Why Are High-Earning Indians Losing Wealth Despite Good Salaries?

Industry Insights · 09 Apr 2026 · Team Armor

You're in the top 2% of Indian earners. You invest. You're disciplined. So why does real wealth still feel out of reach? The answer usually isn't your portfolio, it's five structural leaks that's quietly draining it.

While most high-earning Indians (salaried professionals earning around 40 LPA or above) believe wealth is about math, logic, and 'beating the market,' we often find them consistently making the same financial mistakes. They focus on finding better investments before fixing the leaks in their current setup.

Fewer than 2% of Indians earn 40 LPA or above, yet even within this group, sustained wealth-building remains the exception. Why? Because they are influenced by market hype, or caught in the trap of comparing themselves to their peers. What they end up doing is building a scoreboard and not a portfolio.

This post breaks down the 5 silent wealth leaks that drain even financially disciplined individuals, and why fixing them is worth more than any market return you'll chase this year.

What Are the 5 Silent Wealth Leaks?

Before you ask for a 2% higher return, you have to identify where your financial discipline is slipping. Most high-earning Indians don't lose money to the stock market, they lose it through structural gaps in their financial setup.

1. Lifestyle Inflation: When Income Grows Faster Than Savings

Lifestyle inflation happens when your spending rises in proportion with your income. This is why despite earning significantly more individuals may feel financially upgraded, but their net worth is standing still.

India's rising income levels are directly driving this pattern. Estimates suggest that India's per capita income could approach US$5,000 by 2030 (World Bank, India Economic Monitor 2023), accompanied by a measurable shift toward higher-quality, lifestyle-oriented spending. But here's the problem: if your income grows by 20% and your savings rate stays at 15%, you aren't building more wealth, you're financing a more expensive life.

The fix is simple in principle, every time your income increases, increase your savings rate first before upgrading your lifestyle. Even moving from 15% to 20% savings on a 40LPA salary adds ₹2L annually to your wealth-building engine.

2. Insurance as an Investment: The Coverage Gap Most Don't See

In India, insurance is still widely treated as a tax-saving tool rather than a long-term financial protection instrument. The result is a dangerous illusion of coverage.

The coverage gap is the difference between what you believe you're insured for and what you'd actually receive. For most Indians, including high earners, this gap is wider than 90%.

A 2023 study by SBI Life Insurance in partnership with Deloitte revealed a striking behavioural gap. While 97% of Indians believe their life cover should grow over time, only 6% are actually adequately insured while 68% of existing policyholders think they're sufficiently covered (SBI Life Deloitte Demystifying Indian Consumers Report 2023)

This is the insurance illusion, the feeling of being protected without the substance of it. For a salaried professional earning 40LPA, the recommended term insurance cover is typically 15–20x annual income, meaning ₹6–8 crore of pure term cover. Most high earners hold a fraction of this, often in traditional endowment or ULIP plans that offer poor coverage and mediocre returns simultaneously.

The fix isn't complicated, it's to ensure that there is a pure term plan in place with an appropriate health cover. What you lose in 'investment' you gain back tenfold in actual protection.

3. Lazy Money: What a Savings Account Is Really Costing You

Lazy money is any capital sitting in a low-yield account without a specific job, typically a savings account earning 3% while inflation runs at 5–6%. It makes you feel disciplined and gives you a sense of security.

More than 50% of Indian households prefer to keep their surplus in savings accounts (RBI Household Finance Survey) But here's what most people don't account for, your purchasing power falls whenever your interest rate doesn't keep pace with inflation.

Here's the math:

You save ₹1,00,000 in your savings account at 3% APY. After 1 year it becomes ₹1,03,000, you gain ₹3,000 in interest.

Keeping inflation at 6%, prices rose by ₹6,000 over the same period.

Net effect - You are ₹3,000 short in purchasing power.

In real terms, your ₹1 lakh is now worth ₹97,000 in today's money. Over 10 years, this compounding erosion quietly destroys wealth.

The alternative isn't complicated. A liquid fund in India typically yields 6.5 - 7.5% annually roughly matching or beating inflation but remains accessible within 1–2 business days.

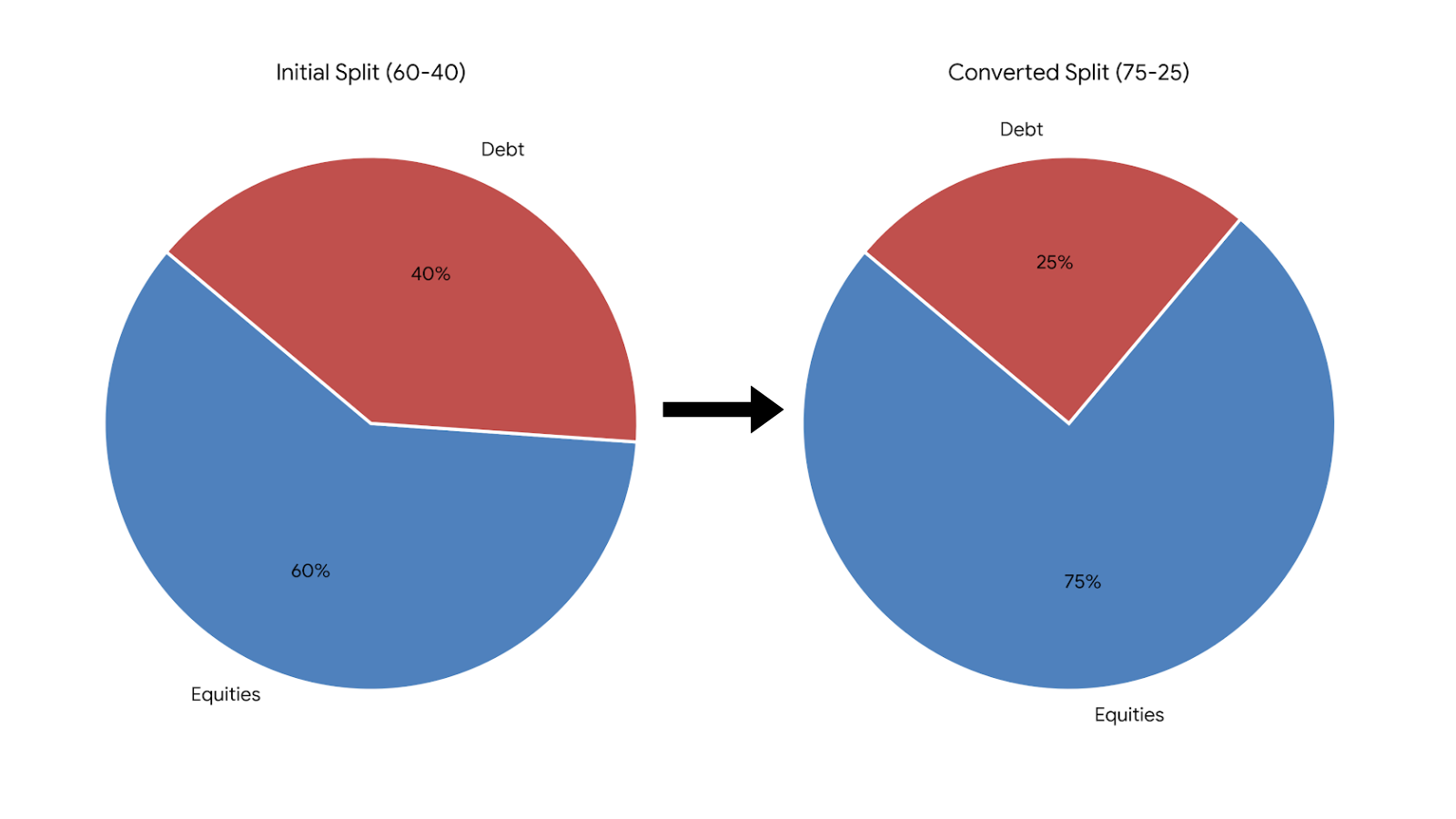

4. Asset Allocation Drift: How Rising Markets Silently Increase Your Risk

Asset allocation drift is what happens when strong market performance quietly shifts your portfolio beyond your intended risk level without you making a single decision to take on more risk.

Getting the right mix of stocks, bonds, and cash in your portfolio is fundamental to long-term wealth creation. An equally important yet far less discussed is maintaining that mix as markets move.

Here's how drift works in practice:

You start with a clear plan: 60% Equity / 40% Debt.

Equities rally strongly over 2–3 years.

Your 60% equity position silently becomes: 65% → 70% → 75%

The plan didn't change. But your portfolio risk did.

When markets correct, and they always do, a 75% equity portfolio falls significantly harder than your original 60% allocation. This increases your recovery time (compounding pauses during drawdown), and raises the probability you'll panic and exit at exactly the wrong moment. You don't lose wealth because equities are bad. You lose wealth because your risk crept up without intention.

The fix is systematic rebalancing. It is important to reset your portfolio to its target allocation once or twice a year, regardless of what markets are doing. Financial discipline over reaction.

5. The Thin Safety Net: Why 6 Months of Liquid Cash Is Non-Negotiable

An emergency fund is a dedicated liquid buffer, separate from investments, that covers 6 months of essential expenses. Without it, any financial shock forces you to disrupt your long-term wealth-building at the worst possible time.

We live in an unpredictable world where layoffs, medical emergencies, or sudden family expenses can arrive without warning. Imagine earning ₹30L a year and investing aggressively but maintaining no liquid buffer. A ₹4–8L emergency doesn't pause your fixed expenses but without an emergency fund, you're forced to redeem long-term investments at potentially unfavourable times, or take on high-interest debt. Both disrupt compounding and derail long-term wealth creation.

For a salaried professional earning 30–50LPA, 6 months of liquid cover typically means ₹10-12L in an easily accessible instrument like a liquid fund or an overnight fund specifically for emergencies. This is not idle money. It's the structural foundation that makes every other part of your financial plan resilient.

How Armor Helps You Build a Leak-Proof Financial System

Once you have your numbers, emotions, and ambitions in place, what you don't need is more 'tips', you need a system to calibrate everything in real time. Armor is that system. It handles logic so you can handle life.

We help you:

• Strip away the 'junk' products that don't serve your goals.

• Build a buffer that actually lets you sleep at night.

• Automate your risk management so you don't have to watch the news.

• Tag every rupee to a specific goal, so your money finally has a job.

Ready to build yours?

Armor maps your entire financial structure which includes your income, savings, insurance, and investments and shows you exactly where the leaks are. Run your free financial health check in under 5 minutes.

" You do not rise to the level of your goals. You fall to the level of your systems" - James Clear, Atomic Habits

Frequently Asked Questions

1. What are the most common wealth leaks for high-earning Indians?

The most common wealth leaks for high-earning Indians are lifestyle inflation, insurance as an investment, lazy money in low-yield savings accounts, asset allocation drift, and an inadequate emergency fund. These aren't market risks but they're structural gaps in financial setup that quietly drain wealth, regardless of how well your investments perform. For salaried professionals earning 30–50LPA, fixing these five leaks typically delivers more financial impact than chasing higher investment returns.

2. How does lifestyle inflation affect wealth building for salaried professionals in India?

Lifestyle inflation happens when spending rises proportionally with income, leaving the savings rate unchanged despite earning more. A salaried professional whose income grows by 20% but whose savings rate stays at 15% isn't building more wealth but they're financing a more expensive version of the same life. The fix is straightforward, every time income increases, raise your savings rate first. Even moving from 15% to 20% savings on a 40LPA salary adds approximately ₹2L annually to long-term wealth creation.

3. Why is keeping money in a savings account bad for high earners in India?

A savings account in India typically yields around 3% APY while inflation runs at 5–6%, meaning your purchasing power falls every year the money sits there. On ₹1,00,000 saved at 3%, you gain ₹3,000 in interest but prices rise by ₹6,000. In real terms, your ₹1 lakh is worth ₹97,000 in today's money by year end. Over 10 years, this compounding erosion quietly destroys wealth. A liquid fund, which yields 6.5–7.5% annually and remains accessible within 1–2 business days, is a significantly better home for money that isn't actively invested.

4. What is asset allocation drift and how does it increase investment risk?

Asset allocation drift is when strong market performance shifts your portfolio beyond its intended risk level without any deliberate decision on your part. If you start with 60% equity and 40% debt, a sustained equity rally can push that to 70% or 75% equity over time. When markets correct, a 75% equity portfolio falls significantly harder than the original 60% allocation, increasing recovery time and the probability of panic-selling at the wrong moment. The fix is systematic rebalancing: resetting your portfolio to its target allocation once or twice a year, regardless of market conditions.

5. How much emergency fund should someone earning 40LPA maintain in India?

For a salaried professional earning 40LPA, a well-structured emergency fund should cover 6 months of essential expenses, typically between ₹8–12L depending on lifestyle and fixed commitments. This buffer should be kept in a dedicated, easily accessible instrument such as a liquid fund or an overnight fund separate from long-term investments. Without this foundation, any financial shock forces you to redeem investments at potentially unfavourable times or take on high-interest debt, both of which disrupt compounding and derail long-term wealth creation.