Portfolio Diversification in India: The 4-Pillar Strategy That Protects Your Wealth

Investing · 09 Apr 2026 · Team Armor

When markets are running hot, diversification feels like a handicap. But in every market cycle, something falls sharply and the investors who survive aren't the ones who picked the right asset. They're the ones who never had everything in the wrong one. Here's the four-pillar framework that keeps an Indian portfolio standing through every cycle.

Your neighbour is talking about how his portfolio is up 40% when the markets are in a bull run and somehow in this context portfolio diversification feels like a deliberate handicap, like you're choosing to be slower on purpose.

But here's what your neighbour isn't telling you: in every market cycle, something falls sharply. It could be stocks, real estate, the rupee or sometimes all three at once. The investors who survive aren't the ones who picked the right asset. They're the ones who never had everything in the wrong one.

Diversification isn't a compromise. It's insurance for your lifestyle.

Why Diversification Matters Differently in India

We live through cycles of dominance. There are years when Indian equities are the standout performers. Years when gold is the only thing standing between you and a weakening rupee or a boring fixed deposit is the only thing that lets you sleep. But then there are years like 2008 and 2020 when nearly every growth asset falls simultaneously, and the investors with no buffers are forced to sell at exactly the wrong moment. The goal of portfolio diversification in India isn't to have everything rise at the same time. It's to hold assets that don't fall at the same time.

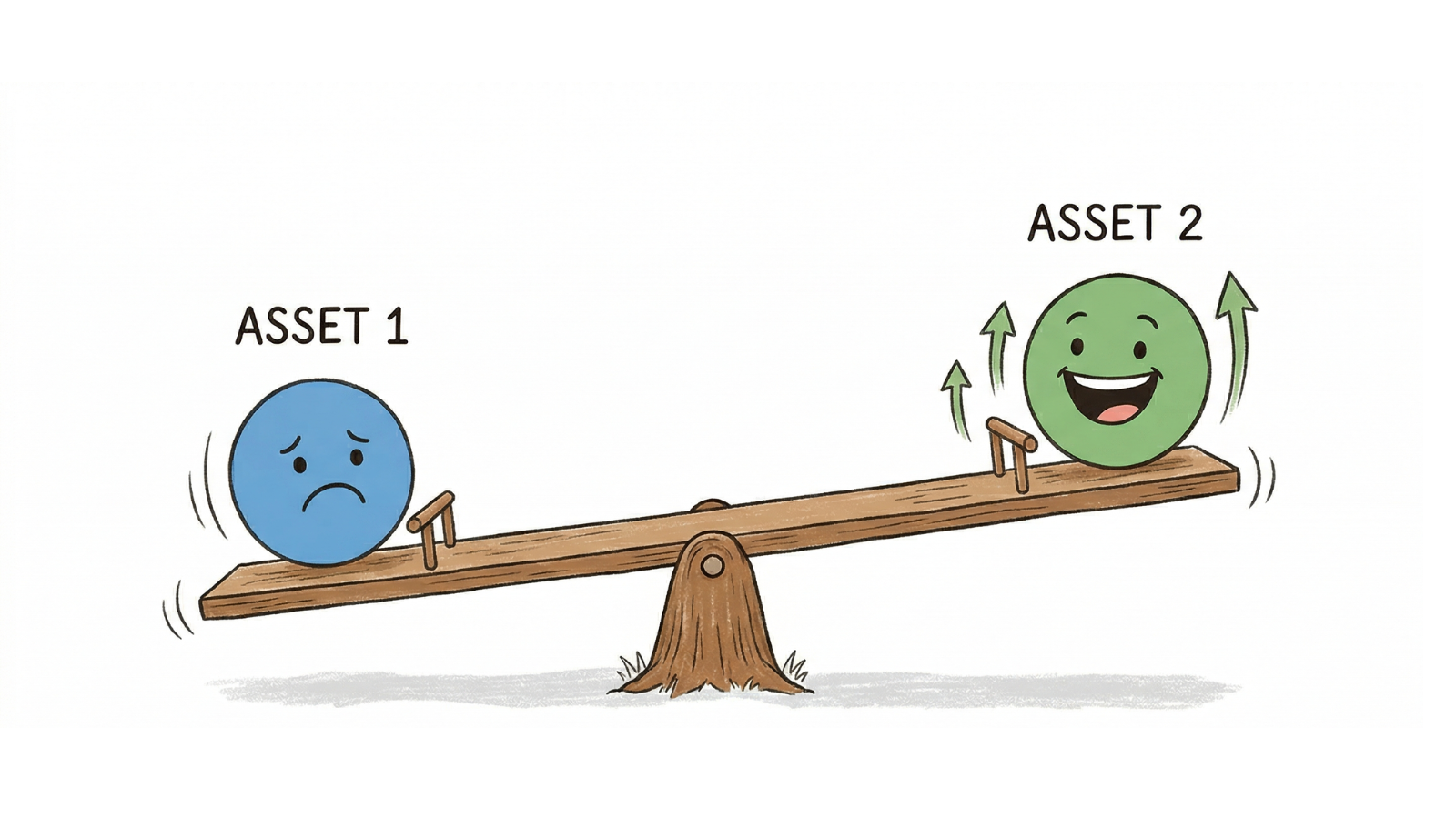

The Negative Correlation Rule: How the Seesaw Works

So what makes diversification work? It's a negative correlation. In practice, it means this: when one asset falls, another tends to hold or rise. Not perfectly. Not always. But enough to matter.

Here's how the major Indian asset classes have historically behaved against each other:

When equities fall: Fear drives investors toward safe havens. Gold typically rises. In 2008, the Sensex fell 60% while gold rose to 20% that same year. In 2020, the Nifty dropped 38% in weeks while gold gained 14%.

When inflation rises: Cash and fixed income lose real value. Real estate and commodities tend to hold their ground, as the underlying assets are repriced upward.

When the rupee weakens: International equities provide a natural hedge. If you hold global funds denominated in dollars or euros, a weaker rupee means your returns translate back to more rupees & not fewer.

The seesaw isn't perfectly balanced at all times. But when one side hits the ground, the other is in the air. That's the whole point.

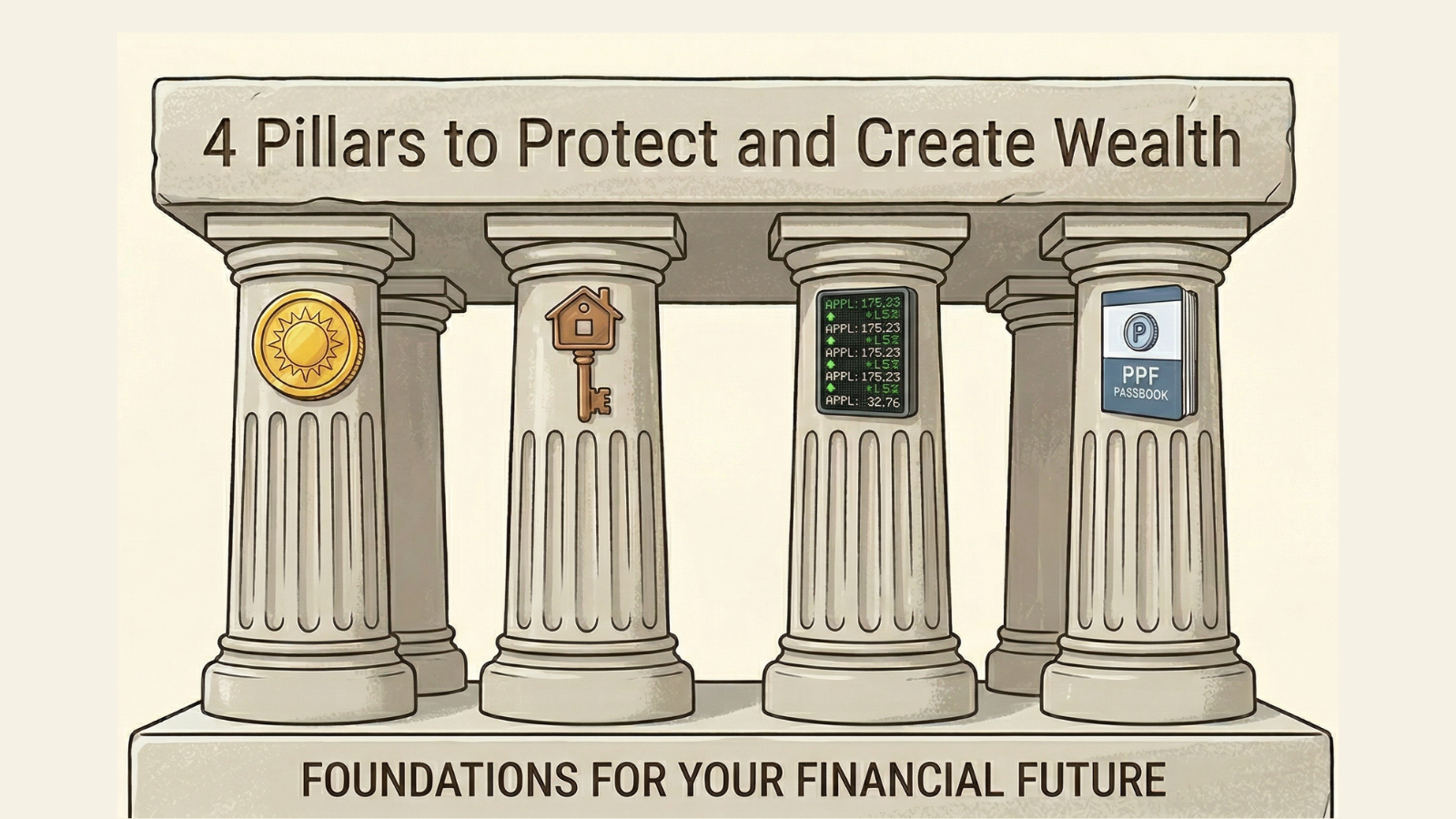

The 4 Pillars: What Every Indian Portfolio Needs

If you think of your portfolio as a set of assets which have distinct jobs then true diversification is when all four jobs are filled.

Pillar 1: Growth (Equities and Mutual Funds)

This is the wealth engine of your portfolio. Over long periods, Indian equities have compounded at 12–14% annually, well ahead of inflation. But equity returns are volatile year-to-year. Without the other pillars, that volatility becomes a behavioural risk: markets fall, you panic-sell, and you lock in losses.

A diversified equity allocation forms the core of wealth creation. It works best when held for 7+ years, with contributions automated through SIP.

Pillar 2: Safety (PPF, EPF, VPF)

These government-backed instruments offer something equities can't: certainty. PPF and EPF returns are fixed, tax-efficient, and completely uncorrelated to market movements. When everything else is falling, this pillar holds.

The safety pillar also serves a psychological function. As Monika Halan notes in Let's Talk Money, having stable buckets in your portfolio protects you from your own worst instincts during downturns.

Pillar 3: Insurance (Gold and Sovereign Gold Bonds)

Gold is a particularly important asset for Indian investors. It serves as a direct hedge against rupee depreciation and global uncertainty.

Sovereign Gold Bonds (SGBs) are the most efficient way to hold gold in India where you get 2.5% interest annually, capital gains on redemption are tax-exempt after 8 years, and there's no storage or making charge. A 10–15% allocation to gold is a reasonable range for most Indian portfolios.

Pillar 4: Structure (Real Estate and REITs)

Real estate is India's most culturally trusted asset class. It provides rental yield, capital appreciation, and a psychological sense of permanence. For most families, the primary home serves this function though it should not be counted as an investable asset since you live in it.

For investors who want real estate exposure without the illiquidity, Real Estate Investment Trusts (REITs) now offer an accessible alternative. REITs are listed on exchanges, pay regular dividends, and can be entered and exited in days rather than months.

The Time Factor: Asset Rich, Cash Poor

Diversification isn't just about asset type. It's also about time horizon and liquidity.

Imagine your entire net worth is tied up in a beautiful 3BHK in Bengaluru. If a medical emergency hits tomorrow, that apartment is completely useless in the short term. You can't sell a kitchen to pay a hospital bill. Real estate takes months to liquidate if it sells at all during a distressed period.

True portfolio diversification in India means holding liquid assets (mutual funds, stocks) that you can access within 48 hours, alongside your long-term illiquid wealth. A simple rule: any money you might need within 24 months should never be in an illiquid asset. Period.

Your emergency fund (6 months of expenses) should sit in a liquid fund or high-interest savings account, not invested in equity, not locked in a fixed deposit with a penalty, and definitely not in real estate.

You don't need all four pillars perfectly in place before you begin. Most people already have one or two without realising it, like their EPF through their employer, a family home, or a couple of SIPs. The question is whether what you have is working as a system or just sitting in silos.

Start by naming which pillar is missing. If you have growth but no safety buffer, that's the gap. If you have real estate but no liquidity, that's the gap. One pillar at a time is how a portfolio actually gets built.

Frequently Asked Questions

1.What is the best way to diversify investments in India?

The most effective approach for most Indian salaried investors is the four-pillar model: equities (mutual funds and SIPs) for growth, PPF/EPF for safety, gold or Sovereign Gold Bonds as a crisis hedge, and real estate or REITs for structure. Each pillar serves a distinct function, and missing any one of them creates a specific vulnerability in your portfolio.

2. How much gold should an Indian investor hold in their portfolio?

A 10–15% allocation to gold is a widely used starting point for Indian portfolios. Sovereign Gold Bonds are the most efficient vehicle as they pay 2.5% annual interest, offer tax-exempt capital gains after 8 years, and carry no storage or making charges. Physical gold is less efficient as an investment but remains culturally significant for many families.

3. Is real estate a good investment for Indian families?

Real estate can be a valuable structural asset, but it comes with significant illiquidity risk. A ₹1 crore apartment cannot be partially sold in an emergency. For investors who want real estate exposure with better liquidity, REITs listed on Indian exchanges offer rental income and capital appreciation without the lock-in of physical property.

4. How much of my portfolio should stay liquid, and where should I keep it?

Any money you might need within the next 24 months should never be in an illiquid asset. Your emergency fund, which should cover 6 months of expenses, belongs in a liquid mutual fund or high-interest savings account. Liquidity isn't a return strategy, it's what ensures you never have to sell the wrong asset at the wrong time.

5. What happened to undiversified investors during India's market crashes?

In 2008, the Sensex fell 60%. Investors with only equities saw devastating declines, those with gold saw it rise 20% that same year. In 2020, the Nifty dropped 38% in weeks while gold gained 14%. In both cases, the investors who held their position through the crash were the ones with buffers. The ones without buffers were forced to sell at the bottom.

6. How often should I rebalance my diversified portfolio in India?

Once a year is sufficient for most investors. If one asset class has significantly outperformed and now represents a much larger share of your portfolio than intended, trim it and redirect to the underweighted pillars. Annual rebalancing isn't market timing, it's systematic risk management.