Financial Freedom Blueprint : A 7-Step Architecture for Indian Families

Financial Planning · 15 Apr 2026 · Team Armor

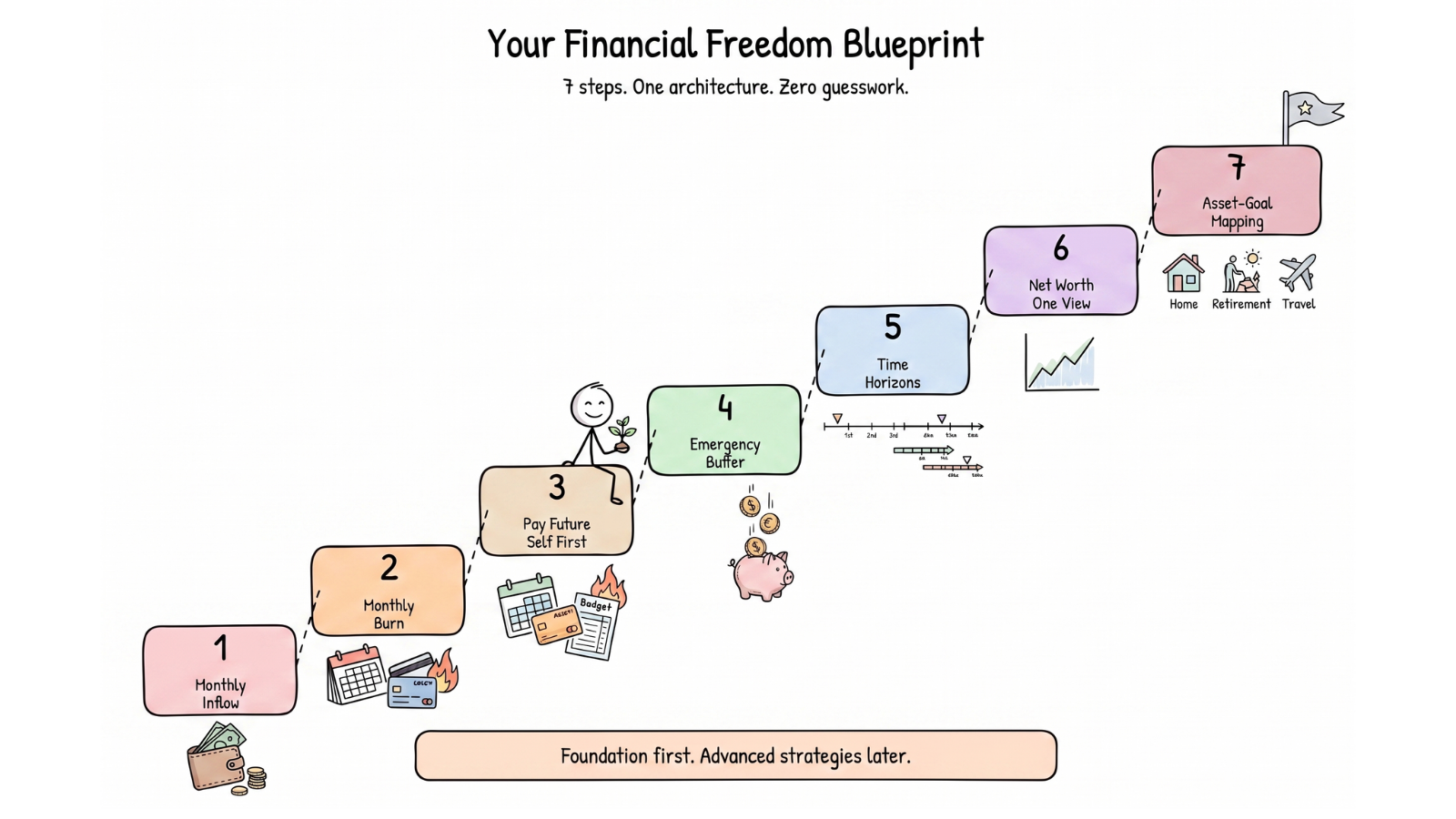

Wealth is rarely built on a lucky gamble. It is architected through a deliberate, plan-first approach. At Armor, we have distilled the core of personal finance into 7 foundational steps: know your inflow, know your burn, pay your future self first, build a life-stage buffer, separate your time horizons, see your net worth in one view, and map every asset to a goal. Get these right and you have solved 80% of the problem.

In the noisy world filled with "hot stocks," overnight crypto stories, and that one relative who made 100% in small-caps, it is easy to feel like you are falling behind.

We see this constantly where users come to us after months of financial anxiety, convinced that they need some advanced strategy or hidden formula. The truth? For most Indian families, wealth is not built on a lucky gamble. It is architected through 7 boring yet brutally effective steps.

True financial intelligence is not about predicting the next market crash. It is about knowing your numbers, building a safety net that actually holds, and giving every rupee a specific job. Once these fundamentals are in place, the "advanced strategies" become optional. Not urgent.

Step 1: Identify Your Starting Engine (Monthly Inflow)

Before you look at a single mutual fund factsheet, you need one clear number: how much actually comes in every month?

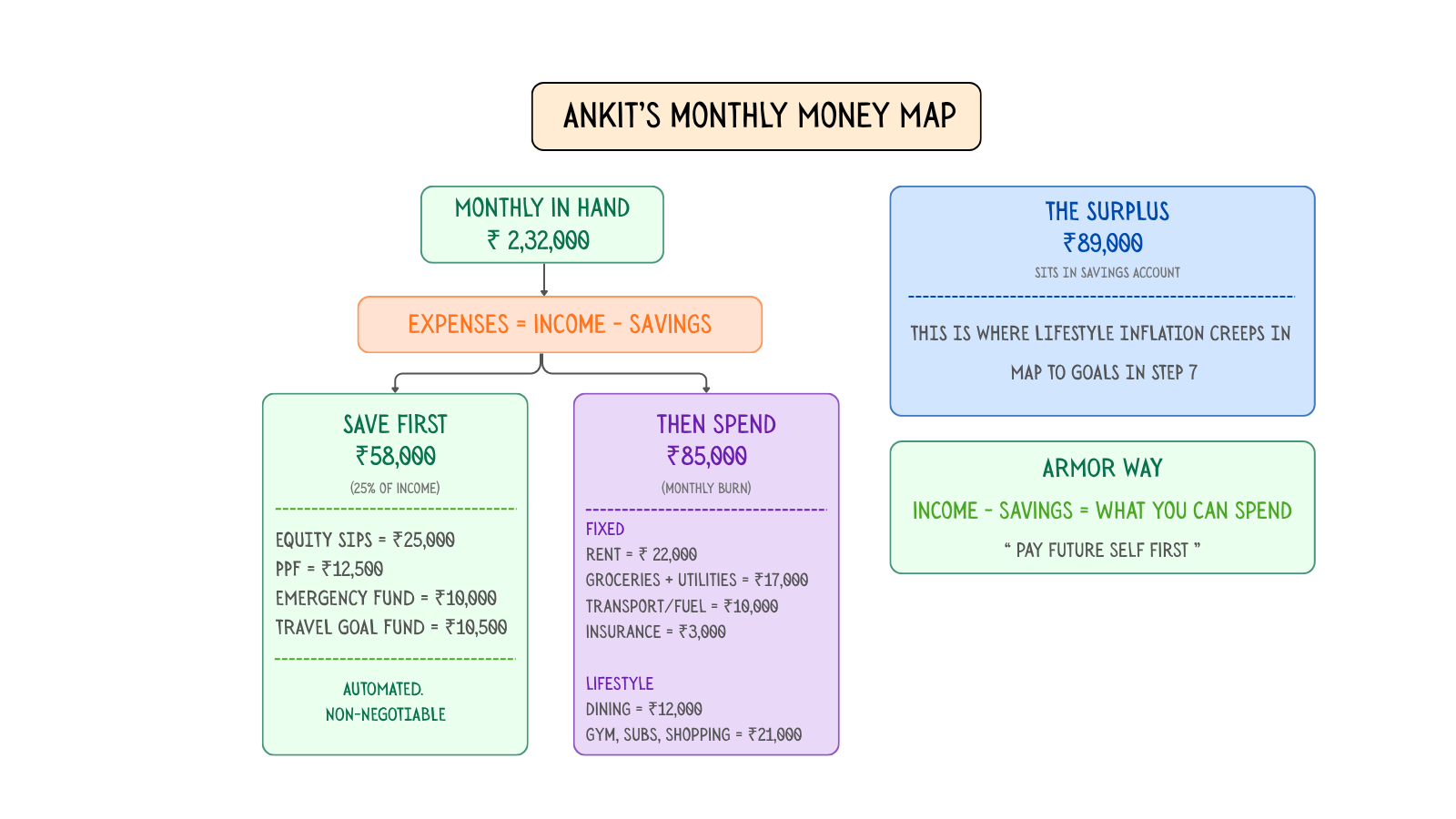

Take Ankit. He is 29, works as a senior data analyst at a tech firm in Hyderabad, earns a fixed salary of ₹1,62,000 per month in-hand, and picks up about ₹70,000 in freelance consulting on average. His "starting engine" is ₹2,32,000 per month.

The trap most people fall into is to use their best month as their baseline. That one month with a big variable pay or a freelance windfall becomes the mental anchor. Do not do this. Use your average monthly inflow over the last 12 months. That is the fuel that powers your entire financial life.

Step 2: Calculate Your Monthly Burn (Real Expenses)

The most dangerous thing a working professional can do is fly blind on spending. You have to know exactly what it costs to live your life for 30 days. Here is why this matters: if you do not know this number, you cannot calculate how much financial freedom you actually have. You are guessing and guessing with money is expensive.

Ankit breaks his expenses into two buckets.

Fixed costs: Rent for a 2BHK in Kondapur at ₹22,000. Groceries and utilities at ₹17,000. Transport and fuel at ₹10,000. Insurance premiums at ₹3,000. Subtotal: ₹52,000.

Lifestyle choices: Dining out and food delivery at ₹12,000. Gym, subscriptions, shopping, and weekend plans at ₹21,000. Subtotal: ₹33,000.

Ankit's monthly burn: ₹85,000.

That leaves a surplus of about ₹89,000 sitting in his savings account every month. And here is the uncomfortable truth: for high-income earners, this surplus is exactly where lifestyle inflation creeps in. A slightly nicer apartment. A more expensive car. An unplanned trip. Without a system, this money vanishes without ever being invested.

Step 3: Pay Your Future Self First (Savings Rate)

This is where most people get the formula backwards.

The conventional approach is: Income - Expenses = Whatever is left for savings.

The problem? Nothing is ever left.

At Armor, we flip it. Income - Savings = Expenses.

That is the identity. Treat your investments as a fixed bill that must be paid on the 5th of every month via an automated SIP. Not at the end of the month. Not "if there is something left." On the 5th. Like rent.

Ankit sets aside 58,000 per month, roughly 25% of his income, before he spends a single rupee on anything else. That ₹58,000 splits into: ₹25,000 in equity SIPs, ₹12,500 into PPF, ₹10,000 toward building his emergency fund, and ₹10,500 into a short-term goal fund earmarked for travel.

The percentage will vary by income, age, and commitments. But the principle does not change. Your savings rate is the single most powerful lever in your financial life. Not returns. Not stock-picking. The rate at which you set money aside.

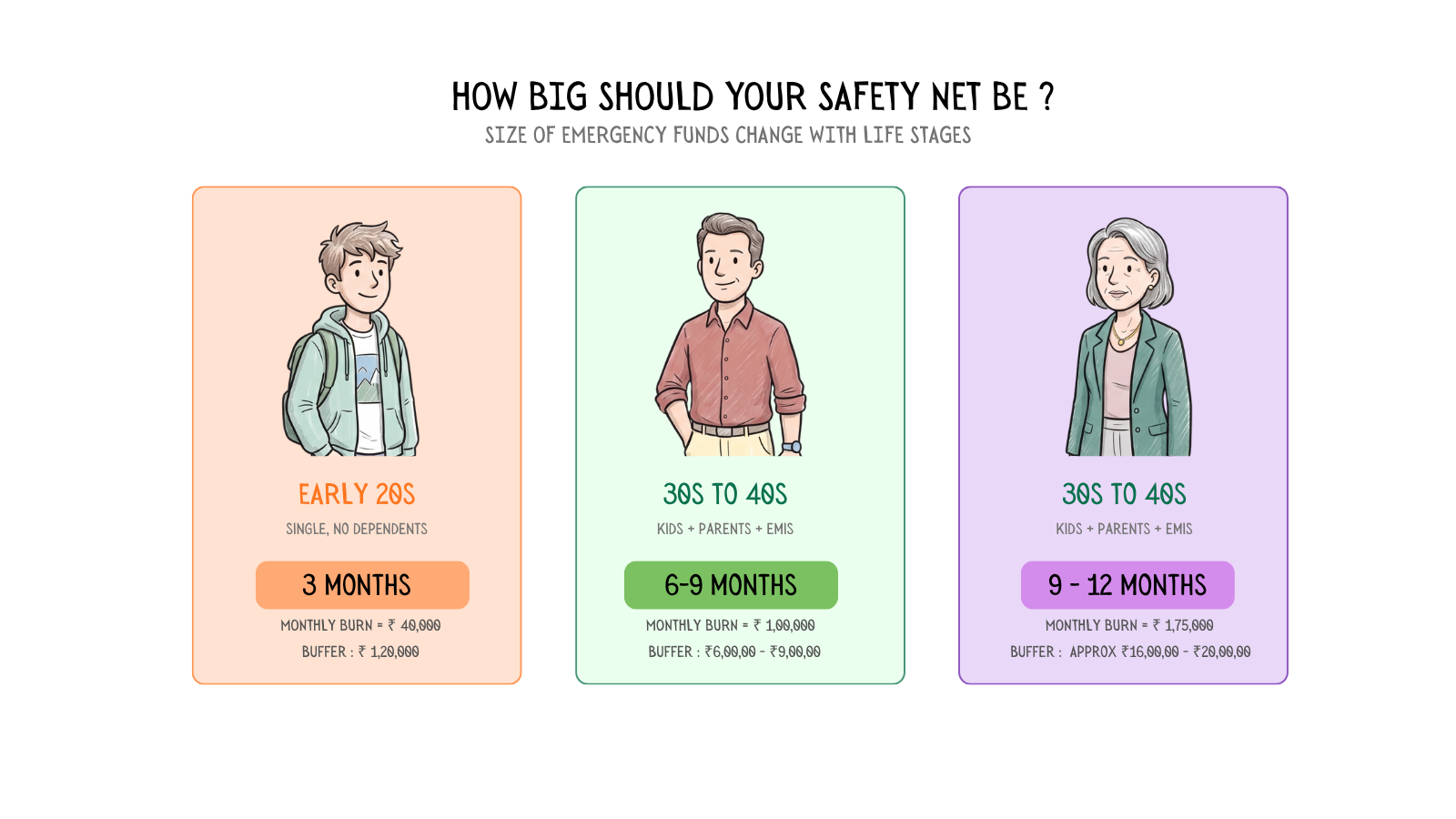

Step 4: Build a Life-Stage Buffer (Emergency Fund)

Ankit has not built his buffer yet. What happens if his freelance income dries up for two months?

An emergency fund is the most boring asset you will ever own. It sits in a savings account or a short-term FD doing almost nothing. Until the day you need it, and then it becomes the most beautiful thing you own.

We see this pattern repeatedly. Someone loses a job, faces a medical emergency, or needs to relocate suddenly. Those with a buffer handle it calmly. Those without it start liquidating investments at the worst possible time, often at a loss.

The size of your buffer should match your life stage. In your early 20s, when you are single with no dependents, 3 months of expenses is a solid floor. In your 30s and 40s, when you have kids, parents, and an EMI, you need 6 to 9 months. In your late 40s with high EMIs and peak expenses, stretch it to 9 to 12 months.

The image above gives you the exact numbers by life stage.

Keep this money in high-liquidity, low-risk instruments. Not equity. Not gold. Something you can access in 24 hours without taking a loss.

Step 5: Categorize Your Horizons (Short vs. Long Term)

Stop viewing your money as one big undifferentiated pile. Give it a timeline so you can choose the right vehicle for the journey.

This is where Vikram, a 33-year-old product designer in Pune, was going wrong. He had 4 lakhs earmarked for a car down payment in 18 months sitting in a mid-cap equity fund. One bad quarter and his "car fund" dropped 12%. The money needed a shorter time horizon instrument.

Here is the framework:

Short-term goals (0 to 2 years): Things like vacations, gadgets, or a wedding, belong in liquid funds. Do not gamble this money in the stock market.

Medium-term goals (2 to 5 years): Things like a car or house down payment, go into a blend of debt funds and conservative hybrid funds.

Long-term goals (5+ years): Things like children's higher education or retirement, are where equity exposure makes sense to beat inflation.

The instrument is not the strategy. The time horizon is the strategy.

We have covered this in more detail in our guide on Financial Goal Setting in India: A 5-Step Plan to Turn Intentions Into Action, where we break down exactly which goals belong at which stage of your life and how to prioritise between them.

Step 6: The One View (Net Worth Sheet)

Most Indian families have money scattered everywhere. EPF in one corner, FDs in another, some gold jewellery, a couple of bank accounts, maybe a few direct stocks bought during the 2020 rally. The result is a scattered, invisible financial picture. You cannot manage what you cannot see.

At Armor, the first thing we do is consolidate everything into a single view. All assets, all liabilities, one number: your net worth.

Priya, a 38-year-old architect in Chennai, discovered something uncomfortable when she did this exercise: 65% of her wealth was locked up in real estate, and barely 8% was in equity. She was asset-rich but liquidity-poor. That single view changed every decision she made from that point forward. It is the most underrated step in this entire blueprint.

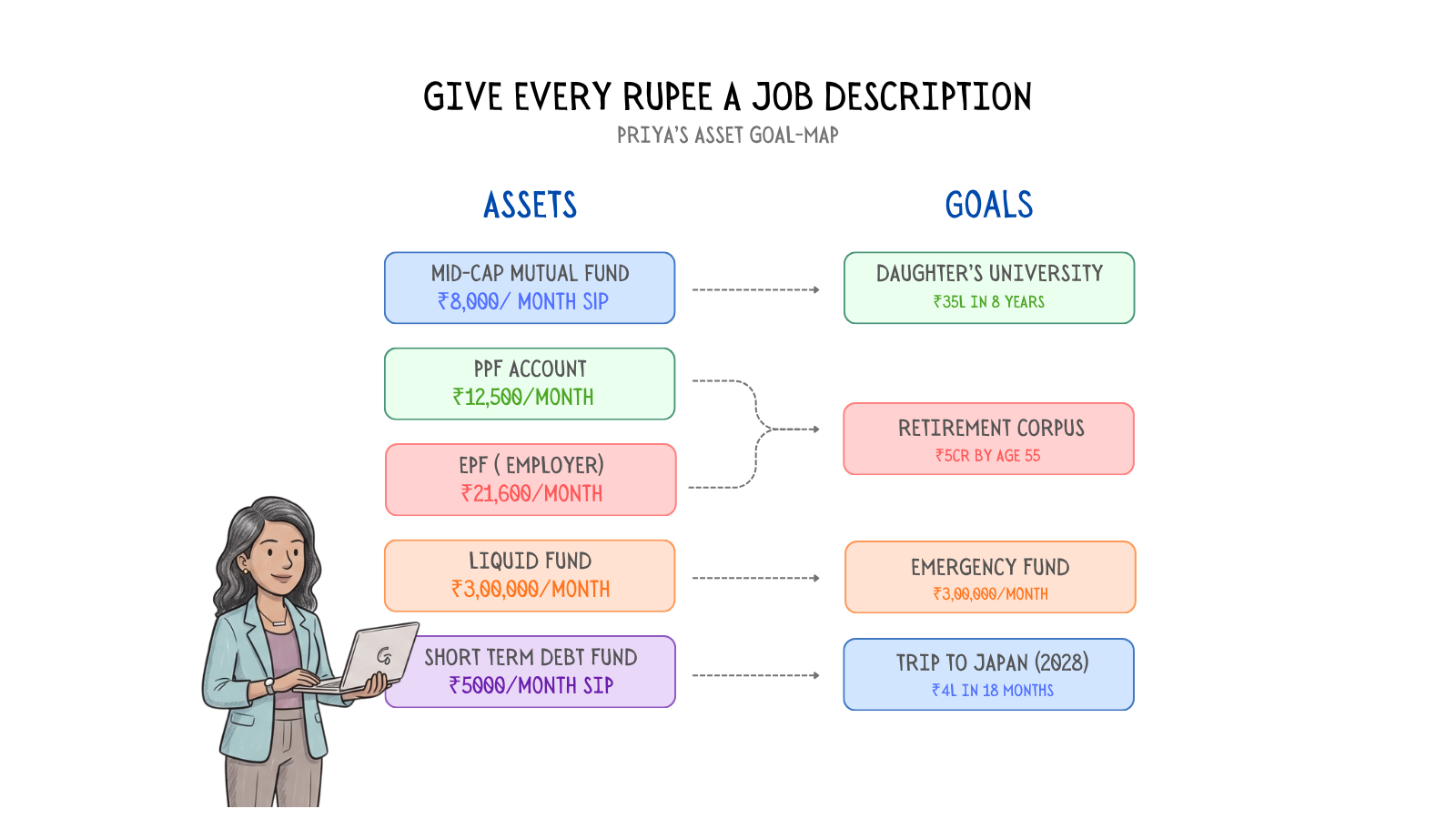

Step 7: Connect the Dots (Asset-Goal Mapping)

The final step is the most rewarding. Every SIP, every FD, every EPF contribution gets assigned to a specific goal.

Priya's mid-cap SIP is not "mutual fund 1." It is her daughter's university fund. Her PPF and EPF feed into her retirement corpus. Her liquid fund is the emergency buffer. Her short-term debt fund is the family trip to Japan in 2027.

When your money has a name, you do not touch it for the wrong reasons. You stop dipping into the "education fund" for a phone upgrade. You stop redeeming the "retirement SIP" for a car accessory. Each rupee knows its job.

For long-term goals like retirement, work backward: estimate your cost of living 20 years from now (adjusting for 7 to 10% inflation), determine your Freedom Number, and check if your current monthly investment gets you there. If not, Armor shows you exactly how much more you need to bridge the gap.

The Bottom Line

Getting these 7 steps right is 80% of the battle. Not 100%. Eighty.

The goal is not perfection. It is moving from "I have no idea where my money goes" to "I have a working plan and every rupee has a job." When your foundation is set, you stop reacting to market noise, stop following LinkedIn stock tips, and start trusting the system you built.

Advanced strategies? They become a choice, not a necessity. And that is exactly what financial freedom feels like.

FAQ SECTION

What is a financial freedom blueprint?

A financial freedom blueprint is a structured, step-by-step plan that covers the core pillars of personal finance: knowing your income, tracking your expenses, automating savings, building an emergency fund, aligning investments with time horizons, tracking your net worth, and mapping every asset to a specific life goal. It provides the foundation needed before any advanced investing strategy.

How much should I save from my salary in India?

A good starting target is 20 to 25% of your in-hand salary. The exact percentage depends on your age, income, and commitments. Someone in their 20s with no dependants can aim higher; someone in their 30s managing EMIs and family expenses might start at 15% and scale up. The critical principle is to treat savings as a fixed monthly bill, not a residual amount.

What is the "Income minus Savings equals Expenses" rule?

It is the inversion of how most people budget. Instead of saving whatever is left after spending, you first deduct your savings (via automated SIPs set on the 5th of the month), and then spend from what remains. This one behavioral shift changes everything because it guarantees that your future self gets paid before your current self overspends.

How big should my emergency fund be in India?

It depends on your life stage. Singles in their early 20s should target 3 months of expenses. Professionals in their 30s and 40s with dependants, EMIs, and family obligations should hold 6 to 9 months. People in their late 40s with high fixed expenses should aim for 9 to 12 months. Keep this in liquid, low-risk instruments like high-yield savings accounts, short-term FDs, or liquid mutual funds.

What is asset-goal mapping and why does it matter?

Asset-goal mapping means assigning every investment to a specific life goal: your SIP is not "Fund A," it is your "daughter's university fund" or your "retirement corpus." It matters because it prevents impulsive withdrawals, creates emotional accountability, and gives you a clear way to track whether each goal is on track. When money has a name, you protect it differently.

How do I calculate my net worth?

Add up all your assets: bank balances, mutual funds, stocks, EPF, PPF, real estate market value, gold, and any other holdings. Then subtract all liabilities: home loan outstanding, car loan, credit card debt, personal loans. The resulting number is your net worth. Review it quarterly to track progress and catch imbalances, like being over-concentrated in real estate or under-allocated to equity.

What are the best instruments for short-term vs long-term goals in India?

For short-term goals (0 to 2 years), use liquid funds or ultra-short-term debt funds. For medium-term goals (2 to 5 years), consider conservative hybrid funds or balanced advantage funds. For long-term goals (5+ years), equity mutual funds, index funds, and PPF give you the growth needed to beat inflation. The instrument follows the timeline, not the other way around.