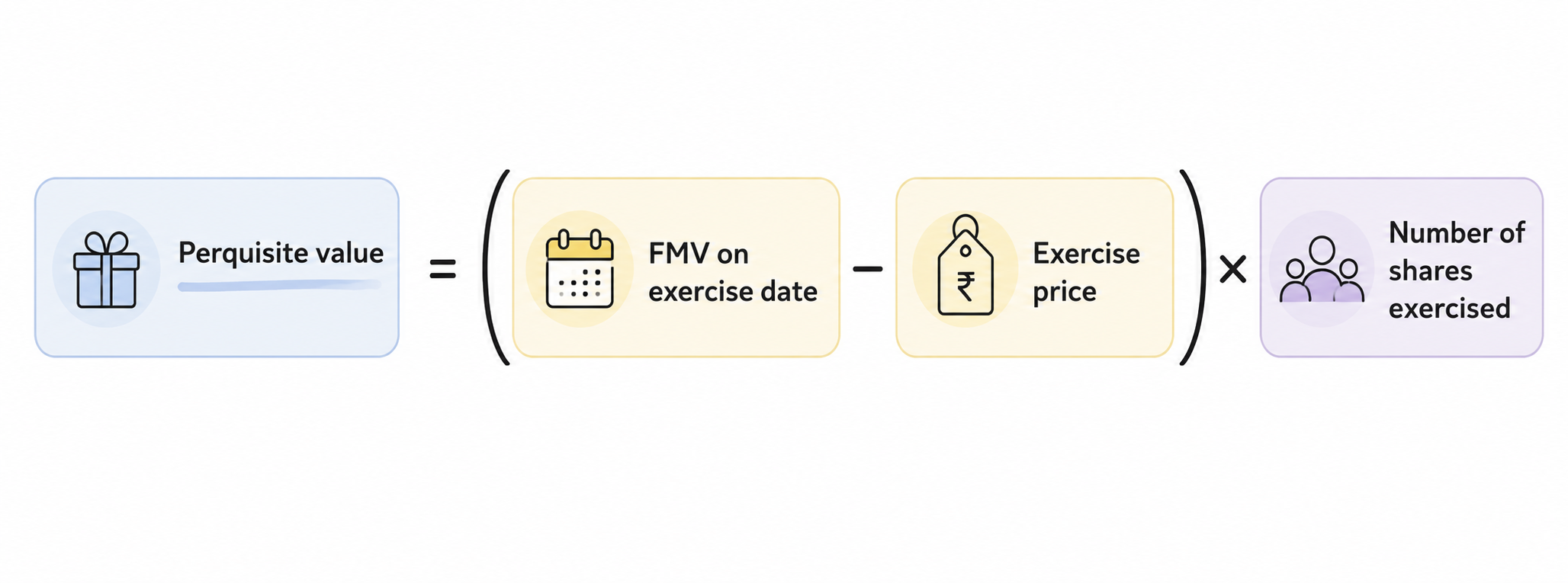

When you exercise your ESOPs, converting your options into actual shares, the difference between the Fair Market Value (FMV) of the shares on the exercise date and your exercise price is treated as a perquisite. A perquisite is a salary benefit. The Income Tax Act adds this amount to your gross salary for the year and taxes it at your slab rate.

Suresh holds 500 ESOPs with an exercise price of ₹100 per share. On exercise day, the FMV is ₹900 per share. The perquisite value is ₹800 × 500 = ₹4,00,000. At a 30% slab, Suresh owes roughly ₹1.2 lakh in tax, even though he hasn't sold a single share.

Your employer deducts this as TDS in the month you exercise, and it shows up in your Form 16. Many employees are blindsided by a much lower salary credit than expected in the exercise month.

Stage 2: Capital gains tax at sale

When you eventually sell those shares, you'll owe capital gains tax on the difference between your sale price and the FMV on the exercise date.

How do RSUs get taxed differently from ESOPs in India?

RSUs (Restricted Stock Units) are simpler in mechanics, but often more expensive in the year of vesting. An RSU is a promise to give you shares at a future date. No exercise price, no payment from your side. The entire FMV at vesting is treated as salary income and taxed at your slab rate.

The simple way to remember it is ESOPs are taxed when you exercise while RSUs are taxed when they vest. There's no exercise step for RSUs because there's no exercise price to pay.

If you work for an Indian subsidiary of a US-listed company and receive RSUs in the parent company's stock, the FMV at vesting is calculated in USD and converted to INR at the RBI reference rate on the vesting date. Two consequences most employees miss:

- Your tax liability moves with the rupee. A weakening rupee inflates your perquisite value in INR.

- You must disclose foreign holdings in Schedule FA of your ITR. Non-disclosure carries penalties under the Black Money Act, even if you owe no additional tax.

An example: A senior engineer at a Hyderabad-based US MNC receives 100 RSUs vesting at $150 per share. At ₹95 to the dollar, FMV is ₹14,250 per share. Total perquisite: ₹14.25 lakh in the year of vesting. At a 30% slab, that's roughly ₹4.3 lakh in tax on shares the employee hasn't sold and may not plan to sell for years.

The tax rules are fixed. The choices you make around them are not.

Decision 1: Exercise early, or wait

If your company is pre-IPO and the current FMV is low, exercising early means a smaller perquisite tax bill. If the company then grows 4× before you sell, all of that additional gain is taxed as capital gains (preferably LTCG at 12.5% on listed shares) rather than as salary income at your slab rate.

A Bengaluru product manager at a Series C startup exercises 1,000 options when FMV is ₹200 against an exercise price of ₹50. Perquisite: ₹1.5 lakh. Tax at 30%: ₹45,000. Two years later, after the company IPO'd and her shares became listed equity, she sold at ₹800. Capital gain: ₹6 lakh, taxed as LTCG at 12.5% on the gain above ₹1.25 lakh, which works out to ₹59,375. Total tax: roughly ₹1.04 lakh on a ₹7.5 lakh gain. Effective rate: 13.9%.

Compare this to waiting until IPO to exercise at ₹800. The entire ₹7.5 lakh is now perquisite, taxed at 30%, which is ₹2.25 lakh. The difference of roughly ₹1.2 lakh stays in your pocket purely by exercising earlier.

The counter-case: exercising costs money. You pay the exercise price and you fund the TDS. If you lack liquidity, or if the company is volatile, early exercise is risky.

Decision 2: Lump-sum, or tranche across financial years

Most ESOP grants vest over 4 years, typically 25% per year. Exercising all four years' worth in a single FY piles the entire perquisite on top of your salary, possibly pushing you into the highest slab even if you were previously in a lower one. Spreading exercise across 2 or 3 FYs can keep some of the gain taxed at 20% rather than 30%.

A senior product lead at a Bengaluru fintech vested ₹35 lakh of ESOPs in FY24-25 and exercised the entire batch in March. The perquisite pushed her into the 30% slab on the top half of her income for the year. Had she split the exercise across March and April, two FYs one month apart, nearly ₹14 lakh would have stayed in the 20% bracket. The decision cost her roughly ₹1.4 lakh in avoidable tax, all from a calendar choice.

Decision 3: Hold 12 months, or sell on day one

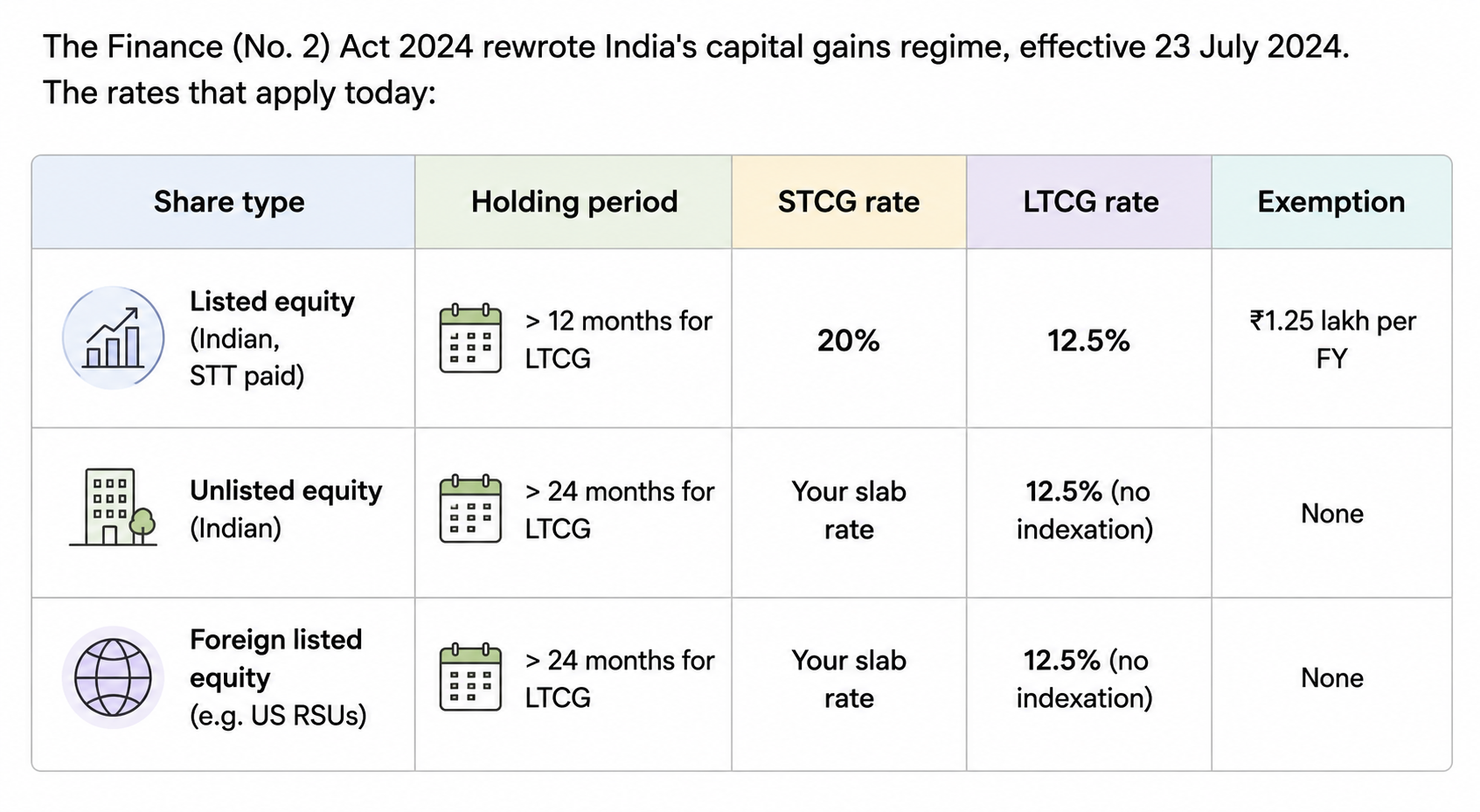

For listed Indian shares, the holding period from exercise to sale determines whether you pay STCG at 20% or LTCG at 12.5% (with ₹1.25 lakh exempt per FY). A one-month delay at exercise can be worth lakhs at sale, purely on tax grounds. For unlisted shares and foreign listed shares like US RSUs, the LTCG threshold is 24 months, not 12.

A Gurgaon engineer at a US-listed MNC sold his RSUs the day they vested in October 2023, treating them like a salary bonus. Two years later, the same shares would have crossed the 24-month foreign-equity LTCG line, except he never gave them the chance. On a ₹22 lakh gain, slab-rate STCG cost him ~₹6.6 lakh. At LTCG, it would have been ₹2.75 lakh. Two years of patience: ₹3.85 lakh.

Decision 4: Concentrate, or diversify

This is the decision the tax rules don't force, but the one that affects your 30-year wealth trajectory the most. A large equity windfall, even well-taxed, leaves your risk profile skewed if you redeploy it poorly into a concentrated position in one stock.

A Hyderabad data scientist held every vested RSU from her US employer through a four-year run, untouched. The stock tripled, then dropped 60% during a sector correction. She optimised every tax decision on the way in. None of it mattered once the position halved while still concentrated. Diversifying even 40% of the post-tax proceeds into a broad index would have cushioned almost the entire drawdown.

The after-tax proceeds matter only insofar as you redeploy them well. This is where most ESOP guides stop, and where good financial planning begins.

The five mistakes Indian employees make, ranked by cost

- Exercising everything in one FY because it feels simpler. Pushes you into the highest slab. Easily ₹5 to ₹10 lakh of avoidable tax on a meaningful grant.

- Selling within 12 months because the shares feel like found money. Triggers 20% STCG when 12 more months would have dropped most of the gain to 12.5% LTCG.

- Not setting aside cash for TDS before exercising. Forces a panic sale that destroys the holding period strategy entirely.

- Forgetting Schedule FA for foreign RSUs. Black Money Act penalties can be punitive, even when no additional tax is owed.

- Optimizing every tax decision, then leaving everything in employer stock. The biggest long-term wealth destroyer. The tax saved is irrelevant if the concentrated position then halves.

Every one of these five mistakes shares a single root cause: the decision was made without seeing the full after-tax picture. The slab math, the holding period math, the rupee math, the concentration math — they each look manageable in isolation. Stack them together across a real grant, across a real career, and the cost compounds quickly.

This is the gap Armor's Scenario Sandbox closes.

Where Armor's Scenario Sandbox fits

The Sandbox takes your specific grant — vesting schedule, exercise price, current FMV, expected sale price — and returns your after-tax proceeds across different exercise-and-hold strategies, ranked by net wealth impact at age 60. It accounts for the perquisite hit, the LTCG vs STCG split, the slab-stacking effect of single-FY exercise, the rupee-dollar movement on US RSUs, and the cost of holding concentrated stock instead of diversifying.

Most employees who run the simulation discover the optimal strategy is meaningfully different from what they had assumed. The difference between a well-planned exercise strategy and an ad-hoc one is usually between ₹5 and ₹15 lakh in tax saved on the same underlying shares.

Stress-test your equity grant at yourarmor.ai/scenario-sandbox

Frequently Asked Questions (FAQ’s)

1.What is ESOP taxation in India?

ESOP taxation in India happens in two stages. First, when you exercise options, the difference between the Fair Market Value and your exercise price is taxed as salary income at your applicable slab rate (up to 30%). Second, when you sell, the gain from FMV at exercise to sale price is taxed as capital gains, STCG at 20% if sold within 12 months, LTCG at 12.5% above ₹1.25 lakh if held longer (for listed Indian equity, post 23 July 2024 rates).

2.How does ESOP tax work in India when you exercise?

When you exercise ESOPs, your employer calculates the perquisite value, the FMV on exercise date minus your exercise price, multiplied by shares exercised. This amount is added to your gross salary for the year and taxed at your income tax slab. Your employer deducts TDS from your salary in the same month. This can significantly reduce or eliminate your salary credit in an exercise month.

3. How much tax will I pay on my ESOPs in India?

It depends on two things: the perquisite value at exercise (taxed at your slab rate, typically 20–30%) and the capital gains at sale (STCG at 20% or LTCG at 12.5% above ₹1.25 lakh, depending on holding period and share type). For a ₹10 lakh perquisite gain, expect roughly ₹3-3.12 lakh in tax at exercise. Additional capital gains tax applies when you sell, based on price movement after exercise.

4. Is it better to exercise ESOPs early or wait for the IPO in India?

For most employees at high-growth startups, exercising early when the FMV is still low minimises the perquisite tax and allows future appreciation to be taxed as LTCG (12.5%) instead of salary income (30%). However, early exercise requires liquidity to pay exercise costs and fund TDS, and carries risk if the company's valuation falls. The right answer depends on your specific company stage, grant details, and cash position.

5. What happens if I exercise my ESOPs but can't pay the tax bill in India?

If you exercise ESOPs and cannot fund the TDS from your salary or savings, your employer may recover the tax from consecutive payroll credits. This can result in zero salary for one or more months. In extreme cases, you may need to sell some shares to fund the tax, eliminating the holding period advantage. Always model the cash flow impact before exercising, especially for large grants.

6. How are RSUs taxed in India?

RSUs are taxed in two stages, but the trigger is different from ESOPs. At vesting, the full Fair Market Value of the vested shares is treated as salary income and taxed at your slab rate, with TDS deducted by your employer. There is no exercise step because RSUs have no exercise price. When you eventually sell, any gain over the FMV-at-vesting is taxed as capital gains, 20% STCG within 12 months (listed Indian) or 24 months (foreign listed), 12.5% LTCG beyond those thresholds.

7. How are US RSUs taxed for Indian employees?

If you work for an Indian subsidiary of a US-listed company and receive RSUs in the parent's stock, the FMV at vesting is calculated in USD and converted to INR using the RBI reference rate on the vesting date. This INR-equivalent amount is added to your salary for the year and taxed at your slab rate. When you sell, capital gains apply, 20% STCG within 24 months, 12.5% LTCG beyond. You must also disclose the foreign holdings in Schedule FA of your ITR. DTAA relief is available against any US tax withheld.