How Indian Families Build Wealth: 5 Habits That Actually Work

Savings · 09 Apr 2026 · Team Armor

Wealth creation for Indian families comes from a set of financial habits, built deliberately and repeated month after month. Here are the five that consistently separate families building wealth from those who aren't.

Wealth creation for Indian families almost never happens by accident. It doesn't come from a lucky stock tip, a once-in-a-decade real estate deal, or the right crypto call at the right moment. It comes from something far less exciting and far more reliable: a set of financial habits, built deliberately and repeated month after month.

Most middle-income households in India work hard, earn reasonably well, and show up every day. But very little structured thought goes into turning that monthly salary into long-term wealth. In a world of FOMO, hot tips, BNPL apps, and the constant pressure of visible consumption, control over where money goes and what it's actually building has quietly slipped away for many families.

Why We Earn Well but Build Little Wealth

It’s a one-sentence diagnosis, "we'll figure it out later" that quietly defines the financial lives of more Indian families than any other factor.

The challenge isn't a lack of income but it is a lack of a system. With easy EMIs, BNPL credit, and the constant pressure of visible consumption, control over where money goes has quietly slipped away from us. One unplanned hospitalisation can wipe out years of careful savings.

The families that build wealth aren't dealing in windfalls. They're dealing in systems.

What "Wealth" Really Means for Indian Families

Before building wealth, it helps to define what you're actually building toward. For one family, wealth means retiring at 52. For another, it means the financial cushion to take a two-year career break.

Money is deeply personal. The value of ₹100 means something different to someone who watched their parents skip meals for school fees than to someone who always had a safety net. That's exactly why one-size-fits-all financial advice rarely works.

Wealth creation for Indian families has to start with one honest question: what do I actually want my money to do?

The 5 Habits That Actually Build Wealth

These aren't complex strategies. They're the habits that consistently separate families building wealth from those who aren't.

1. Automate Savings Before You Spend

The most powerful shift isn't how much you save, it's when you save. Most families save whatever is left at the end of the month. Families building wealth save on the 2nd of every month, before anything else happens.

2. Protect Before You Grow

The single most expensive financial mistake in India isn't a bad investment. It's inadequate insurance. Insurance isn't a cost. It's the foundation that lets compounding happen undisturbed.

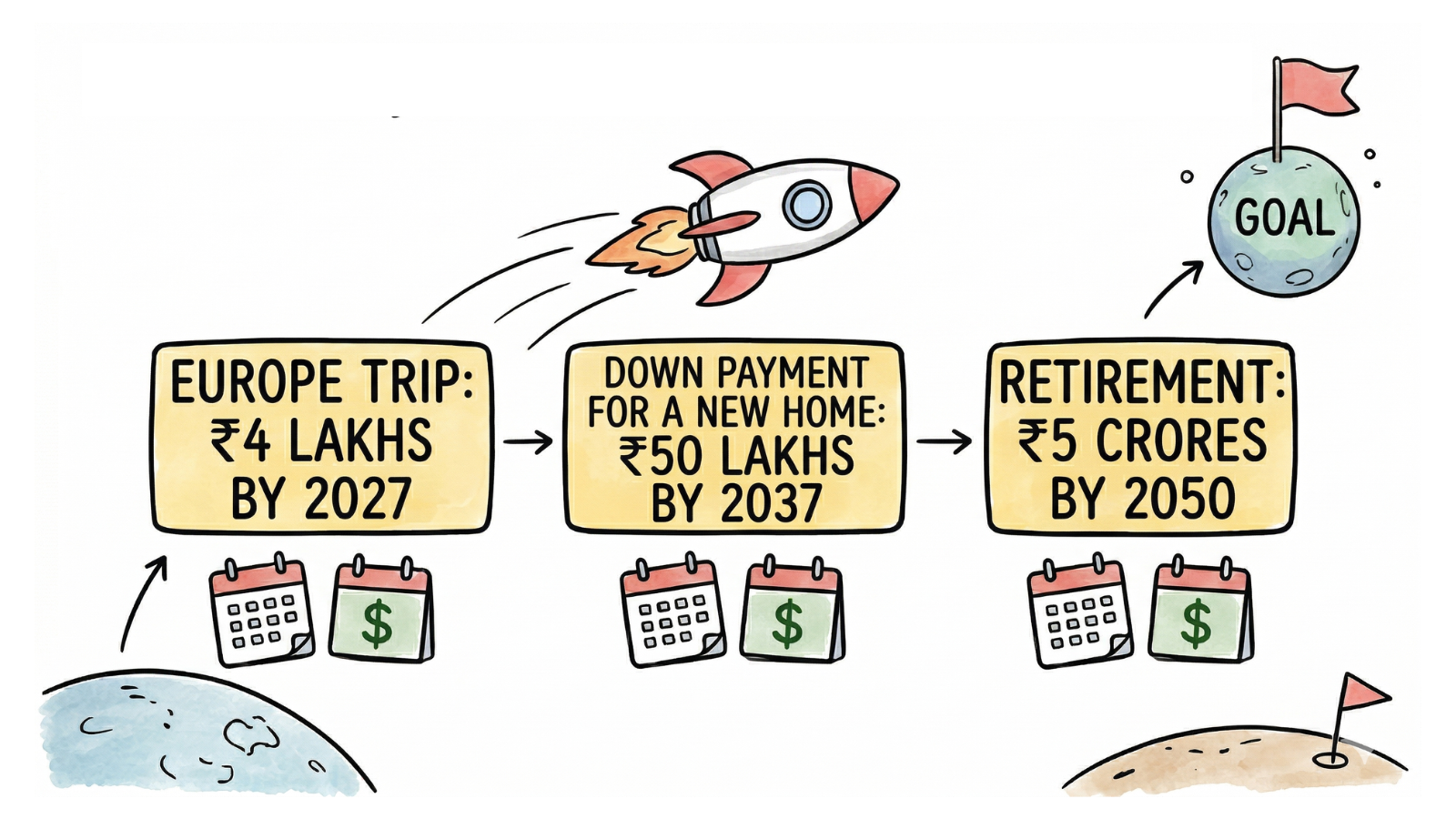

3. Name Every Goal With a ₹ Amount and a Timeline

"I want to save more" is not a plan. "₹20 lakh for a down payment by March 2028, invested in a debt mutual fund" is a plan. Every family has goals. Very few have put a rupee figure and a deadline on them. When you name your goals with specific numbers and timelines, every financial decision becomes simpler.

4. Watch Lifestyle Creep Every Year

A simple annual audit: open your bank statement from two years ago. Compare five categories - rent, food, subscriptions, shopping, and travel. Ask honestly: which of these upgrades actually made your life meaningfully better? The ones that didn't are candidates to redirect into wealth.

5. Review Once a Quarter Before a Crisis Forces You To

Families building wealth don't wait for a health scare or a job loss to look at their finances. They review proactively, once a quarter: check insurance coverage, track investment progress against goals, adjust for major life changes.

This habit alone can save lakhs. Course corrections when you're slightly off-track cost nothing. Course corrections in a crisis cost everything.

Where to Start If You Haven't Yet

If you've read this far, then you already know you need to do something about your finances & that recognition is half the work done. Most people stay stuck not because they lack information, but because awareness never turns into an actionable.

So here's one- pick the habit that feels most off-track for you right now. Not all five. Just one. Set up the SIP, name the goal with a rupee figure, or open the bank statement you've been avoiding. The system builds from there.

At Armor, we help Indian families turn that first step into a plan built around their specific numbers, goals, and life stage. If that's something you're ready for, we're here.

Frequently Asked Questions (FAQs)

1. Why do Indian families struggle to build wealth even when they earn well?

The issue isn't income, it's the absence of a system. Easy EMIs, BNPL credit, and the constant pressure of visible consumption have quietly taken control of where money goes. The "we'll figure it out later" mindset compounds this further: most families are reacting to money rather than directing it.

2. What is the single most effective savings habit for Indian families?

Automating savings before anything else is spent. Most families save whatever is left at month-end which is often very little. Switching your SIP or savings transfer to the 2nd of the month, the day after salary, removes the decision entirely. You can't spend what's already been moved.

3. Why should I sort out insurance before focusing on investments?

Because one unplanned hospitalisation can wipe out years of careful savings, even for a middle-class household. Insurance is the foundation that allows compounding to happen undisturbed. A bad investment costs you returns; inadequate insurance can cost you everything you've built.

4. How do I set financial goals that actually push me to act on them?

Attach a specific ₹ amount and a deadline to every goal. "I want to save more" isn't a plan. "₹20 lakh for a down payment by March 2028, invested in a debt mutual fund" is a plan. The moment a goal has a number and a timeline, every financial decision becomes easier to evaluate against it.

5. How do I know if lifestyle creep is quietly eating into my wealth?

Open your bank statement from two years ago and compare five categories against today: rent, food, subscriptions, shopping, and travel. The question to ask for each upgrade isn't whether you can afford it, it’s whether it actually made your life meaningfully better. The ones that didn't are money that could be redirected into wealth.

6. How often should I review my finances, and what should I check?

Once a quarter, proactively, check insurance coverage is still adequate, track whether investments are on pace for your named goals, and account for any major life changes since the last review. Course corrections when you're slightly off-track are free. In a crisis, they're not.