Financial Goal Setting in India: A 5-Step Plan to Turn Intentions Into Action

Financial Planning · 09 Apr 2026 · Team Armor

Most people can name their financial goals in seconds. Very few have put a rupee figure, a deadline, and a monthly savings target on any of them. That gap between having goals and having a plan is where decades of financial shortfall quietly builds up. This is the framework to close it.

A goal without a number is a wish. A number without a timeline is a hope. A timeline without a savings requirement is a plan you cannot yet execute.

If I were to ask you, What are your top three financial goals?, you'd probably say something like: buy a home, fund the kids' education, retire without depending on anyone.

Now here's the harder question: do you have an actionable plan with actual numbers, a timeline, and a monthly savings target for any of them? For most people, the answer is no. And that gap between having goals and having a plan, is where decades of financial shortfall quietly builds up.

This blog walks you through a 5-step financial goal-setting framework designed specifically for high-income Indian earners. We will follow Priya, a 32-year-old product manager earning ₹35 lakhs per year, through every step so you can see exactly how this plays out with real numbers.

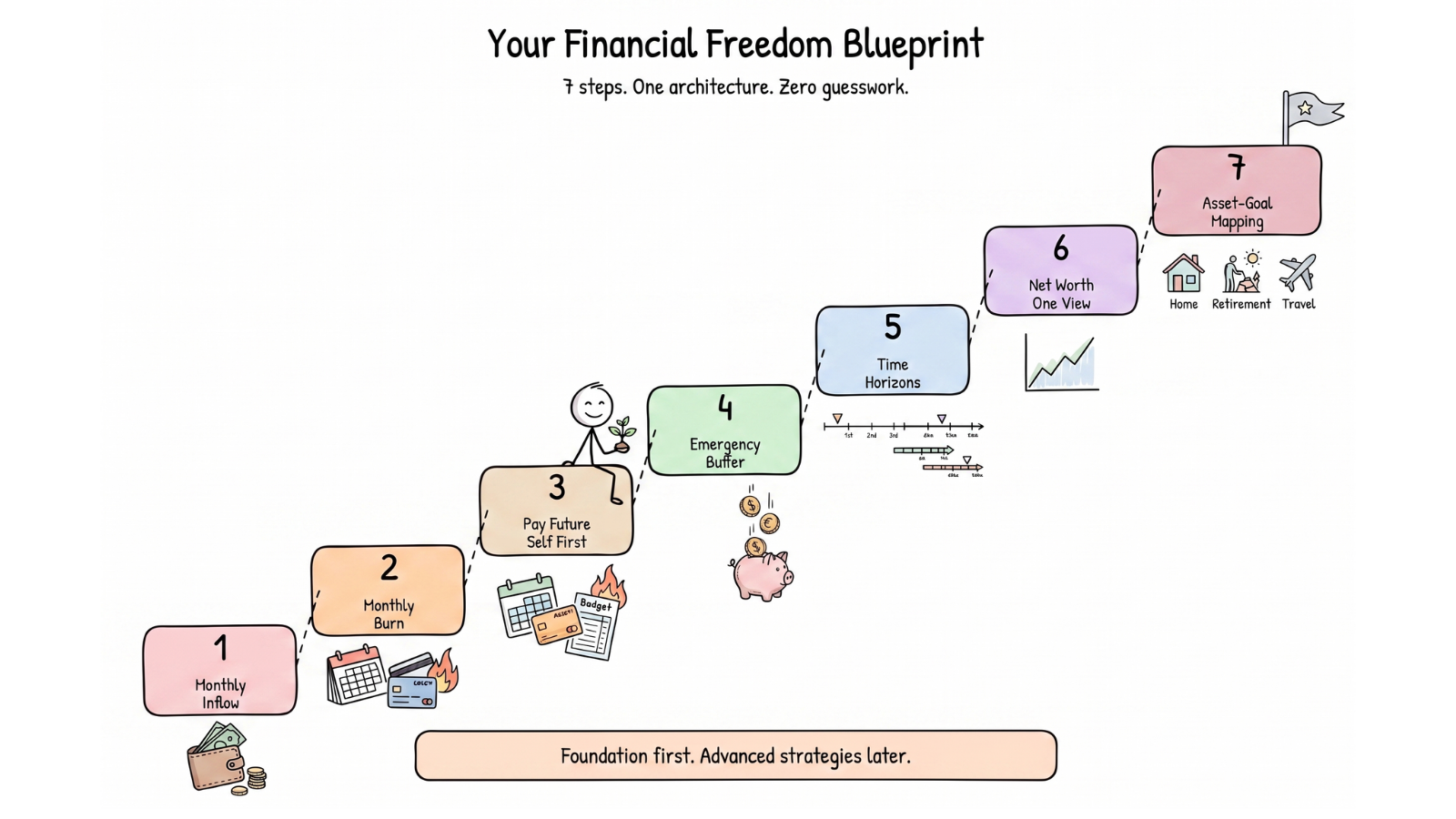

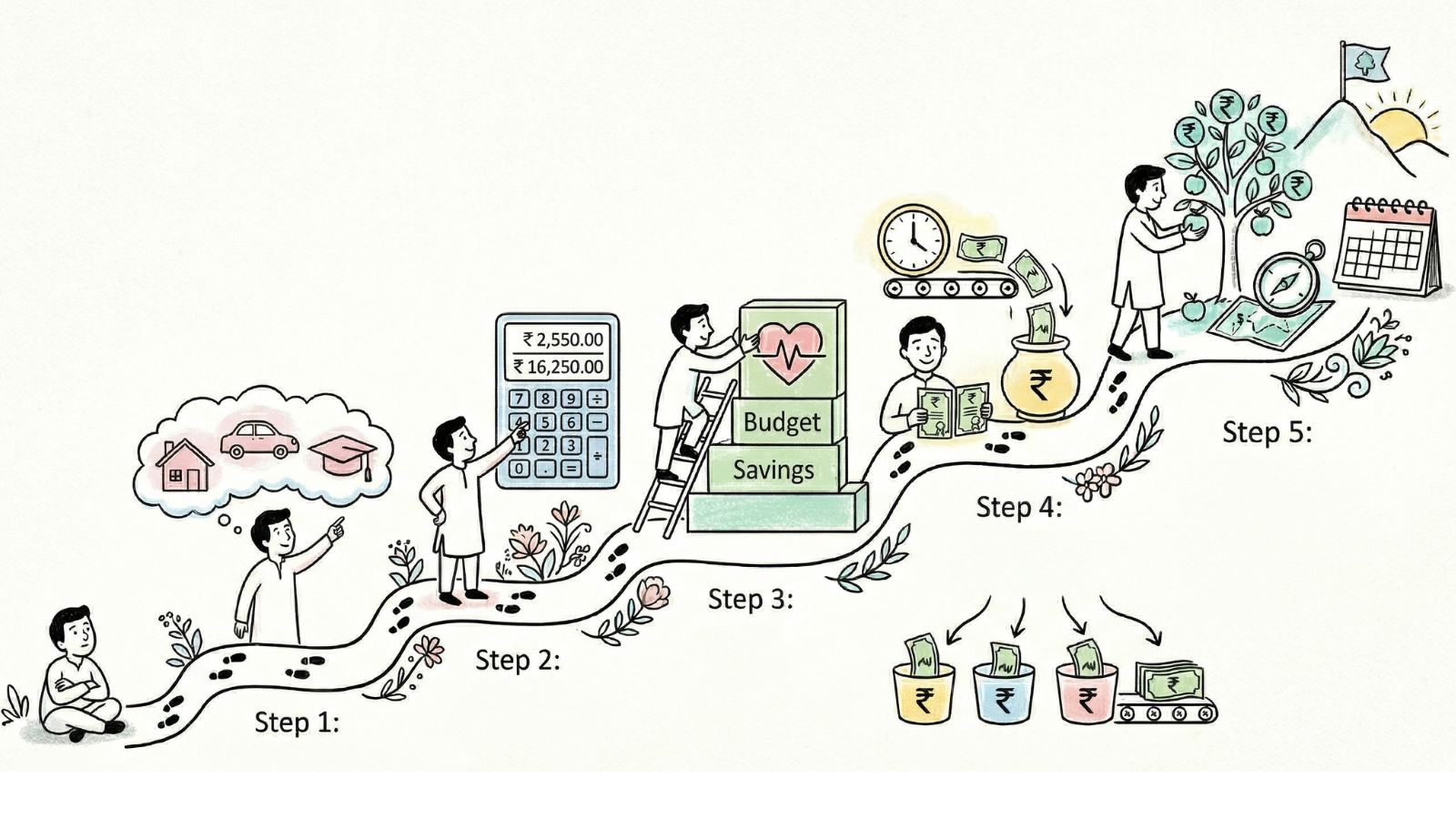

Step 1: Categorise Your Financial Goals

This sounds simple, and to be honest quite cliche but most people skip it. They treat all their goals the same way with maybe one or two savings accounts, a few SIPs, and hope it covers everything. Here’s what they don’t account for - a goal three years away cannot be invested the same way as one that's twenty years away.

Priya’s goals included a flat down payment, her child’s college fund, and retirement. When she saw them together for the first time, she realised her current SIP of ₹50,000/month couldn't fund even one of them fully.

Now don't read that as a problem. That is the whole point of this exercise. You can only prioritise once you see the full picture.

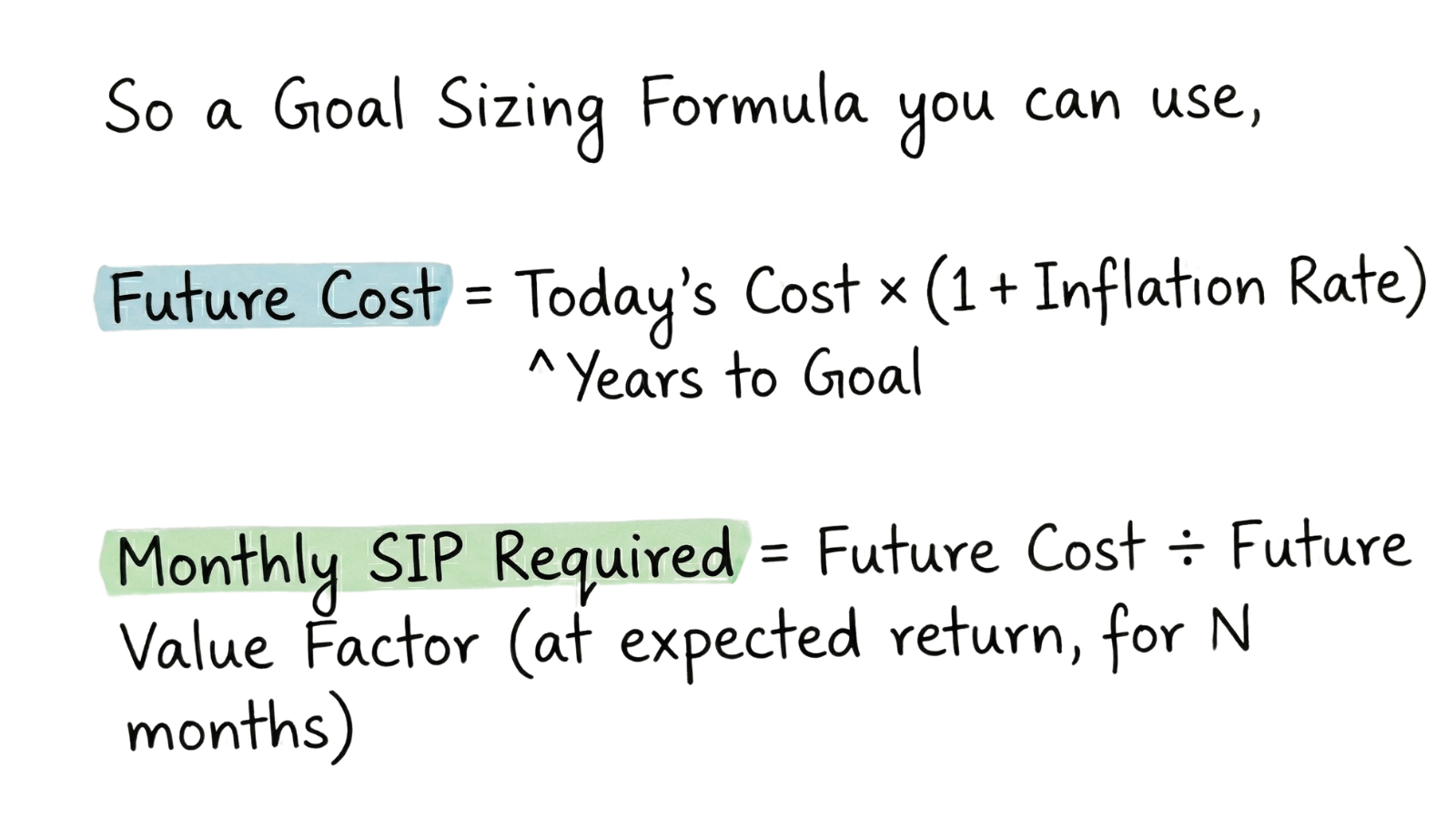

Step 2: Calculate the Actual Cost of Your Goals

Every goal needs a number. And no, a comfortable retirement is not a number. A monthly income of ₹2.5 lakh in today's terms, sustained for 30 years post-retirement is a number and the corpus it requires can be calculated precisely.

But the adjustment most people miss: inflation. Here are the rates to use for India:

- General expenses: 6% annual inflation (based on India's long-term CPI average)

- Education costs: 8–10% annual inflation (education costs in India have consistently outpaced general CPI)

- Healthcare costs: 10–14% annual inflation (one of the highest cost escalators in personal finance)

When Priya calculated her numbers:

Her flat down payment goal: ₹50L in today's value, which she would need in 7 years:

₹50L × (1.06)^7 = ₹75.2L

At 12% expected CAGR through a balanced mutual fund SIP, reaching ₹75.2L in 7 years requires approximately ₹57,500/month just for this one goal.

Her child’s college fund: ₹25L in today's value, 16 years away, at 10% education inflation:

₹25L × (1.10)^16 = ₹1.15 crore

The value of running this exercise early isn't motivational. It's mathematical. When done early enough, the adjustments required are manageable. When done late, the options become far harder.

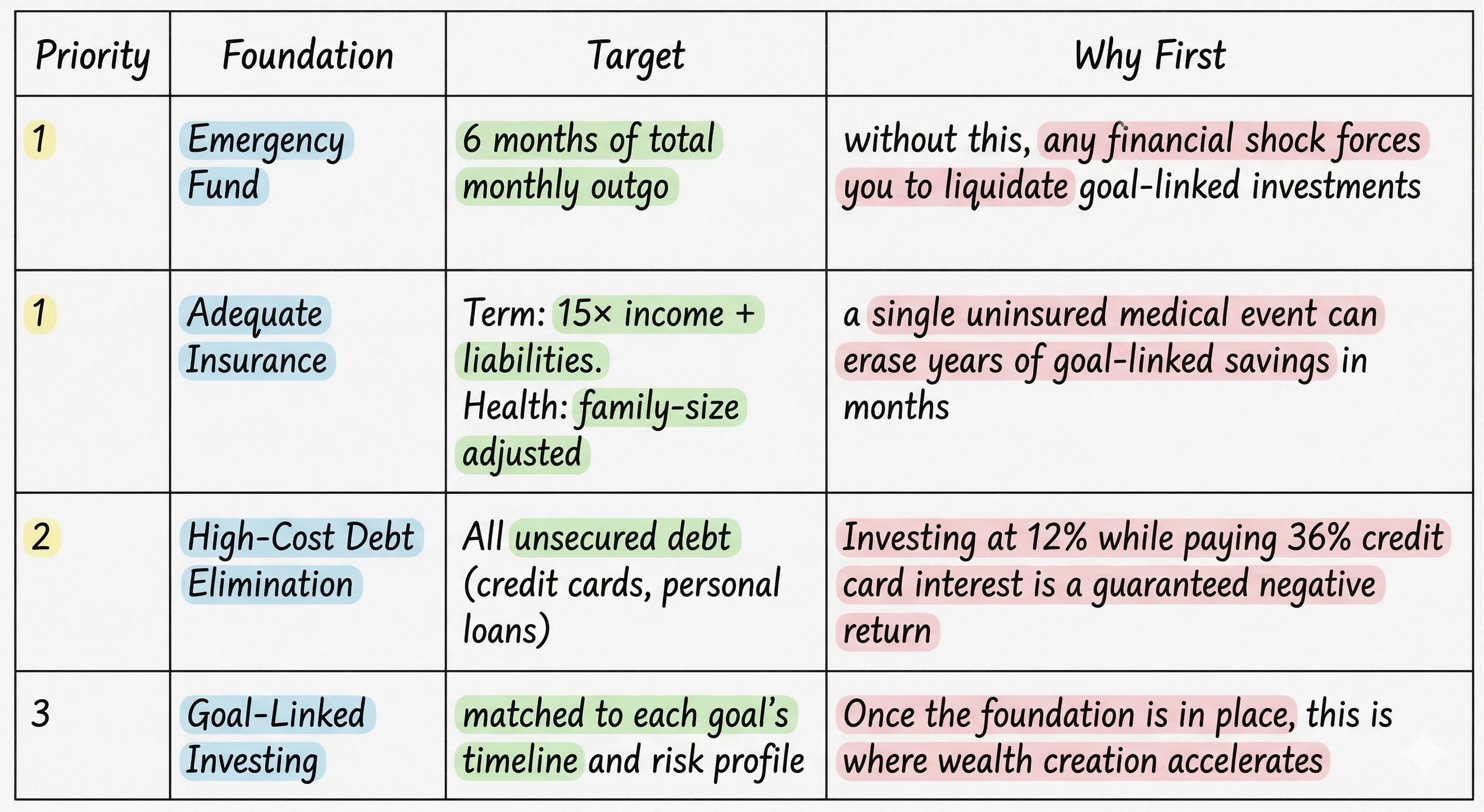

Step 3: Build the Foundation Before You Invest for Your Goals

This is where most financial goal-setting advice goes wrong. Most blogs and advisors jump straight to SIP allocation without asking whether a safety net is in place. That's like building the roof before the foundation.

Before a single rupee goes into a goal-linked investment, here's the priority sequence:

Priya had a term plan, but her family health insurance was through her employer, which is risky, as it disappears if she changes jobs. She had only about ₹1.8L in a savings account (only 1.5 months of her ₹1.2L monthly outgo), and a ₹45,000 credit card balance rolling over monthly.

Before she could start goal-linked SIPs, she needed 4.5 more months of emergency savings and to clear that credit card balance. That became Months 1–6 of her plan.

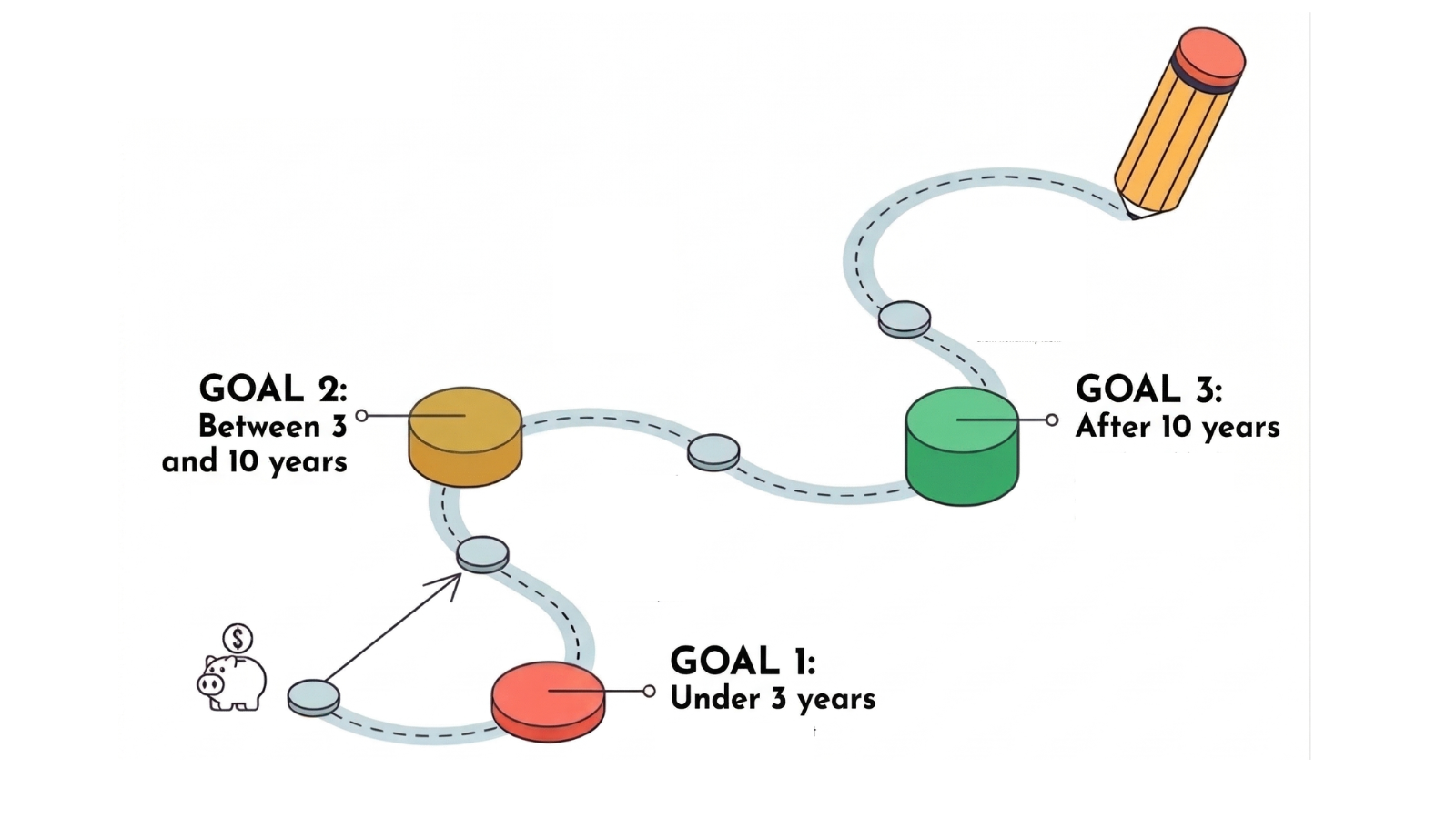

Step 4: Match Investments to the Right Goals

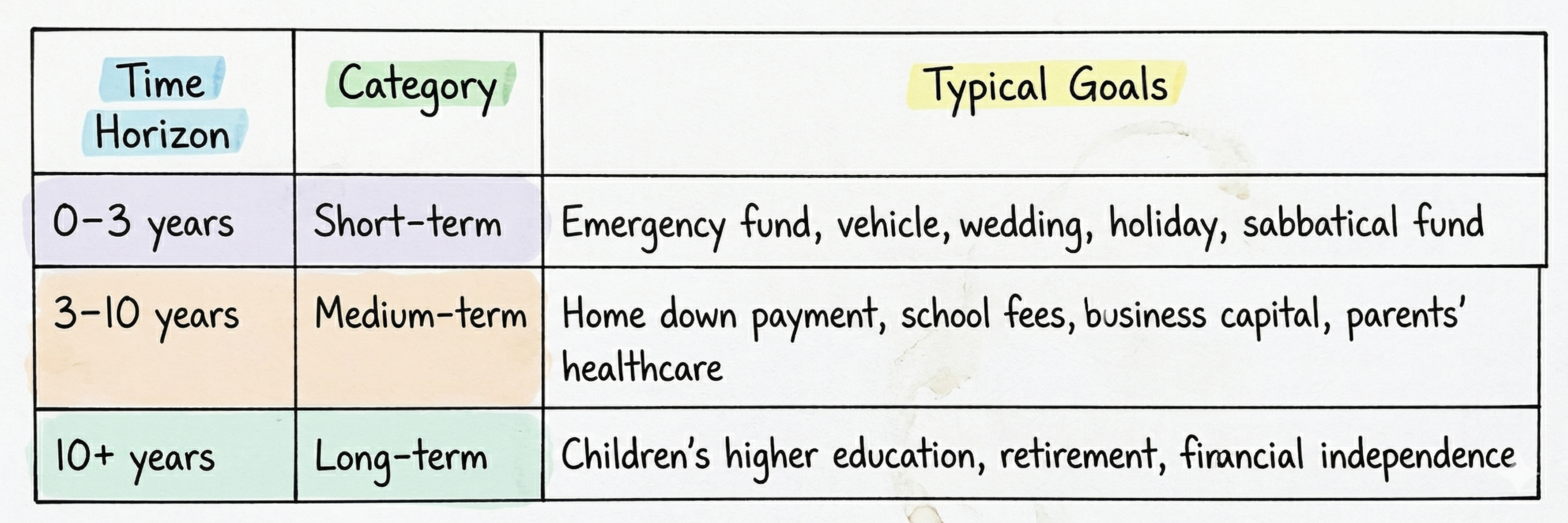

The time horizon of a goal determines its investment vehicle. This isn't about risk appetite or personal preference but it's mathematics. Short-term goals cannot absorb a market correction because there's no time to recover.

Goals within 3 years: Capital protection is non-negotiable. Use liquid funds, short-duration debt mutual funds, or fixed deposits. You're not trying to grow this money. You're making sure it's there when you need it.

Goals 3–10 years away: Use a balanced approach. Balanced advantage funds or aggressive hybrid funds give you equity exposure for growth with a debt cushion. As the goal approaches, systematically shift toward debt. Think of it as a glide path.

Goals beyond 10 years: This is where equity does its best work. Flexi-cap funds, Nifty 50 index funds, mid-cap funds - the longer the timeline, the more equity you can carry. Time smooths volatility. Equity is the compounding engine.

A note on taxes: Equity LTCG above ₹1.25L per year is taxed at 12.5%. Debt fund gains are taxed at your income slab. Factor this into your projections. Your goal sizing should use post-tax return assumptions, not pre-tax.

Priya's allocation: after clearing her credit card and building her emergency fund in Months 1–6, she started goal-linked SIPs with ₹25,000/month:

- ₹12,000/month → flexi-cap fund for retirement (26 years away)

- ₹8,000/month → aggressive hybrid fund for the flat down payment (7 years away)

- ₹5,000/month → liquid fund for a near-term goal (2 years away)

Note what this means: her ₹8,000/month toward the flat is well short of the ₹57,500/month it requires. That gap is deliberate, the foundation comes first, and the SIP grows as income grows.The plan starts where she actually is, not where she wishes she were.

Step 5: When and How to Review Your Financial Goals

A plan built today is built on today's income, expenses, goals, and market assumptions. All of these will change. The goal isn't a plan that lasts forever, it's a plan with clear review triggers so that when life changes, the plan adapts rather than silently drifts off course.

Review whenever any of these happen:

- A significant income change: A raise, job loss, bonus, or freelance income starting or stopping

- A new financial commitment: A home loan, a child, a parent requiring financial support

- A market event that moves your portfolio's value by 20% or more in either direction

- A goal that's been achieved, revised, or is no longer relevant

- A change in insurance or health status affecting your foundation layer

Beyond triggers, an annual review of the full goal picture is the minimum. Set a recurring calendar reminder. Treat it like a health check-up for your money.

Most people already have goals. The work is in translating them from intention into numbers, from numbers into a monthly action, and from that action into a habit that runs regardless of how busy life gets. That translation is what this framework is for.

Start with one goal. Put a rupee figure on it. Put a deadline on it. Calculate what it costs in future money. Then figure out what that requires from you every month.

If you're not sure where your foundation stands, calculating your Armor Score takes five minutes and tells you exactly which layer needs attention before goal-linked investing begins.

Frequently Asked Questions

What is goal-based financial planning?

Goal-based financial planning is the practice of assigning a specific rupee value, timeline, and monthly savings requirement to each financial goal. Instead of saving a general amount, you invest in instruments matched to each goal's time horizon and risk profile, so your money works as efficiently as possible toward each specific target.

How much emergency fund should I have before I start investing for goals?

At least 6 months of your total monthly outgo, including EMIs, insurance premiums, and household expenses, before allocating money to goal-linked SIPs. This ensures you never have to liquidate investments during a financial shock, which often means selling at a loss during a market downturn.

How does inflation affect my financial goals in India?

Inflation increases the future cost of every goal. At 6% general inflation, a goal that costs ₹50L today will cost ₹75.2L in 7 years and over ₹1.6 crore in 20 years. Education and healthcare costs inflate faster, at 8–14% annually. Any plan that doesn't adjust for inflation is systematically underestimating what you actually need.

How often should I review my financial goals?

At minimum, once a year. But also whenever there's a major life change: a salary increase or reduction, a new EMI, the birth of a child, a parent requiring support, or a market move of 20% or more in either direction. The best financial plan isn't one that never changes but one that adapts when your life does.

What is the right savings rate for financial goal setting in India?

A useful baseline is 30–40% of take-home income for goal-linked savings and investments, after accounting for insurance premiums and emergency fund contributions. For dual-income households in metro cities, this can be higher.