The Math Behind Your Money: What Your School Skipped

Investing · 21 May 2026 · Team Armor

If you've started a SIP without fully understanding what's happening underneath it, you're in good company. This post walks through the five return concepts every new Indian investor should know - simple interest, compound interest, absolute return, CAGR, and XIRR with worked examples, clean formulas, and one table that answers most of the questions you'll have.

9.72 crore Indians now run a monthly SIP. In March 2026, monthly SIP contributions crossed ₹32,000 crore for the first time, hitting ₹32,087 crore (Source: AMFI Monthly Note, March 2026, page 16). And yet, if you asked most of those investors what their XIRR actually measures, or whether their 12% return is genuinely good after inflation, you'd get a pause.

The math behind personal finance was never taught in school. We learnt compound interest but not how compounding actually behaves, what CAGR measures, or why time matters more than rate. This is the blog that fills that gap.

What is simple and compound interest?

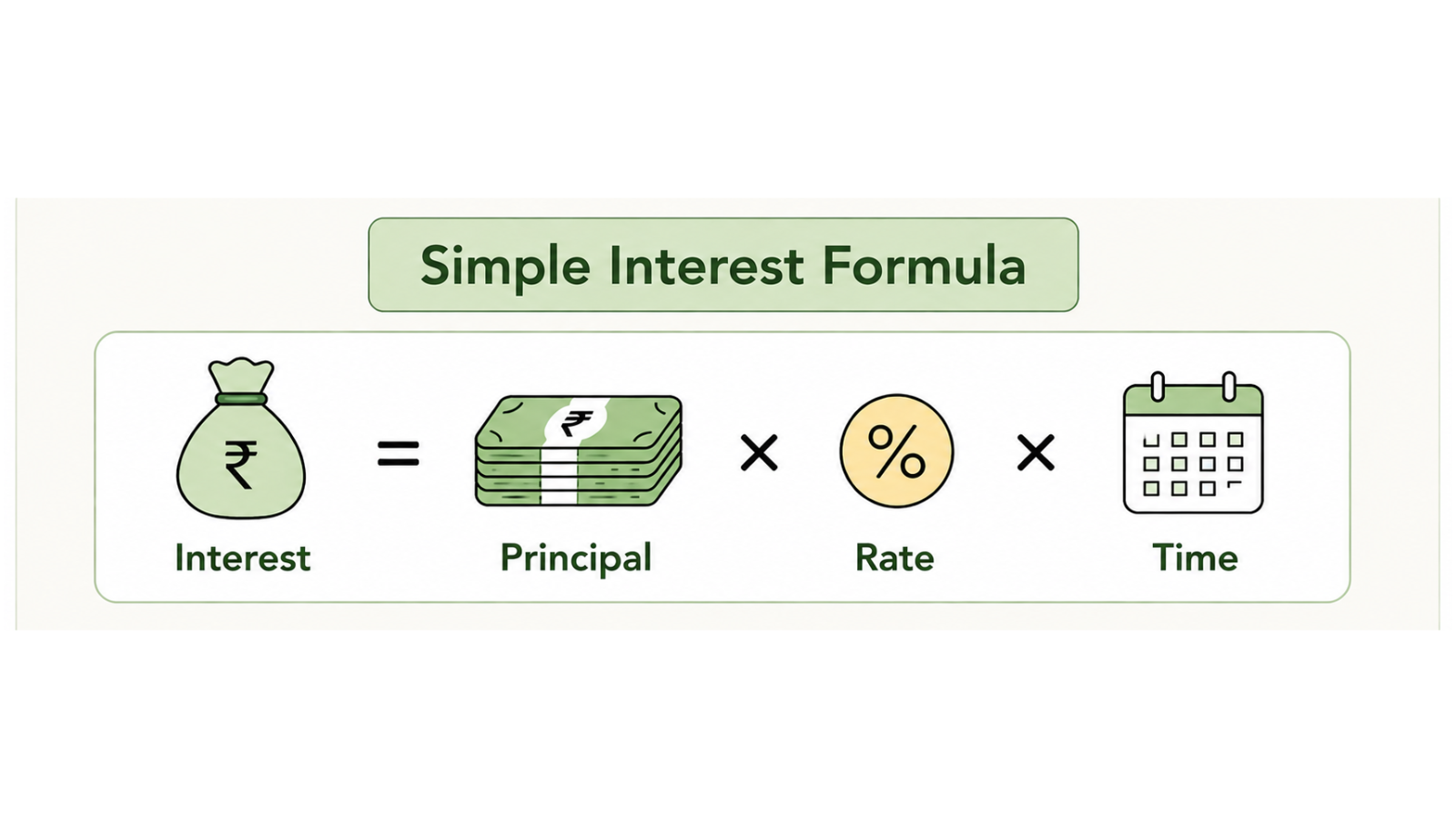

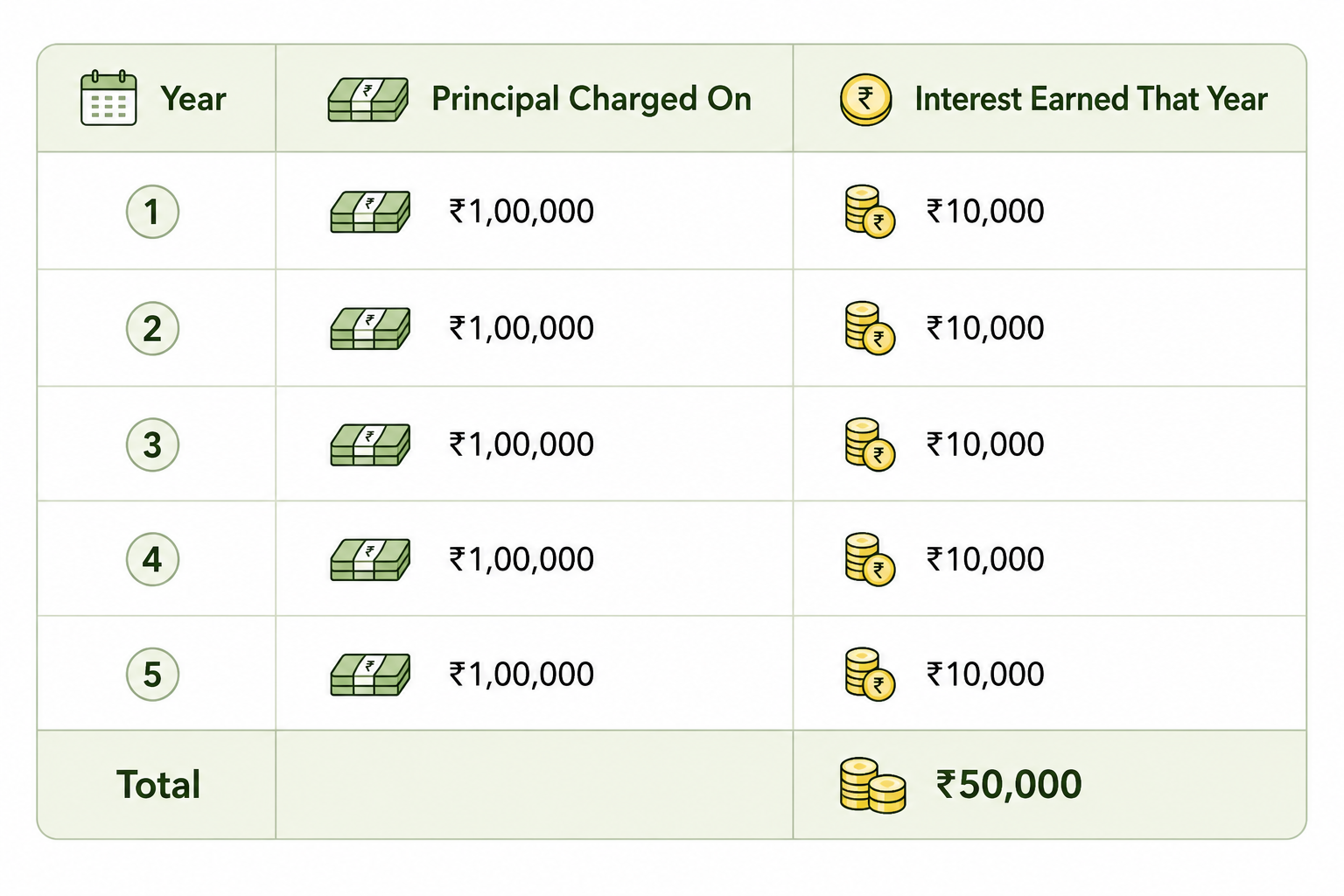

Let’s start with the basics. Simple interest is calculated on the original principal only, the base amount never changes for interest purposes. Every year, you earn exactly the same rupee amount in interest regardless of how long the investment runs.

So let’s say,

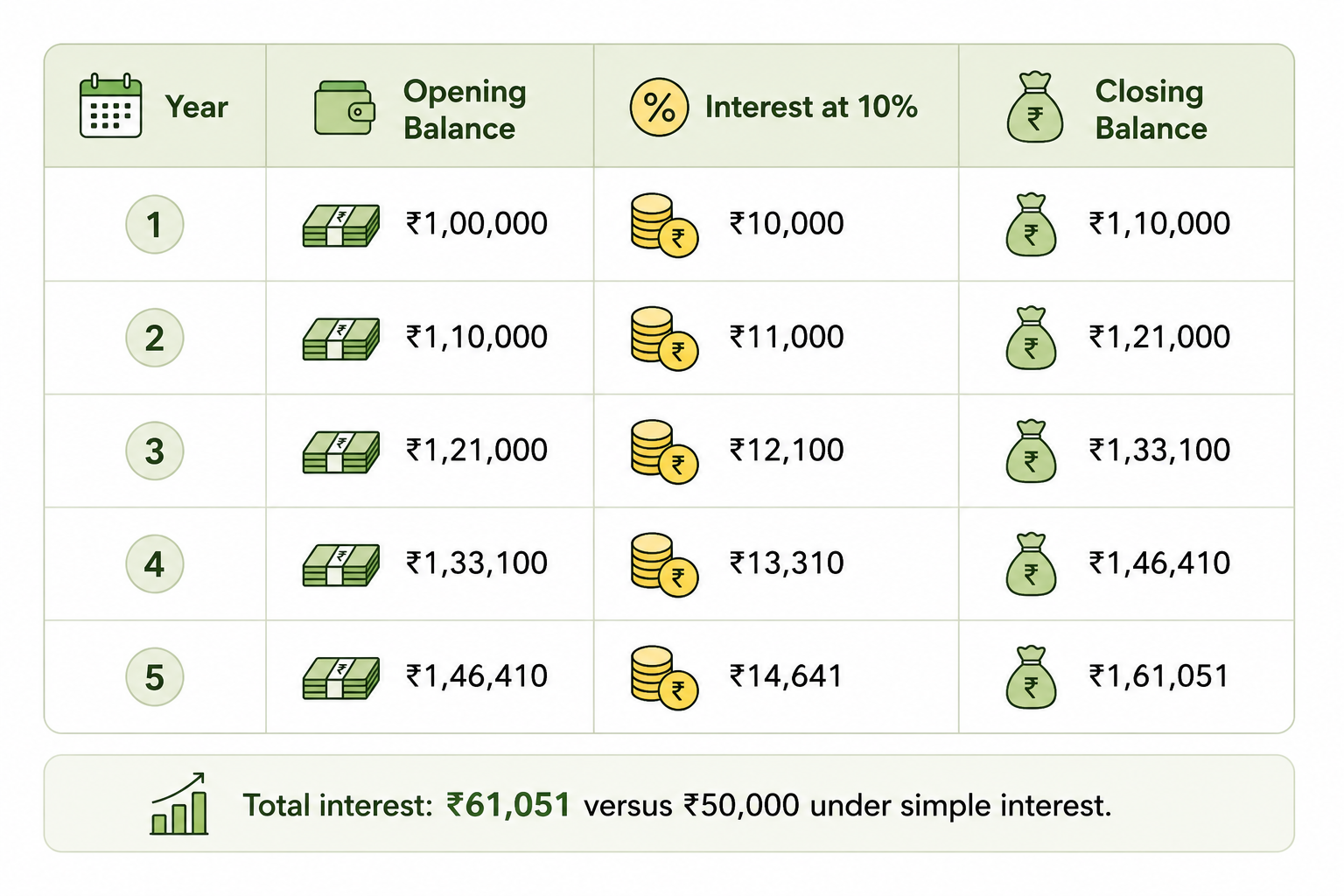

You lend a colleague in Chennai ₹1,00,000 at 10% per year. Under simple interest, you earn ₹10,000 every year and a flat ₹50,000 over 5 years, ₹2,00,000 over 20 years.

Simple interest is predictable and easy to calculate but it's also slow because the ₹10,000 you earn in year 1 never starts earning for you. It sits idle while the original ₹1,00,000 keeps doing all the work.

On the other hand, compound interest is interest calculated on the principal plus all the interest already earned.

Each year, the previous year's interest gets folded into the new starting balance and the next year's interest is calculated on that larger number. Most people understand compounding in theory. They don't feel it.

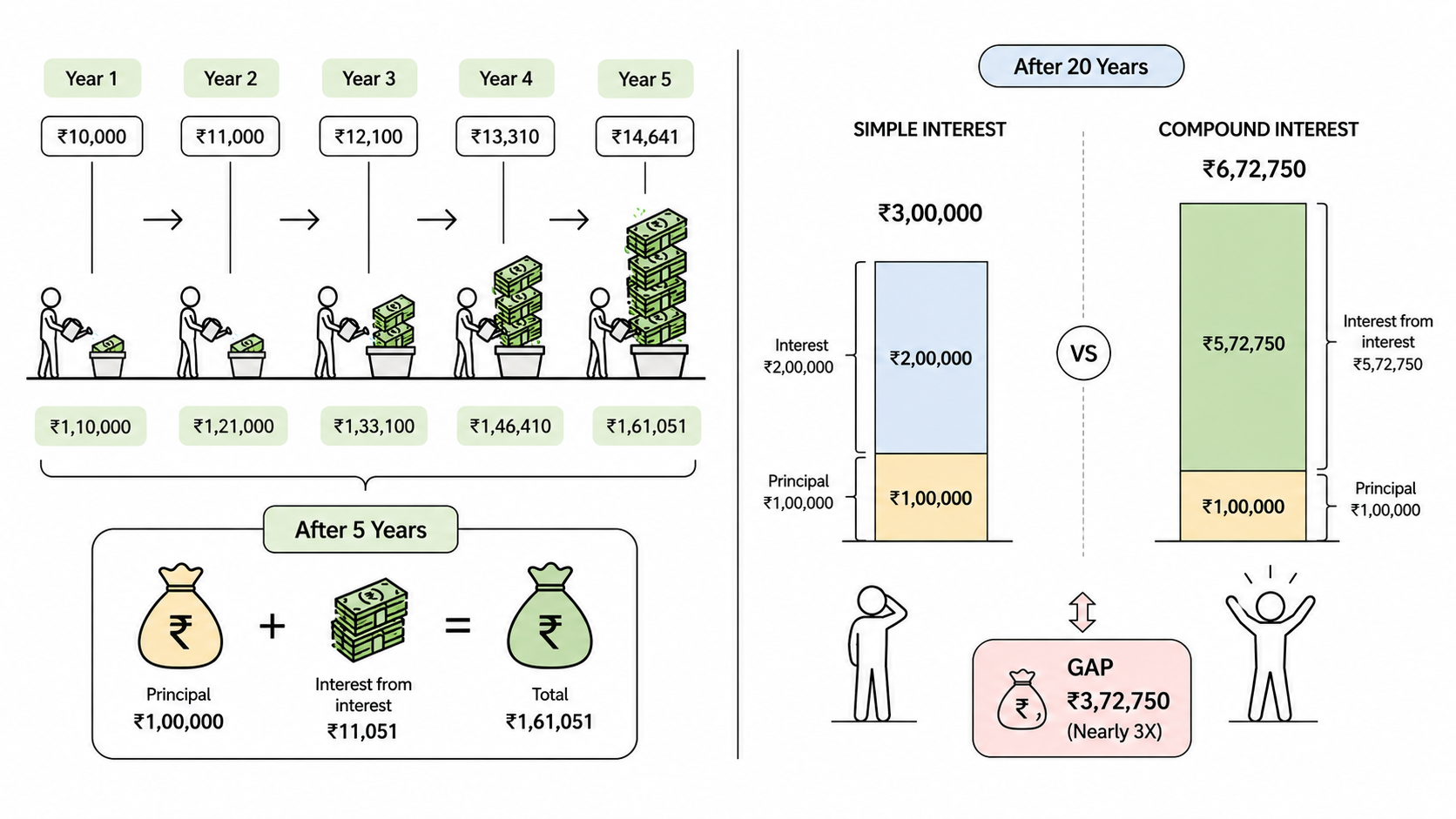

If we were to consider the same example, under compound interest, each year's interest earns its own interest. After 5 years you've earned ₹61,051. After 20 years you've earned ₹5,72,750. Same money, same rate, same time. Nearly triple.

Every SIP, every PPF, every long-held mutual fund grows this way by default. You don't have to do anything to compound. You just have to not interrupt it.

What is Absolute Returns, CAGR and XIRR?

Notice how the mutual fund apps show you a return number?

You feel good seeing it but the number you're reading often misrepresents what your money is actually doing.

There are three return figures every individual who is investing should be able to tell apart.

1. Absolute Return

Absolute return is the total percentage gain on an investment from start to end, with no adjustment for how long it took. It is the right measure only for investments held for less than one year.

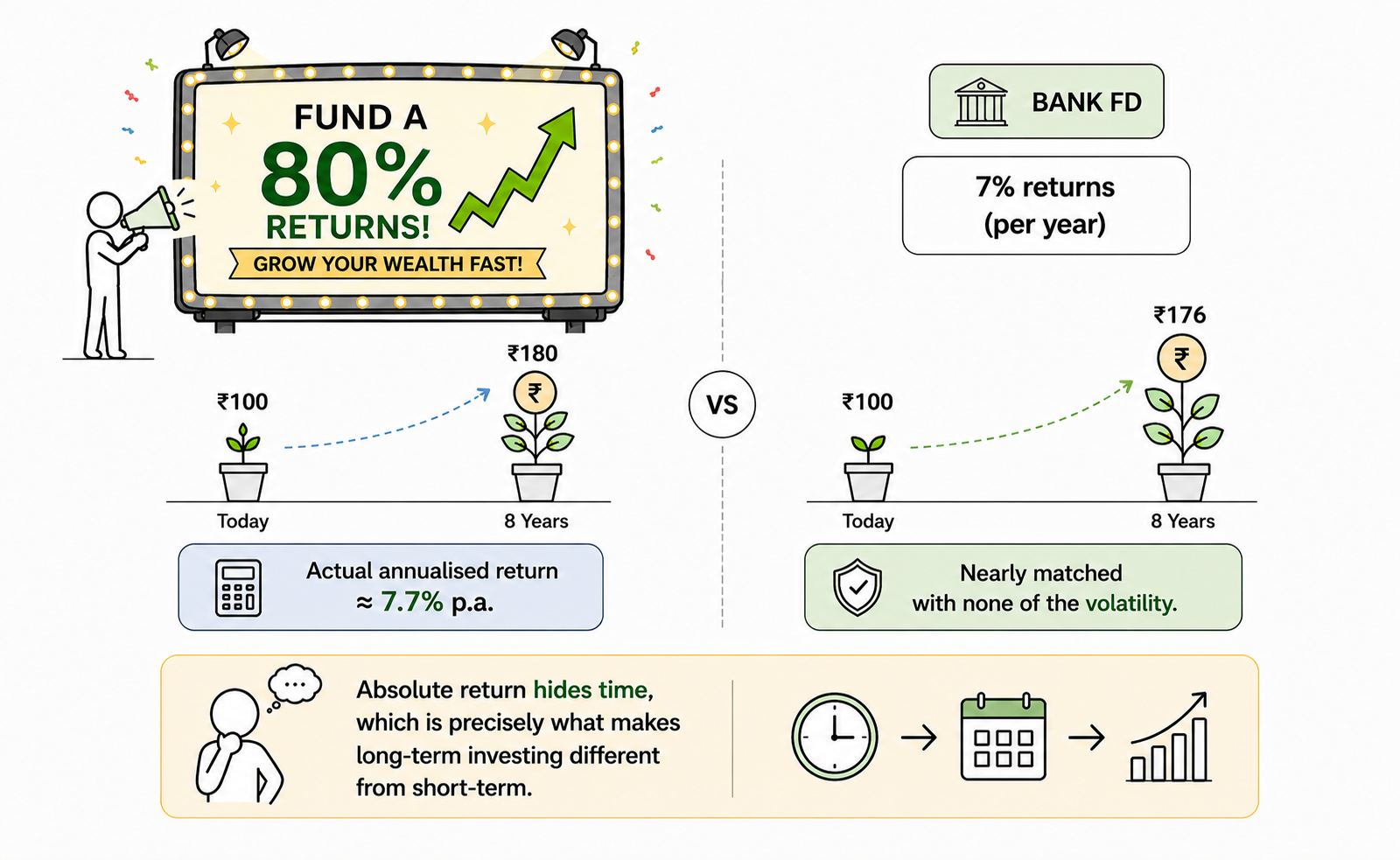

That fund is annualising at 7.7% but an FD at 7% would have nearly matched it, with none of the volatility. Absolute return hides time, which is precisely what makes long-term investing different from short-term.

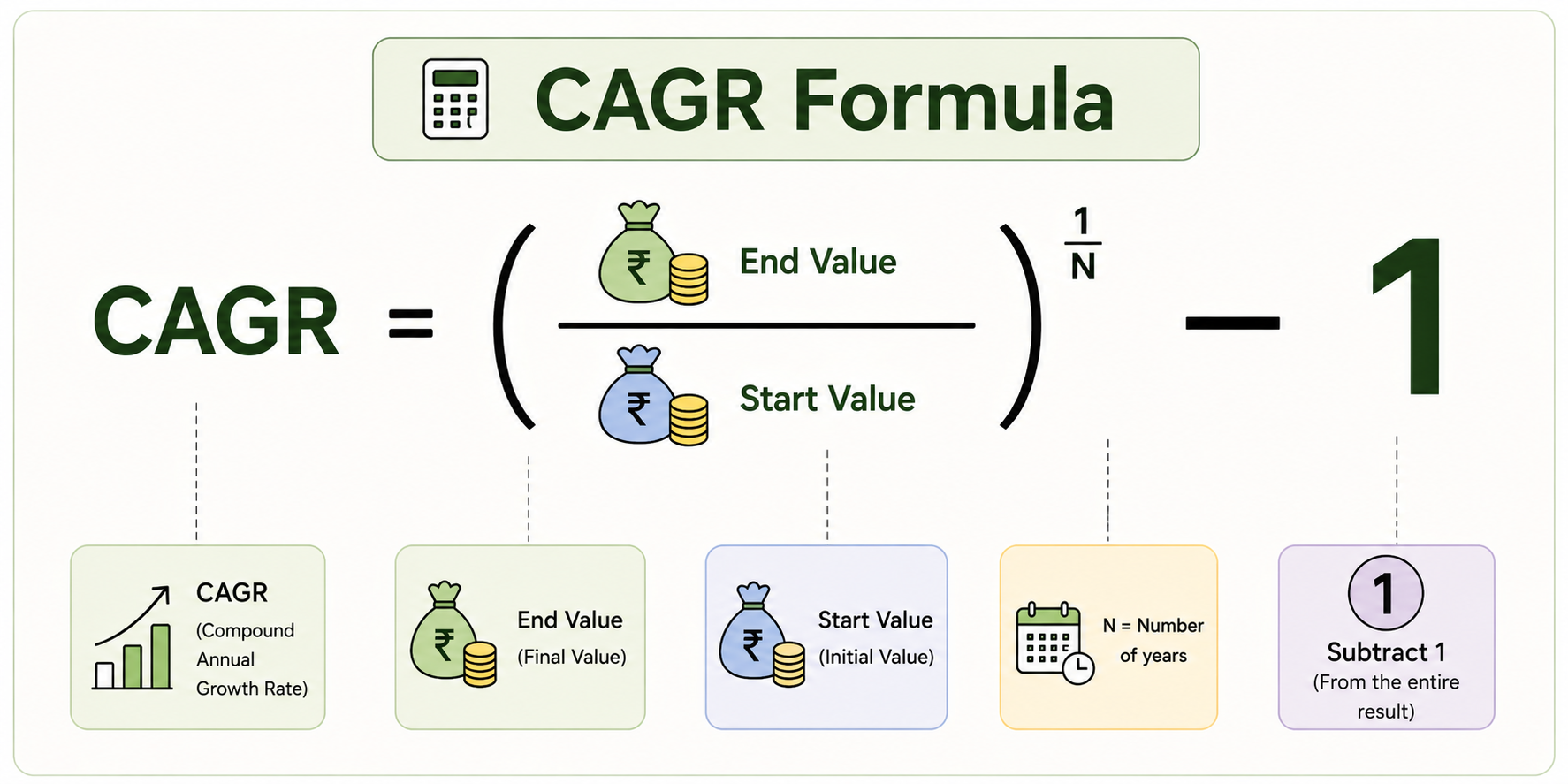

2. CAGR (Compounded Annual Growth Rate)

CAGR (Compounded Annual Growth Rate) is the single annual rate at which your investment grew, smoothed out across all the ups and downs in between. It is the standard measure for any investment held for more than one year in India.

Let’s say, a 34-year-old in Mumbai invested ₹1,00,000 in an equity mutual fund in 2020. In 2025, it's worth ₹1,61,051.

CAGR = (1,61,051 / 1,00,000)^(1/5) − 1 = 10% per year.

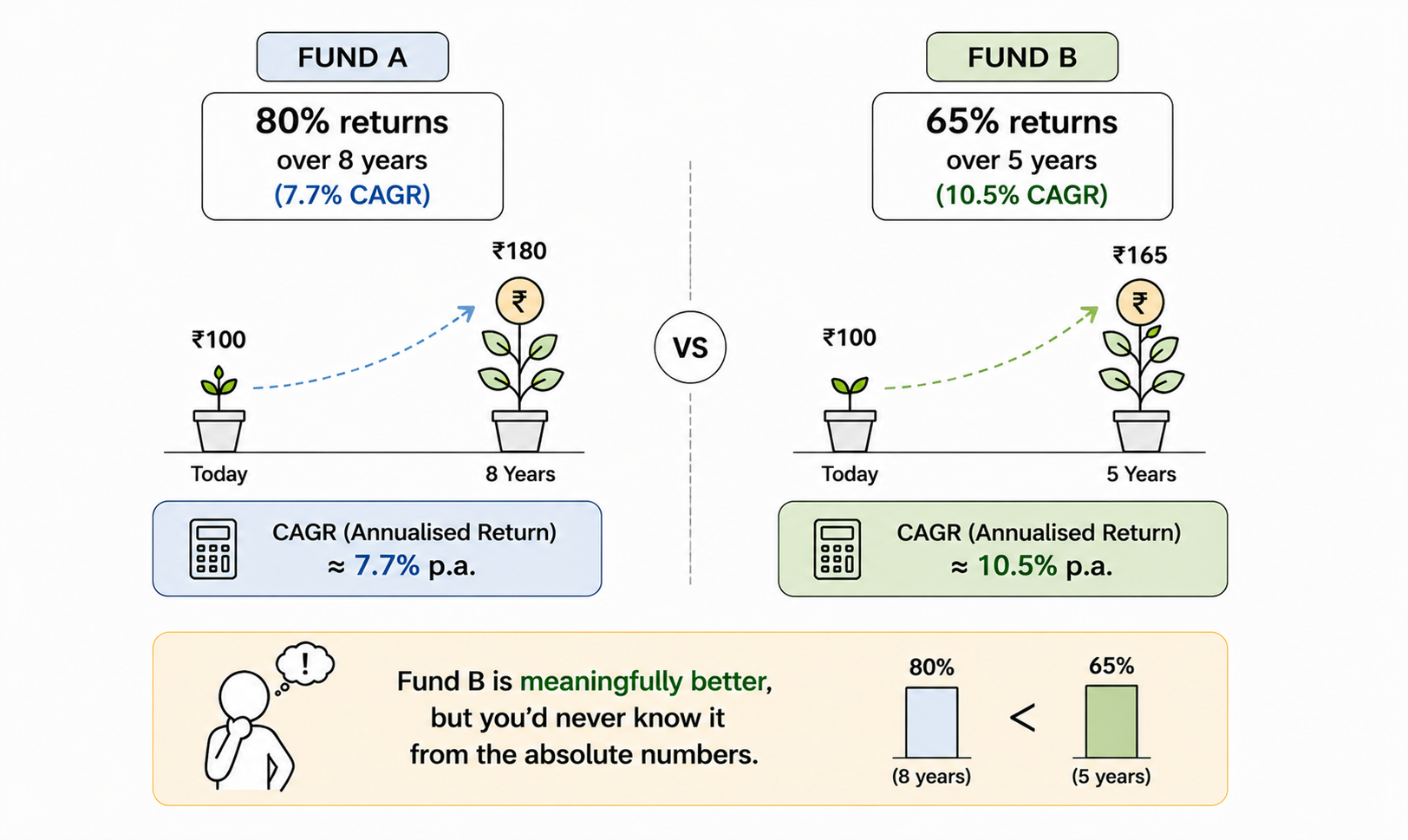

Why CAGR matters when comparing funds?

Fund A shows 80% returns over 8 years. Fund B shows 65% over 5 years. Which is better? You cannot compare these with absolute return. CAGR tells you Fund A earned 7.7% per year and Fund B earned 10.5% per year. Fund B is the stronger performer by a wide margin.

Both numbers are real. Only one tells you which fund actually grew faster. For any lumpsum investment held more than a year, CAGR is the right measure.

3. XIRR (Extended Internal Rate of Return)

This is where it gets interesting for you, because you don't invest in lumpsums. You put it as SIPs. Every month, ₹10,000 (or whatever your amount is) leaves your account and buys mutual fund units at that month's NAV. Each of those monthly investments have been compounding for a different length of time.

CAGR can't handle that. It assumes one entry point and one exit point. XIRR can. It calculates the annualised return across a series of irregular cash flows, which is exactly what a SIP is.

This is the number on your CAS statement (the consolidated statement CAMS or KFintech sends you, as mandated by SEBI). It's also the most honest measure of how your SIP is actually performing. A fund showing 14% CAGR over 5 years might show a 12% XIRR for your specific SIP because of when you invested and at what NAVs.

The rule: if you invested once, check CAGR. If you invest every month, check XIRR. The absolute return number on your app dashboard is almost never the one you should rely on for long-term decisions.

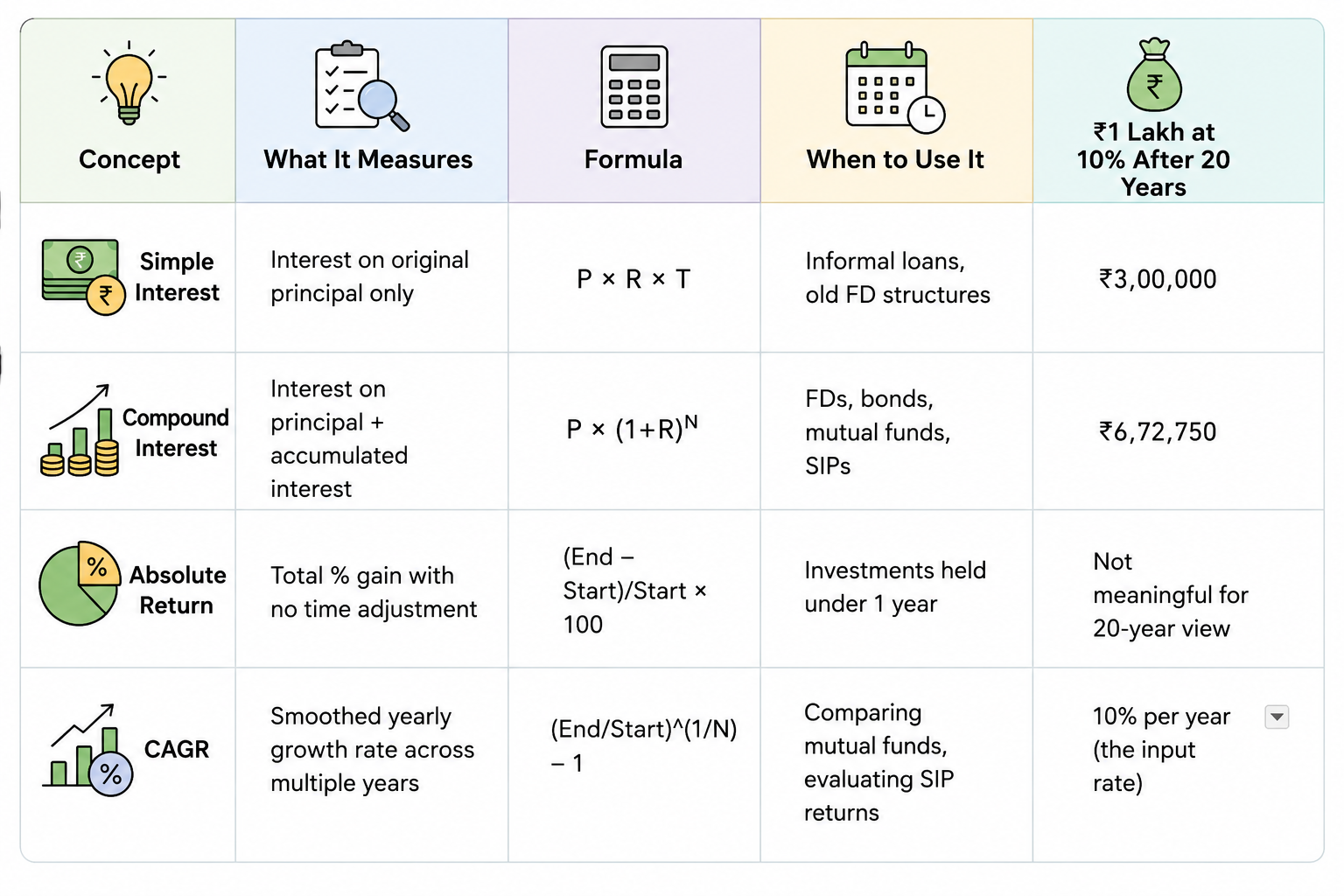

The Full Picture: Simple Interest vs Compound Interest vs Absolute Return vs CAGR

Here is every return concept you'll encounter as an investor in India and exactly what each one means for your money.

The 20-year column makes the stakes clear. Simple interest turns ₹1 lakh into ₹3 lakh. Compound interest turns it into ₹6.72 lakh. The ₹3.72 lakh difference came entirely from interest earning interest. You invested the same amount, waited the same time — the math did the rest.

Time is the only input you can't buy back

Now we come to the most expensive lesson in personal finance.

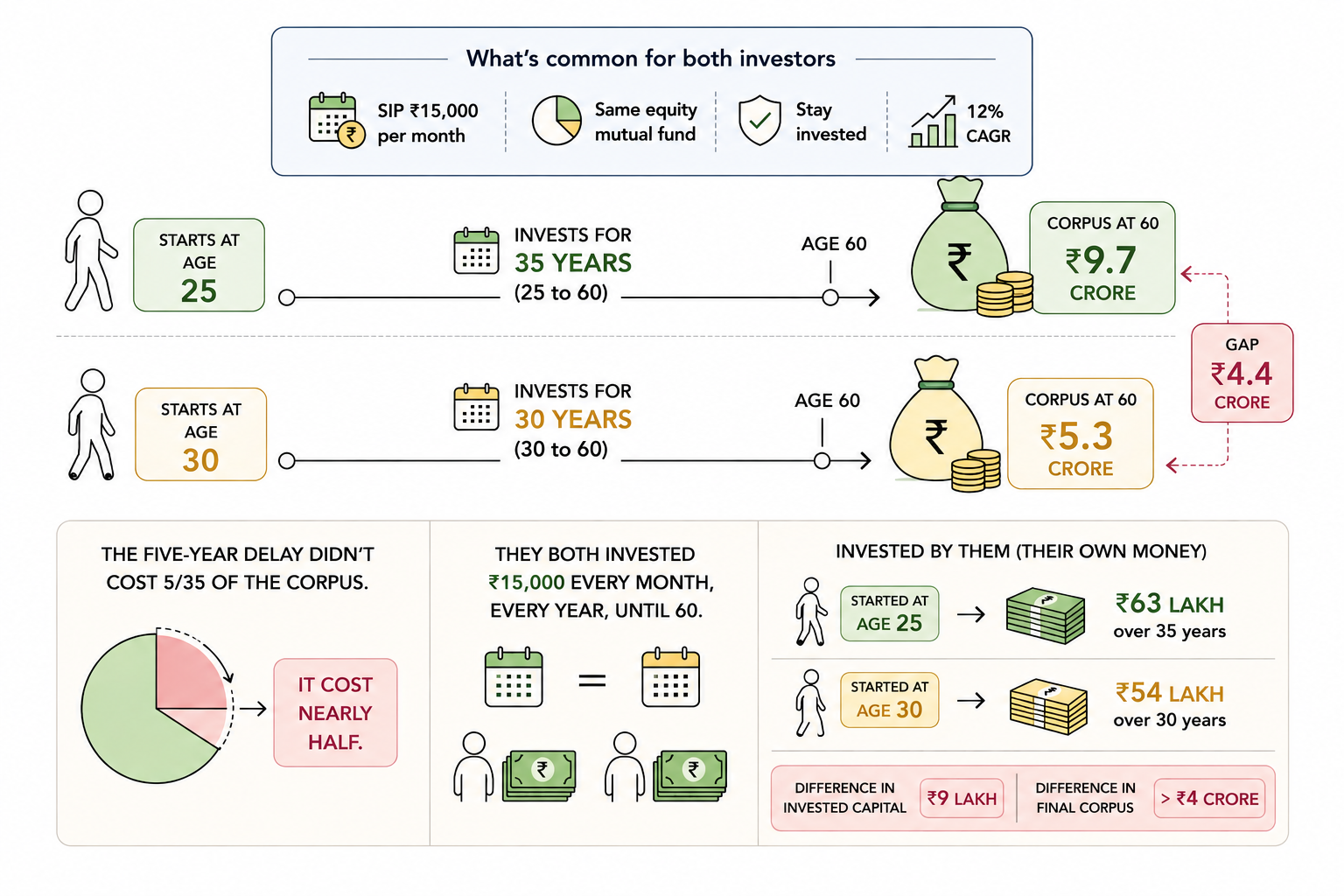

Look at the example illustrated below:

Same SIP. Same return. A five-year delay. The corpus difference is over ₹4 crore. This is what happens when you give compounding more time. The final years are where the absolute rupee gains explode, because the base is so much larger. Year 30 of an SIP adds more rupees than years 1 through 10 combined.

Money you don't invest at 25 isn't money you can simply invest harder later. The corpus that early SIP builds in the final decade cannot be replicated by a larger SIP started later, because there isn't enough time left for the math to do its work.

The single most powerful thing you can do for your future portfolio is start, even small, today. ₹2,000 a month from age 25 will outperform ₹5,000 a month from age 35 over a 35-year horizon. Time, not amount, is the lever.

What does this means for you?

A few takeaways, in the form you can act on this week:

- Stop reading absolute returns on multi-year investments. If your fund app shows you a 5-year absolute number, mentally convert it to CAGR. Roughly: divide by years, then add a small bump for compounding.

- Use CAGR when comparing funds. Two funds with different time periods cannot be compared on absolute return. CAGR puts them on the same scale.

- Find your XIRR. It's the most honest measure of how your specific SIP is actually performing. CAMS and KFintech both display it on the CAS statement, and most fund apps show it under portfolio summary.

- Don't wait until you "have enough" to start. The smallest SIP started today beats the largest SIP started in five years, on a long-enough horizon. ₹2,000 a month from age 25 outperforms ₹5,000 a month from age 35 over a 35-year window. Start now, scale later.

Armor's Scenario Sandbox takes your current portfolio and projects your wealth at 10, 20, and 30 years. It shows the compounding curve specific to your numbers, not a generic example. It also models decisions: what does your trajectory look like if you increase your SIP by ₹5,000/month? What if you extend your holding period by 5 years? On a ₹15 lakh portfolio, either change can shift your final corpus by ₹40–80 lakh. You can see that number before you decide.

Sources

- AMFI Monthly Note, March 2026 — amfiindia.com

- SEBI Investor Education — sebi.gov.in/investors

Frequently Asked Questions (FAQs)

What is the difference between simple and compound interest?

Simple interest is paid only on the original principal. Compound interest is paid on the principal plus all interest already earned. On ₹1 lakh at 10% over 20 years, simple interest gives you a final corpus of ₹3 lakh. Compound interest gives you ₹6.72 lakh.

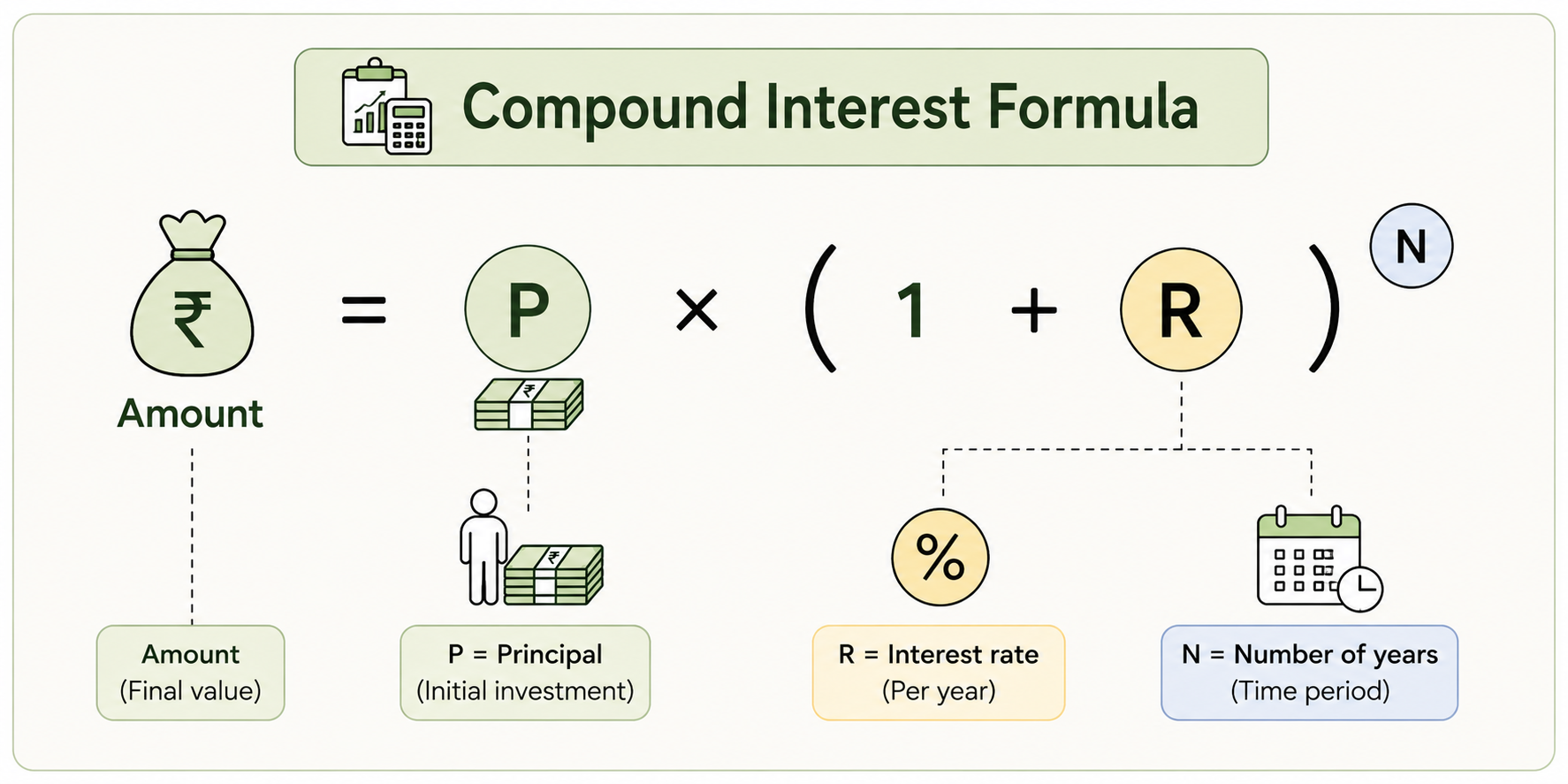

What is the formula for compound interest?

Final Amount = Principal × (1 + Rate)^Number of Years. So ₹1,00,000 invested at 10% for 5 years becomes ₹1,00,000 × (1.10)^5 = ₹1,61,051.

What is absolute return in mutual funds?

Absolute return is the total percentage gain on an investment from start to end, with no adjustment for how long it took. It's the right measure only for investments held for less than one year. For longer-term investments, it overstates performance because it hides time.

What is CAGR and why does it matter?

CAGR (Compounded Annual Growth Rate) is the single annual rate at which your investment grew, smoothed across all the ups and downs. It is the standard measure for any investment held longer than one year in India. A fund showing 80% over 8 years and another showing 65% over 5 years look incomparable on absolute return. On CAGR, they're 7.7% and 10.5% and the second fund is clearly the stronger performer.

What is XIRR and how is it different from CAGR?

CAGR assumes a single lump sum invested at the start and a single exit at the end. XIRR (Extended Internal Rate of Return) handles a series of irregular cash flows, like the monthly investments in a SIP. Each SIP installment compounds for a different length of time, which CAGR cannot capture. For SIPs, XIRR is the right measure.

Where can I see my XIRR?

On the Consolidated Account Statement (CAS) that CAMS or KFintech sends to your registered email every month, as mandated by SEBI. You can also check it out in the Armor app.

Why does starting an SIP early matter so much?

Compounding rewards the years furthest in the future, where the base is largest. The final decade of a 35-year SIP adds more rupees than the first 10 years combined. A five-year delay on a ₹15,000 monthly SIP at 12% reduces the final corpus from roughly ₹9.7 crore to ₹5.3 crore, nearly half, despite investing only ₹9 lakh less of your own money.

Is it better to start with a small SIP now or wait until I can afford a bigger one?

Start small now. ₹2,000 a month from age 25 outperforms ₹5,000 a month from age 35 over a 35-year horizon. The first decade of compounding builds the base everything else multiplies on. You can always scale a SIP up later. You cannot get the years back.